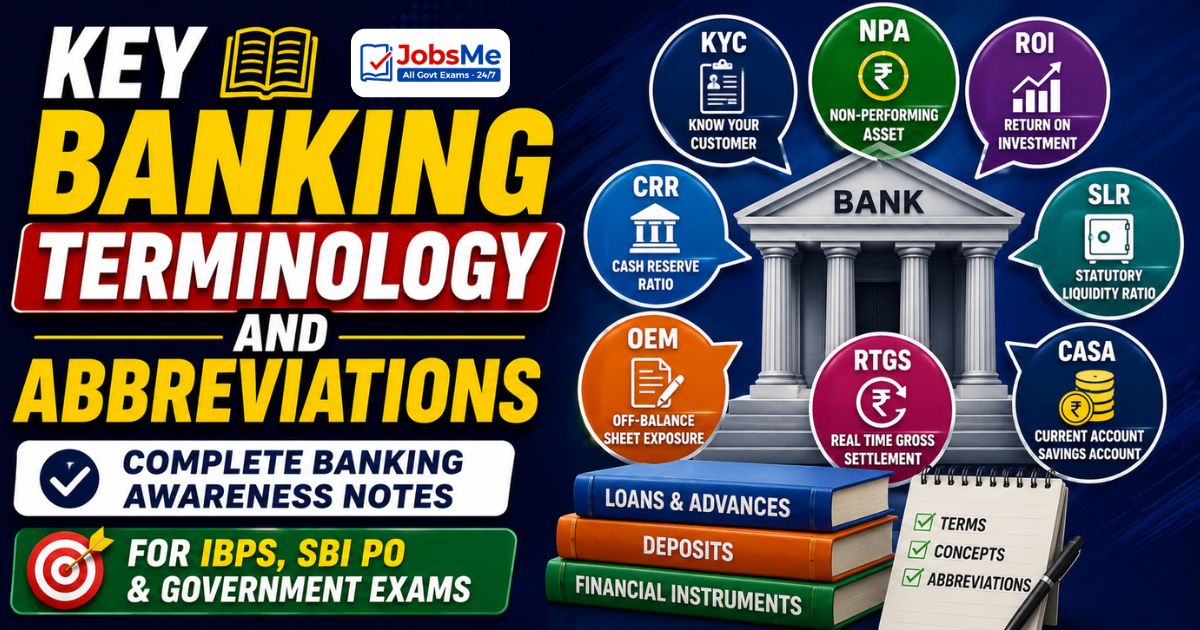

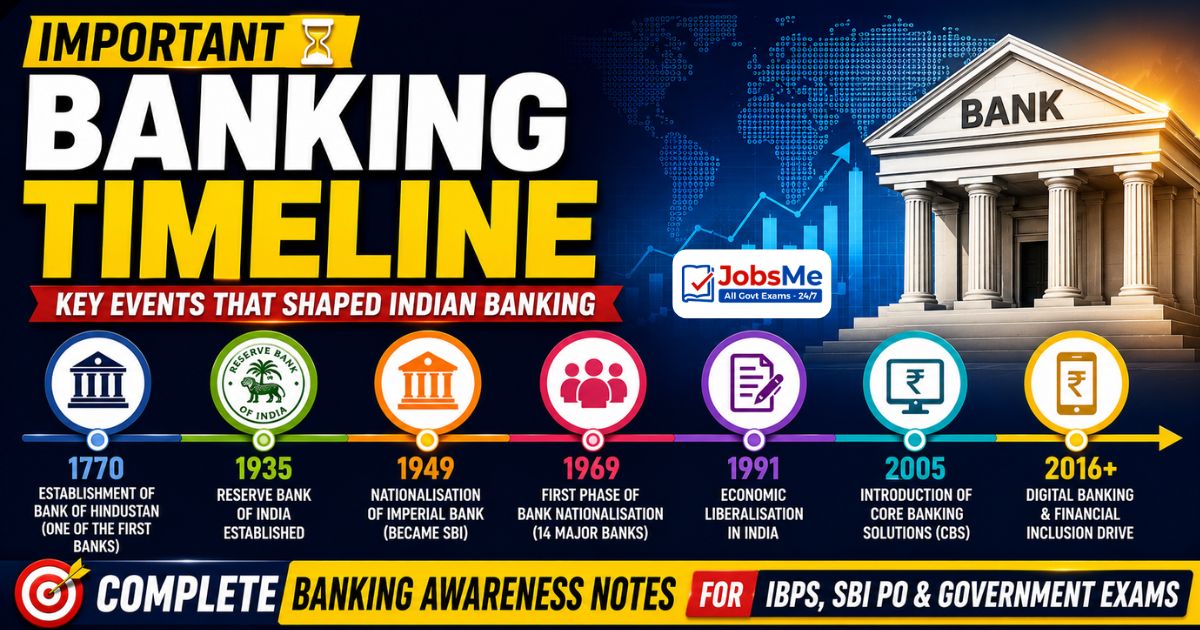

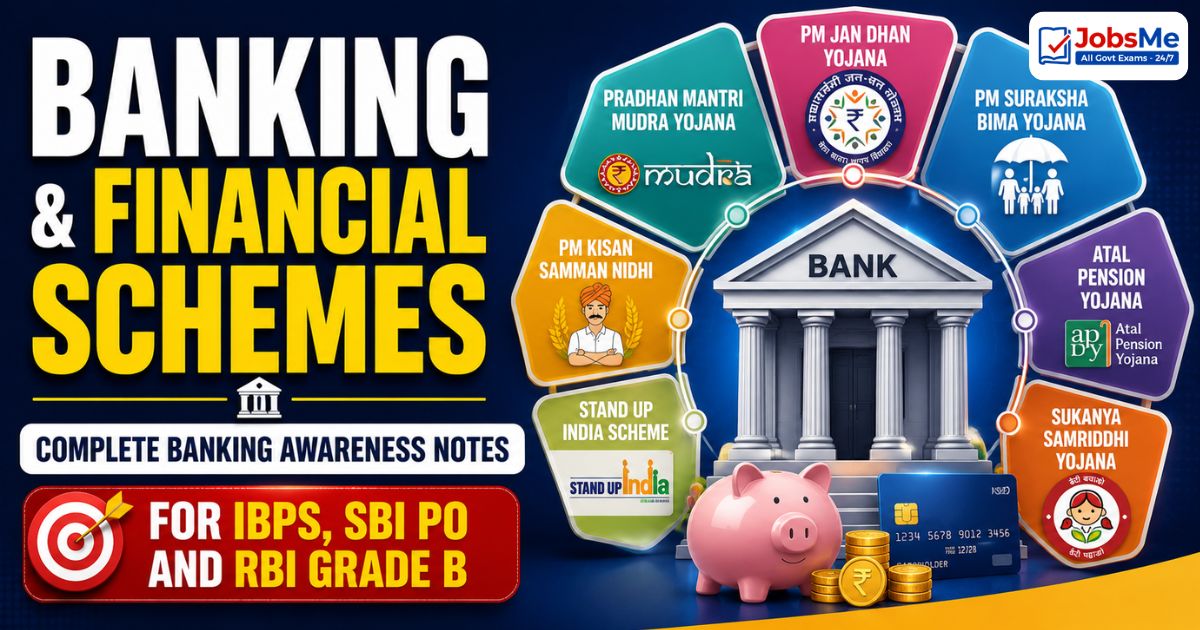

International Payment Systems – SWIFT CIPS SEPA Fedwire PAPSS | Banking Awareness Notes 2026

Payment Systems International covers all global payment and settlement systems tested in banking awareness exams. Topics include SWIFT (messaging network, 11,500+ institutions, ISO 20022 migration November 2025), CIPS (China's RMB system, 1,683 participants), SEPA (EU single payments area), TARGET2/TIPS (ECB systems), Fedwire, CHIPS, FedNow (USA), PIX (Brazil), PayNow (Singapore), PromptPay (Thailand), PAPSS (Africa, January 2022), Project Nexus (BIS) and all cross-border bilateral payment links including UPI-PayNow February 2023 and UPI-TIPS exploration 2025.

