Types of Banks in India – Complete Notes for IBPS, SBI PO and Government Exams 2026

Types of Banks in India covers all categories of banks that are tested in banking awareness sections of IBPS PO, SBI Clerk, RBI Grade B, NABARD and all government banking examinations in 2026. This chapter explains the classification of banks into scheduled and non-scheduled, the four types of commercial banks — public sector, private sector, foreign and regional rural banks — and the specialized differentiated banks like payment banks, small finance banks and cooperative banks. The chapter also covers NBFCs, their differences from banks, and the key features of each bank type with exam-relevant facts.

Jump to section

- Types of Banks in India - Introduction

- Classification of Banks - Scheduled vs Non-Scheduled

- Types of Commercial Banks in India

- Differentiated Banks - New Categories

- Cooperative Banks in India

- Non-Banking Financial Companies (NBFCs) - Key Differences

- Memory Tricks - Types of Banks

- One-Liners for Quick Revision - Types of Banks in India

Types of Banks in India - Introduction

Understanding the different types of banks operating in India is one of the most fundamental and frequently tested topics in banking awareness sections of IBPS PO, SBI Clerk, RBI Grade B, NABARD Grade A and all other government banking examinations. Examiners regularly ask questions about the classification of banks, ownership structure, deposit limits, lending restrictions, regulatory frameworks and real-world examples of each bank type.

The Indian banking system is classified into two broad categories: Scheduled Banks and Non-Scheduled Banks. Scheduled banks are further divided into commercial banks (public sector, private sector, foreign and regional rural banks) and cooperative banks. There are also specialized differentiated bank categories like Payment Banks and Small Finance Banks introduced in recent years.

Classification of Banks - Scheduled vs Non-Scheduled

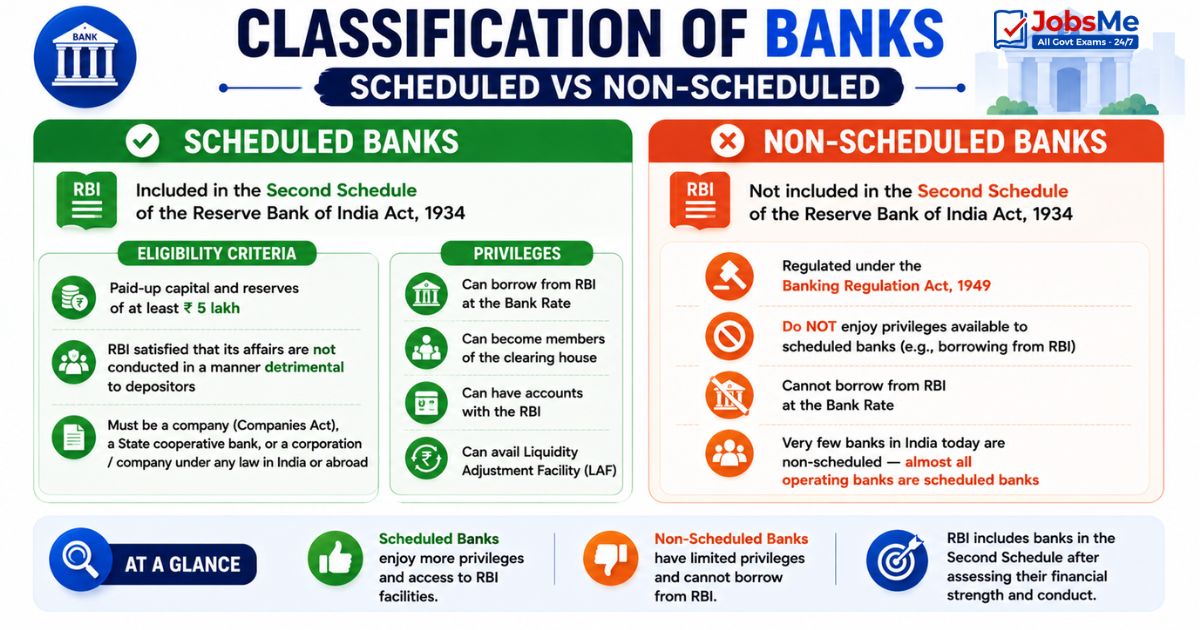

Scheduled Banks

Scheduled Banks are those banks that are included in the Second Schedule of the Reserve Bank of India Act, 1934. To qualify for inclusion in the Second Schedule, a bank must:

