Financial Inclusion and Banking Ombudsman – Banking Awareness Notes 2026 for IBPS and SBI

Financial Inclusion and Banking Ombudsman covers two critical topics tested in all banking awareness sections. Financial inclusion covers the No-Frills Account, BSBDA, PMJDY, Small Account, AePS, and the broader initiatives to bring unbanked populations into the formal banking system. The Banking Ombudsman section covers the RBI's integrated ombudsman scheme RB-IOS 2021, its coverage, complaint process, grounds for complaint, maximum award amounts, appellate authority and conditions for rejection. Both topics are high-frequency in IBPS PO, SBI Clerk, RBI Grade B and NABARD exams.

Jump to section

- Financial Inclusion - Introduction and Importance

- Evolution of Financial Inclusion Accounts

- AePS - Aadhaar Enabled Payment System

- Banking Correspondents (BCs)

- Banking Ombudsman - Complete Notes

- Consumer Protection Act (COPRA)

- Memory Tricks - Financial Inclusion and Banking Ombudsman

- One-Liners for Quick Revision

Financial Inclusion - Introduction and Importance

Financial inclusion is a strategic priority for India's banking system and government. It refers to ensuring that every individual and household — particularly the rural poor, women, tribal communities and migrant workers — has access to formal financial services including bank accounts, credit, insurance and remittance services at affordable cost.

Financial inclusion is directly tested in IBPS PO, SBI Clerk, RBI Grade B and NABARD Grade A exams. Questions cover specific schemes, their launch dates, features, eligibility criteria and the institutions implementing them.

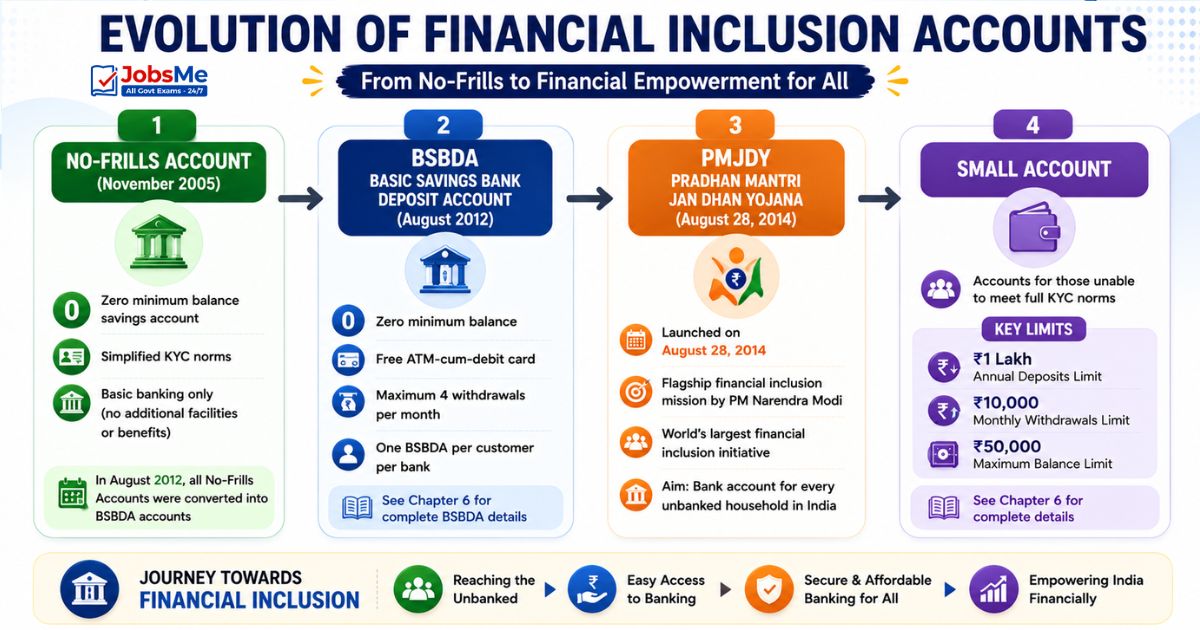

Evolution of Financial Inclusion Accounts

No-Frills Account (November 2005)

The No-Frills Account was introduced by RBI in November 2005 as a zero-minimum-balance savings account with simplified KYC norms designed to bring the unbanked population into the banking system. These accounts had no additional facilities or benefits beyond basic banking. In August 2012, all No-Frills Accounts were converted into Basic Savings Bank Deposit Accounts (BSBDAs).