Jump to section

- International Payment Systems - Introduction

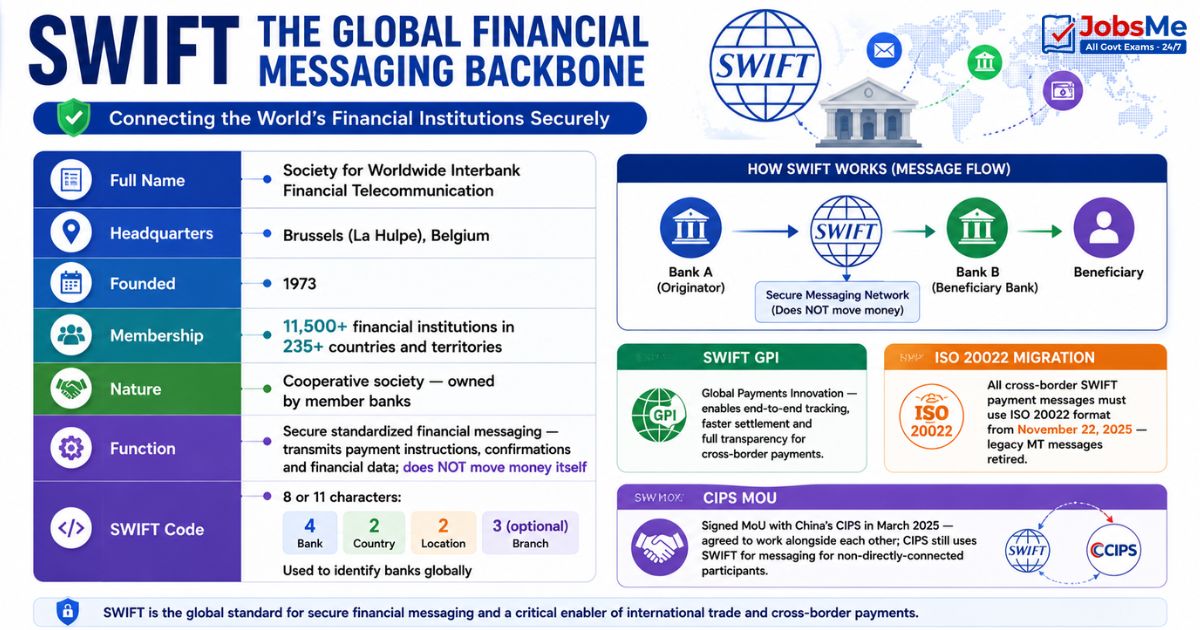

- SWIFT - The Global Financial Messaging Backbone

- CIPS - China's Cross-Border Interbank Payment System

- Major Regional and National Payment Systems Globally

- Cross-Border Payment Linkages - All Key Bilateral and Multilateral Links

- ISO 20022 - The Universal Payment Standard

- Memory Tricks - International Payment Systems

- One-Liners for Quick Revision

International Payment Systems - Introduction

International payment systems are increasingly tested in banking awareness examinations, especially in RBI Grade B, NABARD Grade A and IBPS PO Mains. The global payments landscape is undergoing rapid and significant transformation — new regional systems like CIPS, PAPSS and FedNow are emerging alongside the traditional SWIFT-dominated system. Cross-border instant payment links like UPI-PayNow represent a new era of seamless global financial connectivity.

SWIFT - The Global Financial Messaging Backbone

| Parameter | Details |

|---|---|

| Full Name | Society for Worldwide Interbank Financial Telecommunication |

| Headquarters | Brussels (La Hulpe), Belgium |

| Founded | 1973 |

| Membership | 11,500+ financial institutions in 235+ countries and territories |

| Nature | Cooperative society — owned by member banks |

| Function | Secure standardized financial messaging — transmits payment instructions, confirmations and financial data; does NOT move money itself |

| SWIFT Code | 8 or 11 characters: 4 (Bank) + 2 (Country) + 2 (Location) + 3 optional (Branch); used to identify banks globally |

| SWIFT GPI | Global Payments Innovation — enables end-to-end tracking, faster settlement and full transparency for cross-border payments |

| ISO 20022 Migration | All cross-border SWIFT payment messages must use ISO 20022 format from November 22, 2025 — legacy MT messages retired |

| CIPS MoU | Signed MoU with China's CIPS in March 2025 — agreed to work alongside each other; CIPS still uses SWIFT for messaging for non-directly-connected participants |