- Have paid-up capital and reserves of at least Rs. 5 lakh

- Satisfy the RBI that its affairs are not conducted in a manner detrimental to depositors

- Be a company as defined under the Companies Act, a State cooperative bank, or a corporation or company incorporated under any law in force in India or abroad

Scheduled banks enjoy the following privileges: they can borrow from RBI at the Bank Rate, they can become members of the clearing house, they can have accounts with the RBI and avail of its Liquidity Adjustment Facility (LAF).

Non-Scheduled Banks

Non-Scheduled Banks are banks that are not listed in the Second Schedule of the RBI Act. They are still regulated under the Banking Regulation Act, 1949 but they do not enjoy the privileges available to scheduled banks such as borrowing from the RBI. Very few banks in India today are non-scheduled — almost all operating banks are scheduled banks.

Types of Commercial Banks in India

1. Public Sector Banks (PSBs)

Public Sector Banks are banks in which the Government of India holds more than 50% of the total equity share capital. These banks are also called nationalized banks or government banks. After the major consolidation of 2019-2020, there are currently 12 public sector banks in India.

Features of Public Sector Banks

- Government ownership of more than 50% equity — government controls board appointments and policy direction

- Operate under both the Banking Regulation Act 1949 and applicable government guidelines

- Mandated to fulfill social objectives like priority sector lending, financial inclusion and rural banking

- Subject to Parliamentary oversight and government audit

- Employees are considered quasi-government employees in terms of service conditions

- Generally have lower NIM compared to private banks due to higher social obligations and higher NPA burden

List of 12 Current Public Sector Banks

| Public Sector Bank | Headquarters |

|---|---|

| State Bank of India (SBI) | Mumbai |

| Bank of Baroda | Vadodara |

| Bank of India | Mumbai |

| Bank of Maharashtra | Pune |

| Canara Bank | Bengaluru |

| Central Bank of India | Mumbai |

| Indian Bank | Chennai |

| Indian Overseas Bank | Chennai |

| Punjab and Sind Bank | New Delhi |

| Punjab National Bank | New Delhi |

| UCO Bank | Kolkata |

| Union Bank of India | Mumbai |

2. Private Sector Banks

Private Sector Banks are banks in which the majority of equity is held by private individuals and institutions rather than the government. Private sector banks are registered under the Companies Act and receive their banking licence from the RBI. They are generally more technology-driven, customer-focused and profitable (higher NIM) than public sector banks.

Old Private Sector Banks vs New Private Sector Banks

| Category | Established | Examples |

|---|---|---|

| Old Private Sector Banks | Before 1991 — existed before liberalization | Karnataka Bank, Catholic Syrian Bank, South Indian Bank, Karur Vysya Bank, Lakshmi Vilas Bank, City Union Bank |

| New Private Sector Banks | After 1991 — licensed after liberalization | HDFC Bank, ICICI Bank, Axis Bank, IndusInd Bank, Kotak Mahindra Bank, Yes Bank, IDFC First Bank, Bandhan Bank |

3. Foreign Banks in India

Foreign Banks are banks incorporated outside India that operate in India as branches of their parent organization. They are regulated by RBI under the Banking Regulation Act, 1949. Foreign banks can also operate through Wholly Owned Subsidiaries (WOS) in India.

