Negotiable Instruments – Complete Banking Awareness Notes for IBPS, SBI PO and Government Exams 2026

Negotiable Instruments covers the Negotiable Instruments Act 1881 and all instruments tested in banking awareness. Topics include bill of exchange, promissory note, all types of cheques — order, bearer, stale, post-dated, crossed — types of crossing, MICR code, difference between cheque and demand draft, CTS-2010 cheque truncation system, and international negotiable instruments like letter of credit and certificate of deposit.

Jump to section

- Negotiable Instruments - Introduction and Legal Framework

- 1. Bill of Exchange

- 2. Promissory Note

- 3. Cheques - The Most Important Negotiable Instrument for Exams

- Types of Crossing of Cheques

- Cheque vs Demand Draft - Critical Comparison for Exams

- MICR Code - Magnetic Ink Character Recognition

- CTS-2010 - Cheque Truncation System

- Cheque Dishonour - Section 138 of NI Act

- International Negotiable Instruments

- Memory Tricks - Negotiable Instruments

- One-Liners for Quick Revision

Negotiable Instruments - Introduction and Legal Framework

Negotiable Instruments are written documents that represent a right to receive a specified sum of money and can be transferred freely from one person to another. The transfer of a negotiable instrument transfers the right to receive the money to the new holder. These instruments are the foundation of commercial credit and business financing in India and globally.

In India, negotiable instruments are governed by the Negotiable Instruments Act, 1881. This Act defines three types of negotiable instruments: Bills of Exchange, Promissory Notes and Cheques. The Act was last significantly amended in 2018 to strengthen provisions against cheque dishonour.

Essential Characteristics of Negotiable Instruments

- Must be in writing: Oral promises or orders do not qualify as negotiable instruments

- Signed by maker or drawer: Valid signature is essential for enforceability

- Unconditional: The promise or order to pay must be unconditional — payment cannot depend on the occurrence of any event

- Definite sum of money: The amount must be specific and certain

- Freely transferable: Can be passed from person to person by delivery or endorsement

- Holder in due course: A person who receives a negotiable instrument in good faith and for value gets a better title than the transferor

1. Bill of Exchange

A Bill of Exchange is defined in the NI Act as a written instrument containing an unconditional order, signed by the maker, directing a certain person to pay a certain sum of money only to, or to the order of, a certain person or to the bearer of the instrument.

Key Features

- Three parties: Drawer (who draws the bill and orders payment), Drawee (the person ordered to pay — must accept the bill), Payee (who receives the payment)

- The drawee must accept the bill by signing it before it becomes binding on them

- Once accepted by the drawee, it becomes an Accepted Bill

- When accepted by a bank, it becomes a Bank Acceptance

- Commonly used in international trade — exporters draw bills on importers for goods shipped

- Can be discounted with banks for immediate liquidity — bank pays the face value minus discount charge

2. Promissory Note

A Promissory Note is an instrument in writing containing an unconditional undertaking signed by the maker to pay a certain sum of money only to, or to the order of, a certain person, or to the bearer of the instrument.

Key Features

- Two parties: Maker (who promises to pay) and Payee (who receives payment)

- The promise to pay is made by the maker — unlike a bill of exchange where an order is given by the drawer to someone else

- Must be in writing — cannot be verbal

- The promise must be unconditional

- Also called trade credit in commercial transactions

- Used in personal loans, business loans and commercial paper issuance

3. Cheques - The Most Important Negotiable Instrument for Exams

A Cheque is a bill of exchange drawn on a specified banker and not expressed to be payable otherwise than on demand. It is the most commonly used and most heavily tested negotiable instrument in banking awareness exams.

Three Parties to a Cheque

| Party | Role |

|---|---|

| Drawer | The account holder who writes and signs the cheque ordering the bank to pay |

| Drawee | The bank on which the cheque is drawn — the bank that makes the payment |