BSBDA - Basic Savings Bank Deposit Account (August 2012)

The BSBDA replaced No-Frills Accounts and introduced standardized features across all banks. See Chapter 6 for complete BSBDA details. Key points: zero minimum balance, free ATM-cum-debit card, maximum four withdrawals per month, one BSBDA per customer per bank.

PMJDY - Pradhan Mantri Jan Dhan Yojana (August 28, 2014)

The Pradhan Mantri Jan Dhan Yojana (PMJDY) is India's flagship financial inclusion mission launched by PM Narendra Modi on August 28, 2014. It is the world's largest financial inclusion initiative and aimed to provide a bank account to every unbanked household in India within a specific timeframe.

Small Account

Accounts for those unable to meet full KYC norms. See Chapter 6 for complete details on limits: Rs. 1 lakh annual deposits, Rs. 10,000 monthly withdrawals, Rs. 50,000 maximum balance.

AePS - Aadhaar Enabled Payment System

The AePS (Aadhaar Enabled Payment System) is a landmark financial inclusion tool operated by NPCI that uses the Aadhaar biometric authentication infrastructure to deliver basic banking services through Banking Correspondents (BCs) in remote areas.

Services Available Through AePS

- Cash Withdrawal — Withdraw cash from any bank account using only Aadhaar number and fingerprint at any banking correspondent

- Cash Deposit — Deposit cash into a bank account through banking correspondent

- Balance Inquiry — Check bank account balance

- Mini Statement — Get last 5 transaction details

- Fund Transfer — Transfer funds from one Aadhaar-linked account to another

- BHIM Aadhaar Pay — Merchants can receive payments using customer's Aadhaar biometric authentication without any card or smartphone required from the customer

Why AePS is Critical for Financial Inclusion

AePS does not require a debit card, PIN, mobile phone or internet connection on the customer's part. The only requirement is the customer's Aadhaar number and fingerprint. This makes it the most accessible banking channel for illiterate, elderly, rural and technically challenged customers who cannot use ATMs, mobile banking or internet banking.

Banking Correspondents (BCs)

Banking Correspondents (BCs) are retail agents authorized by banks to provide basic banking services in areas where a physical bank branch is not economically viable. BCs use handheld devices connected to CBS (Core Banking Solution) to deliver services like account opening, deposits, withdrawals, remittances and loan repayments, often using AePS.

- BCs can be individuals, NGOs, microfinance institutions, post offices, insurance agents or retail shop owners

- They extend the reach of banks to the last mile in remote rural and tribal areas

- BCs are a key component of the government's and RBI's financial inclusion strategy

Banking Ombudsman - Complete Notes

What is the Banking Ombudsman?

The Banking Ombudsman is a senior official appointed by the Reserve Bank of India to receive and resolve customer complaints against banks and other financial institutions regarding deficiency in banking services. The scheme is established under Section 35A of the Banking Regulation Act, 1949.