Key Features of Foreign Banks in India

- Must maintain the same CRR and SLR as domestic banks

- Priority Sector Lending (PSL) norms apply — must lend 40% of ANBC to priority sectors

- Deposits are insured by DICGC up to Rs. 5 lakh like domestic banks

- RBI can restrict the number of branches and ATMs they can open

Major Foreign Banks Operating in India

HSBC, Citibank (now taken over by Axis Bank for retail), Standard Chartered Bank, Deutsche Bank, Barclays Bank, DBS Bank, Bank of America, JPMorgan Chase, BNP Paribas, MUFG Bank, Societe Generale

4. Regional Rural Banks (RRBs)

Regional Rural Banks (RRBs) were established to provide banking and credit facilities to rural areas with a focus on agriculture, small enterprises and weaker sections. They combine the local knowledge of cooperative banks with the commercial efficiency of commercial banks.

| Parameter | Details |

|---|---|

| Established | October 2, 1975 (Gandhi Jayanti) |

| Under Act | Regional Rural Banks Act, 1976 |

| Based on recommendation of | Narasimham Committee, 1975 |

| First RRB | Prathama Bank, Moradabad, Uttar Pradesh (sponsored by Syndicate Bank) |

| Ownership | Central Government 50% + State Government 15% + Sponsoring Bank 35% |

| Focus Area | Rural credit — small farmers, agricultural labourers, artisans, small traders |

| Regulation | Regulated by RBI for banking; NABARD for supervision and refinancing |

Differentiated Banks - New Categories

5. Payment Banks

Payment Banks are a new category of banks introduced by RBI in 2015 based on the recommendations of the Nachiket Mor Committee. They are designed to promote financial inclusion by providing basic financial services — primarily payments and remittances — to the unbanked and underbanked population, especially through mobile phones.

Key Features and Restrictions of Payment Banks

| Feature | Details | |

|---|---|---|

| Maximum deposit limit | Rs. 2 lakh per individual customer | |

| Can offer loans | No — payment banks cannot provide loans or credit cards | |

| Can issue debit cards | Yes — can issue RuPay debit cards | |

| Can issue credit cards | No — strictly prohibited | |

| Where deposits are invested | Must invest minimum 75% of deposits in government securities (SLR) | |

| Minimum capital | Rs. 100 crore paid-up equity capital | |

| Foreign shareholding | As per FDI policy for private sector banks |

Current Payment Banks in India

Airtel Payments Bank, India Post Payments Bank (IPPB), Jio Payments Bank, NSDL Payments Bank, Paytm Payments Bank (had licence issues in 2024), Fino Payments Bank, Fino Payments Bank

6. Small Finance Banks (SFBs)

Small Finance Banks are another new category of banks introduced by RBI in 2015. Unlike payment banks, SFBs are full-service banks — they can both accept deposits and provide loans. They target segments that were previously underserved by mainstream banking — small farmers, micro and small industries, unorganized sector entities.

Key Features of Small Finance Banks

| Feature | Details |

|---|---|

| Can accept deposits | Yes — no upper limit on deposit amounts |

| Can provide loans | Yes — full lending operations permitted |

| Priority sector lending | 75% of adjusted net bank credit must go to priority sectors |

| Small loan requirement | At least 50% of loan portfolio must consist of loans of Rs. 25 lakh and below |

| Minimum capital | Rs. 200 crore paid-up equity capital |

| Focus | Microfinance, small farmers, small businesses, unorganized sector, low-income households |

Examples of Small Finance Banks in India

AU Small Finance Bank, Equitas Small Finance Bank, Ujjivan Small Finance Bank, Jana Small Finance Bank, ESAF Small Finance Bank, Suryoday Small Finance Bank, Utkarsh Small Finance Bank, Capital Small Finance Bank, Northeast Small Finance Bank, Shivalik Small Finance Bank