CIPS - China's Cross-Border Interbank Payment System

| Parameter | Details |

|---|---|

| Full Name | Cross-Border Interbank Payment System |

| Launched | 2015 (Phase 1: October 2015; Phase 2: 2018) |

| Operated by | People's Bank of China (PBoC) |

| Settlement Type | RTGS (Real-Time Gross Settlement) — immediate individual transaction settlement |

| Primary Currency | Chinese Yuan (RMB/Renminbi) — expanding to multi-currency capability |

| Participants (May 2025) | 1,683 direct and indirect participants from 103+ countries and territories |

| Annual Volume (2024) | ¥175.49 trillion (approximately USD 24.45 trillion) — 43% increase over 2023 |

| Purpose | Reduces China's dependence on SWIFT for RMB transactions; expands international use of Chinese Yuan |

Major Regional and National Payment Systems Globally

| System | Country/Region | Type | Key Features |

|---|---|---|---|

| SEPA SCT | EU (40+ countries) | Credit Transfer (standard — 1 day) | Single Euro Payments Area; euro-only; harmonized rules across 40+ countries |

| SEPA SCT Inst | EU (40+ countries) | Instant Credit Transfer (seconds) | Real-time instant euro payments; 24x7; growing adoption |

| SEPA SDD | EU (40+ countries) | Direct Debit (3 days) | Pan-European direct debit for recurring payments |

| TARGET2 / T2 | Eurozone (ECB) | RTGS | Large-value euro settlements; 1,000+ institutions; 99.98% availability; migrated to ISO 20022 |

| TIPS | Eurozone (ECB) | Instant Payments | TARGET Instant Payment Settlement; instant euro 24x7; RBI exploring UPI-TIPS bilateral link 2025 |

| CHAPS | United Kingdom | RTGS | Same-day high-value GBP settlements; operated by Bank of England |

| Faster Payments (FPS) | United Kingdom | Instant | Real-time retail GBP payments 24x7; most UK consumer transfers use this |

| Fedwire | USA | RTGS | Federal Reserve's large-value USD RTGS; 9,000+ institutions; migrated to ISO 20022 July 14, 2025 |

| CHIPS | USA | LVTS (Large Value Transfer) | Clearing House Interbank Payment System; private USD clearing; established 1970; migrated to ISO 20022 2025 |

| ACH | USA | Batch | Automated Clearing House; domestic retail batch payments — payroll, direct deposits, bill payments |

| FedNow | USA | Instant | Federal Reserve's instant payment rail; launched July 2023; competes with private RTP (Real-Time Payments) system |

| PIX | Brazil | Instant | Operated by Banco Central do Brasil (BCB); launched November 2020; 150+ million users; largest instant payment system in Latin America |

| SPEI | Mexico | RTGS | Sistema de Pagos Electrónicos Interbancarios; Mexico's domestic RTGS system; operated by Banco de México |

| Lynx | Canada | RTGS | High-value payment system; operated by Bank of Canada; 24x7 since 2021; replaced LVTS |

| PayNow | Singapore | Instant | Real-time peer-to-peer payments; uses mobile number/NRIC/UEN; linked with India UPI (Feb 2023) and Thailand PromptPay (Apr 2021) |

| PromptPay | Thailand | Instant | Real-time payments; linked with Singapore PayNow (April 2021 — world's first bilateral FPS link) |

| DuitNow | Malaysia | Instant | Real-time payments using national ID, mobile number or business registration number; part of Project Nexus |

| InstaPay | Philippines | Instant | Real-time retail payments; part of Project Nexus multilateral initiative |

| PAPSS | Africa (Pan-African) | RTGS | Pan-African Payment and Settlement System; launched January 2022; intra-African local-currency trade settlements; backed by African Union and Afreximbank |