Historical Timeline of Banking Ombudsman

| Year | Development |

|---|---|

| 1995 | First Banking Ombudsman Scheme introduced in India |

| 2006 | Revised Banking Ombudsman Scheme introduced and expanded |

| 2007, 2009 | Further amendments to expand scope of complaints |

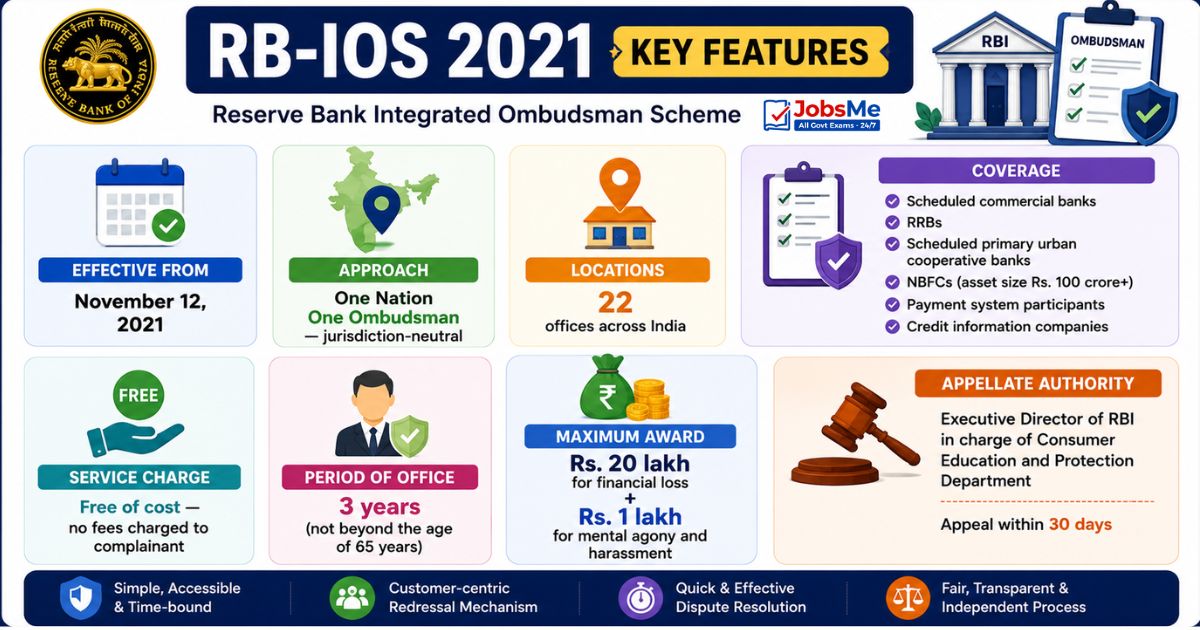

| November 12, 2021 | RBI Integrated Ombudsman Scheme (RB-IOS 2021) launched — integrated three separate schemes into one |

RB-IOS 2021 - Key Features

| Parameter | Details |

|---|---|

| Effective from | November 12, 2021 |

| Approach | One Nation One Ombudsman — jurisdiction-neutral |

| Locations | 22 offices across India |

| Coverage | Scheduled commercial banks, RRBs, scheduled primary urban cooperative banks, NBFCs (asset size Rs. 100 crore+), payment system participants, credit information companies |

| Service charge | Free of cost — no fees charged to complainant |

| Period of office | 3 years (not beyond the age of 65 years) |

| Maximum award | Rs. 20 lakh for financial loss + Rs. 1 lakh for mental agony and harassment |

| Appellate Authority | Executive Director of RBI in charge of Consumer Education and Protection Department; appeal within 30 days |

How to File a Complaint with the Banking Ombudsman

- First approach the bank — Submit a written complaint to the concerned bank branch or head office and obtain an acknowledgment.

- Wait 30 days — Give the bank 30 days to resolve the complaint. If not resolved satisfactorily within 30 days, proceed to the Ombudsman.

- File within time limit — Must file the complaint with the Ombudsman within one year of receiving the bank's reply or within one year and one month from the date of the complaint to the bank.

- Submit complaint — File via the Centralised Receipt and Processing Centre (CRPC) online, by post, by email or in person at any Ombudsman office. No specific format required — can be on plain paper.

- Free of charge — No fees are charged at any stage of the complaint process.