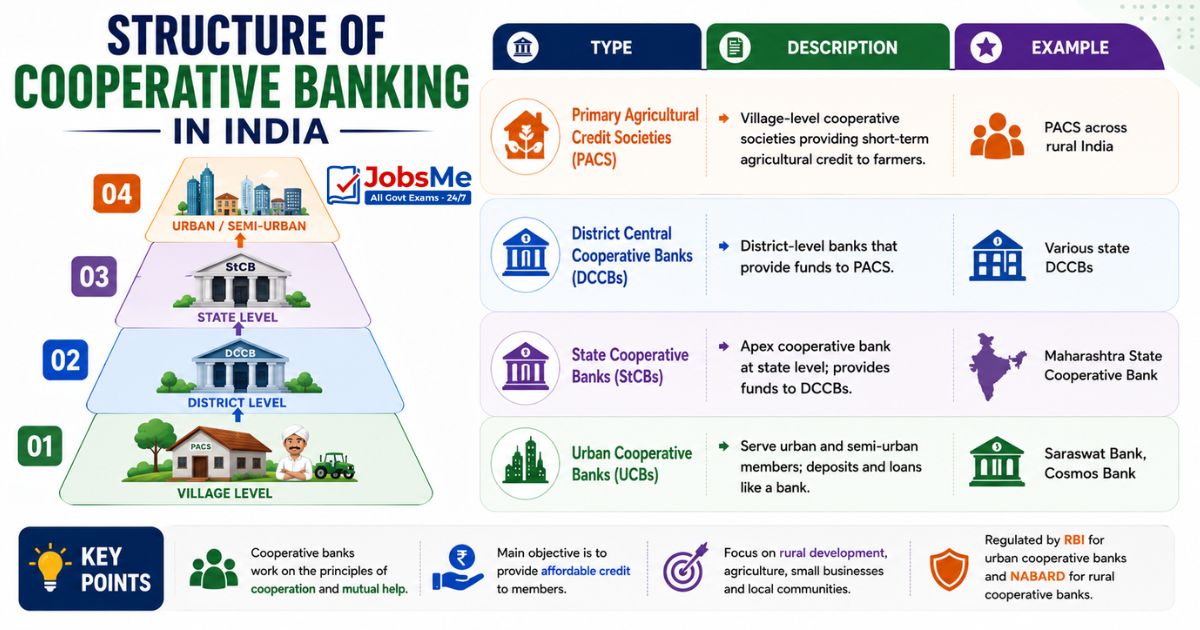

Cooperative Banks in India

Cooperative Banks are financial institutions organized on cooperative principles where members own and control the bank. They serve the banking needs of their members — primarily farmers, small businesses and community groups — at low cost. Cooperative banks operate under a dual regulatory structure:

- RBI regulates their banking functions (deposits, loans, interest rates, KYC)

- Registrar of Cooperative Societies regulates their organizational and governance aspects

Structure of Cooperative Banking in India

| Type | Description | Example |

|---|---|---|

| Primary Agricultural Credit Societies (PACS) | Village-level cooperative societies providing short-term agricultural credit to farmers | PACS across rural India |

| District Central Cooperative Banks (DCCBs) | District-level banks that provide funds to PACS | Various state DCCBs |

| State Cooperative Banks (StCBs) | Apex cooperative bank at state level; provides funds to DCCBs | Maharashtra State Cooperative Bank |

| Urban Cooperative Banks (UCBs) | Serve urban and semi-urban members; deposits and loans like a bank | Saraswat Bank, Cosmos Bank |

Non-Banking Financial Companies (NBFCs) - Key Differences

NBFCs are companies registered under the Companies Act that carry out financial activities like lending, investment and leasing without holding a banking licence. Understanding what NBFCs can and cannot do compared to banks is extremely important for exam questions.