| Payee | The person or entity named on the cheque to receive the payment |

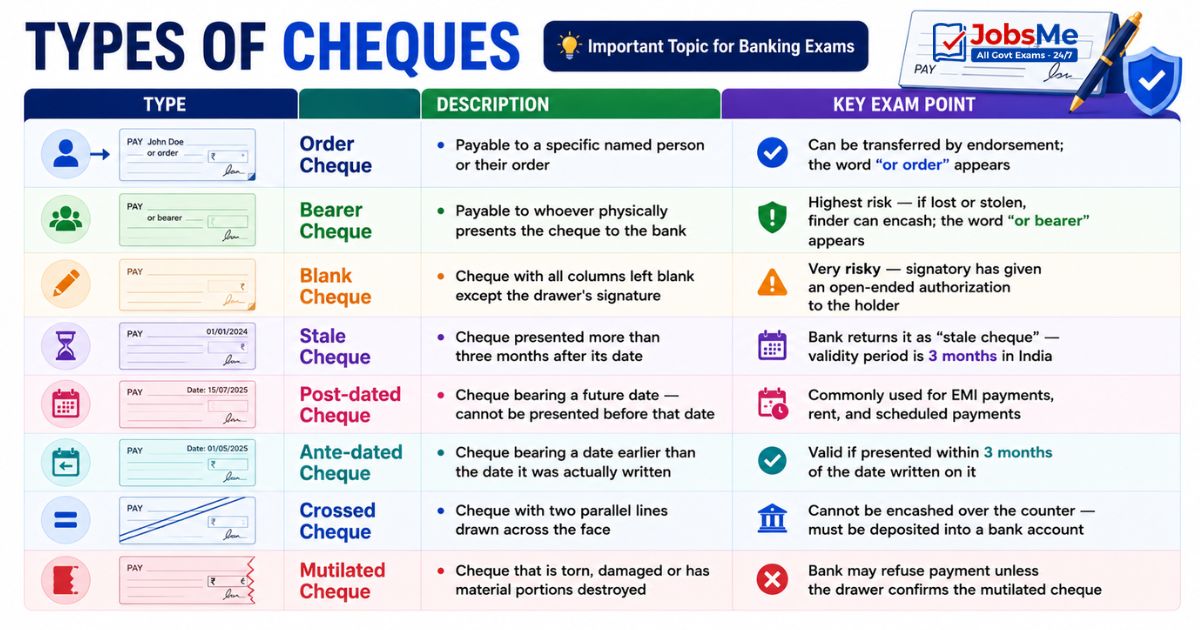

Types of Cheques

| Type | Description | Key Exam Point |

|---|---|---|

| Order Cheque | Payable to a specific named person or their order | Can be transferred by endorsement; the word "or order" appears on the cheque |

| Bearer Cheque | Payable to whoever physically presents the cheque to the bank | Highest risk — if lost or stolen, finder can encash; the word "or bearer" appears |

| Blank Cheque | Cheque with all columns left blank except the drawer's signature | Very risky — signatory has given an open-ended authorization to the holder |

| Stale Cheque | Cheque presented more than three months after its date | Bank returns it as "stale cheque" — validity period is 3 months in India |

| Post-dated Cheque | Cheque bearing a future date — cannot be presented before that date | Commonly used for EMI payments, rent, and scheduled payments |

| Ante-dated Cheque | Cheque bearing a date earlier than the date it was actually written | Valid if presented within 3 months of the date written on it |

| Crossed Cheque | Cheque with two parallel lines drawn across the face | Cannot be encashed over the counter — must be deposited into a bank account |

| Mutilated Cheque | Cheque that is torn, damaged or has material portions destroyed | Bank may refuse payment unless the drawer confirms the mutilated cheque |

Types of Crossing of Cheques

Crossing a cheque adds a layer of security by restricting how the cheque can be encashed. There are three types of crossing:

| Type of Crossing | How to Identify | Effect |

|---|---|---|

| General Crossing | Two parallel transverse lines across the face of the cheque, with or without the words and company or not negotiable between the lines | Cannot be paid in cash over the counter — must be deposited into any bank account; can be transferred |

| Special Crossing | Two parallel lines with the name of a specific bank written between the lines | Must be deposited only with the named bank — only that specific bank can collect payment |

| Account Payee Crossing | Two parallel lines with the words Account Payee or A/C Payee written between them | Most restrictive — can only be credited to the account of the named payee; cannot be transferred or endorsed to any other person |

Cheque vs Demand Draft - Critical Comparison for Exams

| Parameter | Cheque | Demand Draft (DD) |

|---|---|---|

| Who issues it | Individual account holder (the drawer) | Bank itself — issued by the bank on behalf of the applicant |

| Payment certainty | Uncertain — can bounce if insufficient funds or signature mismatch | Certain — bank has already collected the amount before issuing DD |

| Can be stopped | Yes — drawer can issue stop payment instructions to the bank | No — cannot be stopped once issued (only cancelled by the issuing bank) |

| Governed by NI Act 1881 | Yes — specifically defined and governed | Not specifically defined in the NI Act 1881 |

| Charges | No charge for issuing (cheque book provided by bank) | Bank charges commission for issuing a demand draft |

| Requirement | Requires the drawer to have sufficient balance in account | Payment is made upfront to the bank before DD is issued |

| Dishonour | Can be dishonoured — Section 138 of NI Act provides criminal liability for cheque bounce | Cannot be dishonoured by the bank — the bank is the drawer |