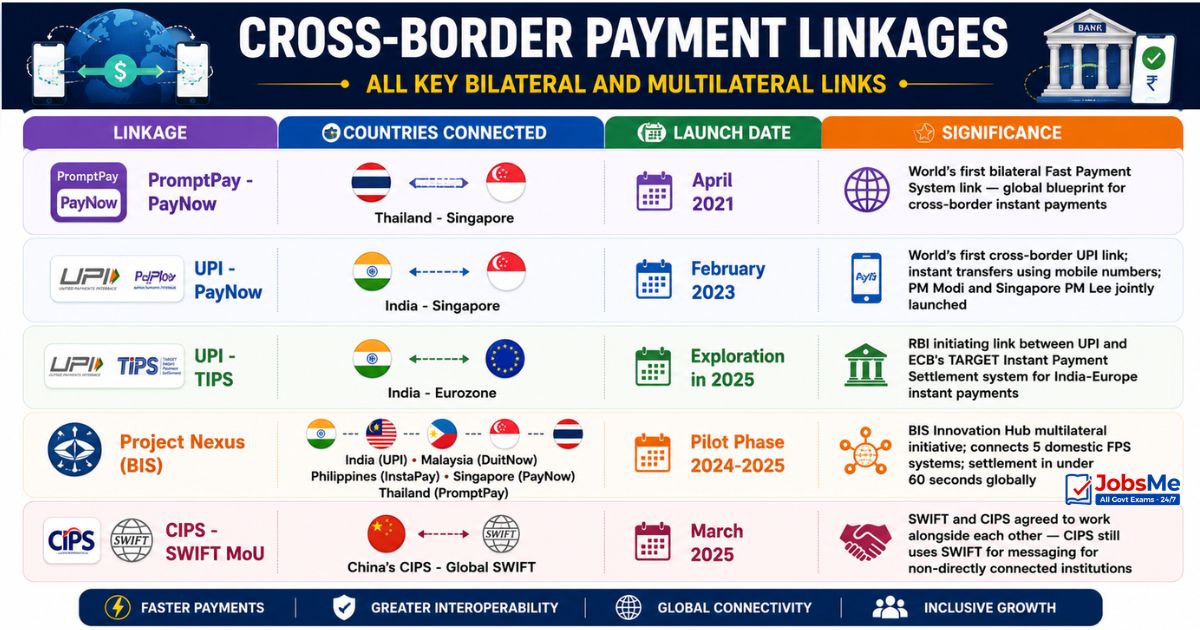

Cross-Border Payment Linkages - All Key Bilateral and Multilateral Links

| Linkage | Countries Connected | Launch Date | Significance |

|---|---|---|---|

| PromptPay - PayNow | Thailand - Singapore | April 2021 | World's first bilateral Fast Payment System link — global blueprint for cross-border instant payments |

| UPI - PayNow | India - Singapore | February 2023 | World's first cross-border UPI link; instant transfers using mobile numbers; PM Modi and Singapore PM Lee jointly launched |

| UPI - TIPS | India - Eurozone | Exploration in 2025 | RBI initiating link between UPI and ECB's TARGET Instant Payment Settlement system for India-Europe instant payments |

| Project Nexus (BIS) | India (UPI), Malaysia (DuitNow), Philippines (InstaPay), Singapore (PayNow), Thailand (PromptPay) | Pilot phase 2024-2025 | BIS Innovation Hub multilateral initiative; connects 5 domestic FPS systems; settlement in under 60 seconds globally |

| CIPS - SWIFT MoU | China's CIPS - Global SWIFT | March 2025 | SWIFT and CIPS agreed to work alongside each other — CIPS still uses SWIFT for messaging for non-directly connected institutions |

ISO 20022 - The Universal Payment Standard

ISO 20022 is an international standard for financial messaging that provides a common, rich, structured data format for payment transactions across all financial systems globally. The key benefit of ISO 20022 is that it carries significantly more data with each payment message compared to legacy formats — including full address details, purpose of payment, structured remittance information and legal entity identifiers.