| Parameter | Bank | NBFC |

|---|---|---|

| Accepts demand deposits | Yes — current and savings accounts | No — cannot accept demand deposits |

| Part of payment system | Yes — can issue cheques, participate in RTGS/NEFT | No — not part of payment and settlement system |

| DICGC deposit insurance | Yes — deposits insured up to Rs. 5 lakh | No — no deposit insurance coverage |

| RBI licence required | Yes — mandatory banking licence | No banking licence; registered under Companies Act |

| Can use word bank | Yes | No — strictly prohibited |

| CRR and SLR | Mandatory maintenance | Not required to maintain CRR and SLR |

| Examples | SBI, HDFC Bank, Axis Bank, PNB | Bajaj Finance, Muthoot Finance, L&T Finance, Aditya Birla Finance |

Memory Tricks - Types of Banks

Remember Payment Banks Cannot Lend

Trick: Payment Banks are PAY-only banks. They are designed only to receive and SEND payments — they cannot create credit. Rs. 2 lakh is the deposit limit — think of 2 as the limit for the second-class banking service.

Remember Small Finance Bank PSL Requirement

Trick: SFBs serve Small and Poor = 75% to Priority Sectors. Small Finance Banks must lend 75% to priority sectors — the highest PSL requirement among all bank types. The other key number is 50% of loans must be below Rs. 25 lakh.

Remember RRB Ownership

Trick: 50-15-35 for RRBs. Central Government 50% + State Government 15% + Sponsoring Bank 35% = 100%. The Centre owns the most (50%), the sponsoring bank owns the least (35%) and the state is in the middle (15%).

Remember 12 Public Sector Banks

Trick: SBI is the giant + 11 others = 12 total PSBs. After the 2020 mergers, 27 PSBs reduced to 12. SBI stands alone as the largest. The other 11 are Bank of Baroda, Bank of India, Bank of Maharashtra, Canara Bank, Central Bank, Indian Bank, Indian Overseas Bank, PNB, Punjab and Sind Bank, UCO Bank, Union Bank.

One-Liners for Quick Revision - Types of Banks in India

- Scheduled banks are listed in the Second Schedule of RBI Act 1934.

- Currently there are 12 public sector banks in India after 2020 mergers.

- Government holds more than 50% equity in public sector banks.

- Payment banks can accept deposits up to Rs. 2 lakh per customer.

- Payment banks cannot provide loans or credit cards.

- Small finance banks must lend 75% of ANBC to priority sectors.

- SFBs must lend at least 50% of loan portfolio as loans below Rs. 25 lakh.

- First RRB — Prathama Bank, established October 2, 1975.

- RRB ownership: Central Govt 50% + State Govt 15% + Sponsoring Bank 35%.

- RRBs are supervised by NABARD and regulated by RBI.

- NBFCs cannot accept demand deposits or be part of payment systems.

- DICGC deposit insurance does not cover NBFC deposits.

- Cooperative banks are regulated by both RBI and Registrar of Cooperative Societies.

- The first payment bank licence in India was given to 11 applicants in 2015, of which 6 currently operate.

- Small Finance Banks require minimum paid-up capital of Rs. 200 crore.

- Payment Banks require minimum paid-up capital of Rs. 100 crore.

Preparing for competitive exams requires consistent revision. Platforms like JobsMe simplify preparation through:

- Daily Current Affairs

- Weekly Current Affairs

- Monthly Current Affairs

- Static GK for Competitive Exams

- Latest Government Jobs Notifications

- Computer Awareness

Stay updated, revise regularly, and attempt quizzes for better accuracy in UPSC, SSC CGL, IBPS PO/Clerk, SBI, RBI Grade B, RRB NTPC, Defence, and State PSC exams.

Free quiz • No signup required

Put this topic into practice with Current Affairs Quiz 13–15 June 2026 MCQs for UPSC, SSC, Banking, Railways, Defence & State PSC Exams. It is the quickest way to reinforce what you just learned.

Frequently Asked Questions

What is the difference between scheduled and non-scheduled banks in India?

What is a public sector bank in India?

What is the difference between a payment bank and a small finance bank?

What is an NBFC and how is it different from a bank?

How many public sector banks are there in India currently?

What are Regional Rural Banks (RRBs)?

What is a cooperative bank in India?

About the author