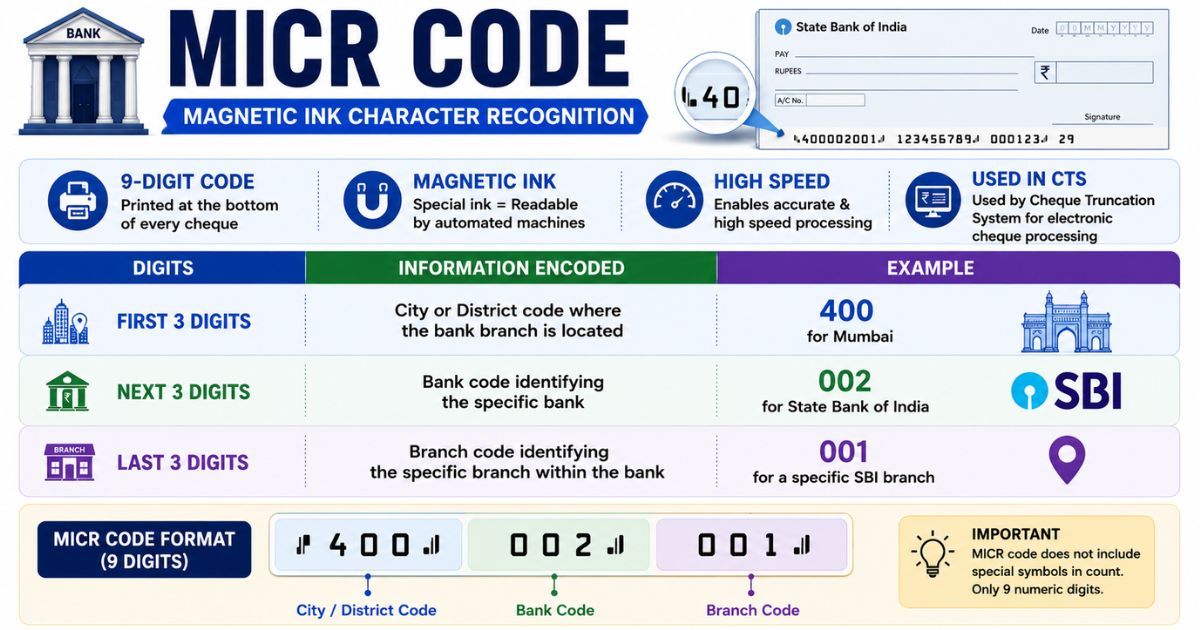

MICR Code - Magnetic Ink Character Recognition

MICR is a 9-digit code printed at the bottom of every cheque using special magnetic ink that allows automated machines to read and process cheques accurately and at high speed. The MICR code is used by the Cheque Truncation System (CTS) for electronic cheque processing.

| Digits | Information Encoded | Example |

|---|---|---|

| First 3 digits | City or District code where the bank branch is located | 400 for Mumbai |

| Next 3 digits | Bank code identifying the specific bank | 002 for State Bank of India |

| Last 3 digits | Branch code identifying the specific branch within the bank | 001 for a specific SBI branch |

CTS-2010 - Cheque Truncation System

The Cheque Truncation System (CTS) was introduced by RBI to modernize and speed up cheque clearing by replacing the physical movement of cheques with electronic transmission of cheque images. The CTS-2010 standard specifies the physical and data requirements for all new cheques issued in India.

How CTS Works

- When a customer deposits a cheque, the bank of deposit scans the cheque and creates a digital image

- The digital image and MICR data are transmitted electronically to the clearing house and then to the drawee bank

- The drawee bank verifies the image and authorizes payment

- The physical cheque stays with the depositing bank — it is never physically transported

- This eliminates transit time, reduces risk of loss in transit and speeds up clearing significantly

- Customers receive credit within one working day in most cases

CTS-2010 Security Features

- Void pantograph — special background print that shows "VOID" when photocopied

- Watermark — "CTS-INDIA" watermark visible when held against light

- UV fluorescent ink — bank logo visible only under UV light

- Magnetic ink — MICR line printed with ink readable by magnetic readers

- Specific paper quality requirements to prevent chemical tampering

Cheque Dishonour - Section 138 of NI Act

When a cheque is returned unpaid by the bank due to insufficient funds or for the amount exceeding the arrangement — this is called cheque dishonour or cheque bounce. The NI Act provides strict remedies:

- Section 138: Makes cheque dishonour a criminal offence — punishable with imprisonment up to 2 years or fine up to twice the cheque amount or both