Grounds for Filing Complaint with Banking Ombudsman

- Non-payment or inordinate delay in payment or collection of cheques, drafts, bills

- Refusal to open deposit account or close account without valid reason

- Non-acceptance of small denomination notes and coins without valid reason

- Failure to adhere to prescribed working hours

- Failure to issue or delay in issue of demand drafts, pay orders or banker's cheques

- Non-adherence to RBI instructions on ATM, debit card or credit card operations

- Non-disbursement or delay in disbursement of pension to the extent attributable to bank actions

- Refusal to accept or delay in accepting payments towards taxes

- Complaints from NRIs regarding remittances or deposits in India

- Levying charges without adequate prior notice to the customer

- Non-adherence to BCSBI (Banking Codes and Standards Board of India) guidelines

- Unauthorized electronic transactions — fraud, cyber crimes involving bank accounts

When Complaints Are Rejected

- The complaint is frivolous, vexatious or without sufficient cause

- The complaint is beyond the pecuniary jurisdiction of the Ombudsman

- The same matter is sub-judice before a court, tribunal or arbitrator

- The complainant has not approached the bank first for redressal

- The complaint is not pursued with reasonable diligence by the complainant

- No loss, damage or inconvenience was caused to the complainant

Consumer Protection Act (COPRA)

- COPRA (Consumer Protection Act) enacted in 1986 (Act 68 of 1986)

- Implemented on April 15, 1987

- Comprehensively amended in 2002

- New Consumer Protection Act 2019 replaced the 1986 Act

- The Consumer Protection Act 2019 covers e-commerce, product liability, mediation and Central Consumer Protection Authority (CCPA)

Memory Tricks - Financial Inclusion and Banking Ombudsman

Remember PMJDY Date

Trick: "August 28, 2014 — 28th day, 8th month, year 2014." The number sequence 28-8-2014 is easy to remember if you think of it as a descending pattern: 28 (date) then 8 (month) then 2014 (year).

Remember Ombudsman Award Limit

Trick: "20 lakh for financial loss + 1 lakh for mental pain." Financial loss gets the bigger award (20) and mental agony gets the smaller add-on (1). Total potential award = Rs. 21 lakh maximum.

Remember RB-IOS 2021 Launch

Trick: "November 12, 2021 — National Education Day (November 11) plus one day." National Education Day is November 11. RB-IOS came the very next day — November 12, 2021.

One-Liners for Quick Revision

- No-Frills Account introduced: November 2005; converted to BSBDA in August 2012.

- PMJDY launched: August 28, 2014 by PM Narendra Modi.

- PMJDY accident insurance: Rs. 2 lakh; overdraft: Rs. 10,000.

- Banking Ombudsman scheme first introduced: 1995.

- Current scheme: RB-IOS 2021, effective from November 12, 2021.

- Ombudsman operates from 22 locations across India.

- Maximum award: Rs. 20 lakh financial loss + Rs. 1 lakh mental agony.

- Service is completely free for complainants.

- Must approach bank first; if unresolved in 30 days, can approach Ombudsman.

- Appellate Authority: Executive Director of RBI (Consumer Education and Protection Dept).

- AePS uses Aadhaar biometric for banking — no card or internet needed by customer.

- BCs (Banking Correspondents) extend banking to areas where physical branches are not viable.

Preparing for competitive exams requires consistent revision. Platforms like JobsMe simplify preparation through:

- Daily Current Affairs

- Weekly Current Affairs

- Monthly Current Affairs

- Static GK for Competitive Exams

- Latest Government Jobs Notifications

- Computer Awareness

Stay updated, revise regularly, and attempt quizzes for better accuracy in UPSC, SSC CGL, IBPS PO/Clerk, SBI, RBI Grade B, RRB NTPC, Defence, and State PSC exams.

Free quiz • No signup required

Put this topic into practice with Current Affairs Quiz 12 June 2026 MCQs for UPSC, SSC, Banking, Railways & State PSC Exams. It is the quickest way to reinforce what you just learned.

Frequently Asked Questions

What is financial inclusion in banking?

What is the Banking Ombudsman scheme?

What is the maximum compensation that can be awarded by the Banking Ombudsman?

What is the RB-IOS 2021?

Who can file a complaint with the Banking Ombudsman?

What is AePS and why is it important for financial inclusion?

About the author