ISO 20022 Adoption Timeline

| System | Migration Date | Impact |

|---|---|---|

| SWIFT (Global) | November 22, 2025 — mandatory | All cross-border payment messages must use ISO 20022; legacy MT format retired |

| Fedwire (USA) | July 14, 2025 | USA's main RTGS system moved to ISO 20022; enables richer data in US high-value payments |

| CHIPS (USA) | 2025 | Private USD clearing system adopted ISO 20022 |

| TARGET2/T2 (Eurozone) | Earlier migration | ECB's RTGS had already moved to ISO 20022 |

| India's NEFT/RTGS | ISO 20022 aligned | India's NEFT and RTGS systems have been upgraded to be ISO 20022 compatible |

Why ISO 20022 Matters for Banks

- Richer data: More structured information per transaction reduces manual intervention and exceptions

- Better compliance: Easier AML/CFT screening with structured beneficiary and purpose data

- Reduced fraud: More data per transaction makes fraudulent payments easier to detect

- Straight-through processing: Machines can handle end-to-end without human intervention

- Global interoperability: Same format used worldwide eliminates translation errors

Memory Tricks - International Payment Systems

Remember SWIFT vs CIPS

Trick: SWIFT = Message (the telegram). CIPS = Settlement (the money). SWIFT sends the instruction; CIPS actually settles RMB transactions for China. They signed an MoU in March 2025 to work together — they are not enemies, they are partners with different functions.

Remember PAPSS

Trick: PAPSS = Pan-African = Africa's SEPA. Just as SEPA allows euro payments across Europe without USD, PAPSS allows African local-currency trade settlements without going through USD. Launched January 2022. Backed by African Union + Afreximbank (Cairo, Egypt).

Remember World Firsts in Cross-Border Payments

Trick: First bilateral FPS link = PromptPay-PayNow (Thailand-Singapore, April 2021). First UPI cross-border = UPI-PayNow (India-Singapore, February 2023). Singapore is in both — it is the hub of cross-border instant payment innovation.

Remember ISO 20022

Trick: ISO 20022 = International Standard 20022. SWIFT deadline: November 22, 2025. Fedwire: July 14, 2025. After these dates — only ISO 20022; no old MT messages allowed.

One-Liners for Quick Revision

- SWIFT: Brussels (La Hulpe), Belgium; founded 1973; 11,500+ institutions; 235+ countries.

- SWIFT sends messages — it does NOT move money itself.

- CIPS: China's RMB payment system; launched 2015; 1,683 participants (May 2025).

- CIPS annual volume (2024): ¥175.49 trillion; 43% increase over 2023.

- CIPS + SWIFT MoU: signed March 2025; agreed to work alongside each other.

- SEPA covers 40+ countries; euro payments only; Credit Transfer 1 day, Instant seconds.

- TARGET2/T2: Eurozone ECB RTGS; 99.98% availability.

- TIPS: ECB instant payments 24x7; RBI exploring UPI-TIPS link in 2025.

- Fedwire: USA RTGS; 9,000+ institutions; migrated to ISO 20022: July 14, 2025.

- FedNow: USA instant payment rail; launched July 2023 by Federal Reserve.

- PIX: Brazil's instant payment; 150+ million users; launched November 2020.

- PAPSS: Africa; launched January 2022; African Union + Afreximbank (Cairo).

- PromptPay-PayNow: world's first bilateral FPS link; April 2021 (Thailand-Singapore).

- UPI-PayNow: India-Singapore; February 2023; world's first cross-border UPI link.

- Project Nexus (BIS): connects UPI, DuitNow, InstaPay, PayNow, PromptPay into one multilateral network.

- ISO 20022 SWIFT deadline: November 22, 2025 — all cross-border messages must use this format.

Preparing for competitive exams requires consistent revision. Platforms like JobsMe simplify preparation through:

- Daily Current Affairs

- Weekly Current Affairs

- Monthly Current Affairs

- Static GK for Competitive Exams

- Latest Government Jobs Notifications

- Computer Awareness

Stay updated, revise regularly, and attempt quizzes for better accuracy in UPSC, SSC CGL, IBPS PO/Clerk, SBI, RBI Grade B, RRB NTPC, Defence, and State PSC exams.

Free quiz • No signup required

Put this topic into practice with Current Affairs Quiz 12 June 2026 MCQs for UPSC, SSC, Banking, Railways & State PSC Exams. It is the quickest way to reinforce what you just learned.

Frequently Asked Questions

What is SWIFT and why is it important?

What is CIPS?

What is PAPSS?

What is ISO 20022 and why is it significant?

What was the world's first bilateral fast payment system link?

What is Project Nexus?

About the author