- The payee must send a written demand notice to the drawer within 30 days of receiving the dishonoured cheque

- The drawer has 15 days from receipt of notice to make payment

- If payment not made, complaint can be filed in court within one month of expiry of the 15-day notice period

- Section 143A (added in 2018): Court can order payment of interim compensation of up to 20% of the cheque amount to the payee during pendency of the case

- Section 148 (added in 2018): Appellate court can order deposit of minimum 20% of the fine or compensation awarded by trial court

International Negotiable Instruments

| Instrument | Description | Use Case |

|---|---|---|

| Letter of Credit (LC) | Bank guarantee issued by the buyer's bank promising payment to the seller upon presentation of specified shipping documents | International trade — eliminates counterparty risk between exporters and importers in different countries |

| Bank Guarantee | Commitment by a bank to pay the beneficiary if the bank's customer fails to fulfil their contractual obligation | Performance guarantees in construction contracts, bid bonds in government tenders |

| Certificate of Deposit (CD) | Tradeable fixed-term deposit instrument issued by a bank; higher interest than regular FD; can be sold in the secondary market | Corporates and institutions invest large sums for fixed periods while retaining option to sell before maturity |

| Commercial Paper (CP) | Unsecured short-term promissory note issued by corporates to raise working capital | Large companies borrow directly from the market without going through banks; tenures typically 7 days to 1 year |

| Treasury Bills (T-Bills) | Short-term government borrowing instruments; 91-day, 182-day and 364-day | Government raises short-term funds; banks and institutions invest surplus funds safely |

Memory Tricks - Negotiable Instruments

Remember Three Types of NI

Trick: BPC = Bill of Exchange, Promissory note, Cheque. These are the three negotiable instruments defined in the NI Act 1881. BPC — like "Basics of Payment Contracts."

Remember Types of Crossing

Trick: GSA = General (any bank), Special (named bank), Account Payee (named person's account only). Each crossing is more restrictive than the previous one. General is the least restrictive, Account Payee is the most restrictive.

Remember Cheque Validity

Trick: Cheques are valid for THREE months. After 3 months it becomes a stale cheque. Three is also the number of parties to a cheque (drawer, drawee, payee). Three appears twice — validity and parties.

Remember Section 138

Trick: "138 — One call (notice within 30 days), 3+8=11... wait — easier: 1 month notice, 3 rounds (1 dishonour + notice + complaint), 8... just remember Sec 138 = Criminal liability for cheque bounce." Imprisonment up to 2 years, fine up to twice the cheque amount.

One-Liners for Quick Revision

- Negotiable Instruments Act: 1881; amended significantly in 2018.

- Three types of NI: Bill of Exchange, Promissory Note, Cheque.

- Bill of Exchange has three parties: Drawer, Drawee, Payee.

- Promissory Note has two parties: Maker and Payee.

- Cheque three parties: Drawer (account holder), Drawee (bank), Payee (recipient).

- Stale cheque: more than 3 months old from date of issue.

- Bearer cheque: payable to whoever presents it — highest risk if lost.

- Account Payee crossing: most restrictive — only credited to named payee's account.

- Cheque can be stopped; DD cannot be stopped once issued.

- DD payment is certain; cheque payment is uncertain (can bounce).

- Demand Draft not specifically defined in NI Act.

- MICR: 9 digits — city (3) + bank (3) + branch (3).

- CTS-2010: cheques cleared through electronic images, not physical movement.

- Section 138 of NI Act: criminal liability for cheque dishonour.

- Imprisonment for cheque bounce: up to 2 years; fine up to twice cheque amount.

- Section 143A (2018): interim compensation of up to 20% during trial.

Preparing for competitive exams requires consistent revision. Platforms like JobsMe simplify preparation through:

- Daily Current Affairs

- Weekly Current Affairs

- Monthly Current Affairs

- Static GK for Competitive Exams

- Latest Government Jobs Notifications

- Computer Awareness

Stay updated, revise regularly, and attempt quizzes for better accuracy in UPSC, SSC CGL, IBPS PO/Clerk, SBI, RBI Grade B, RRB NTPC, Defence, and State PSC exams.

Free quiz • No signup required

Put this topic into practice with Current Affairs Quiz 13–15 June 2026 MCQs for UPSC, SSC, Banking, Railways, Defence & State PSC Exams. It is the quickest way to reinforce what you just learned.

Frequently Asked Questions

What is the Negotiable Instruments Act 1881?

What is the difference between a cheque and a demand draft?

What is a stale cheque?

What is a crossed cheque?

What is MICR code on a cheque?

What is CTS-2010?

What is a letter of credit in banking?

About the author