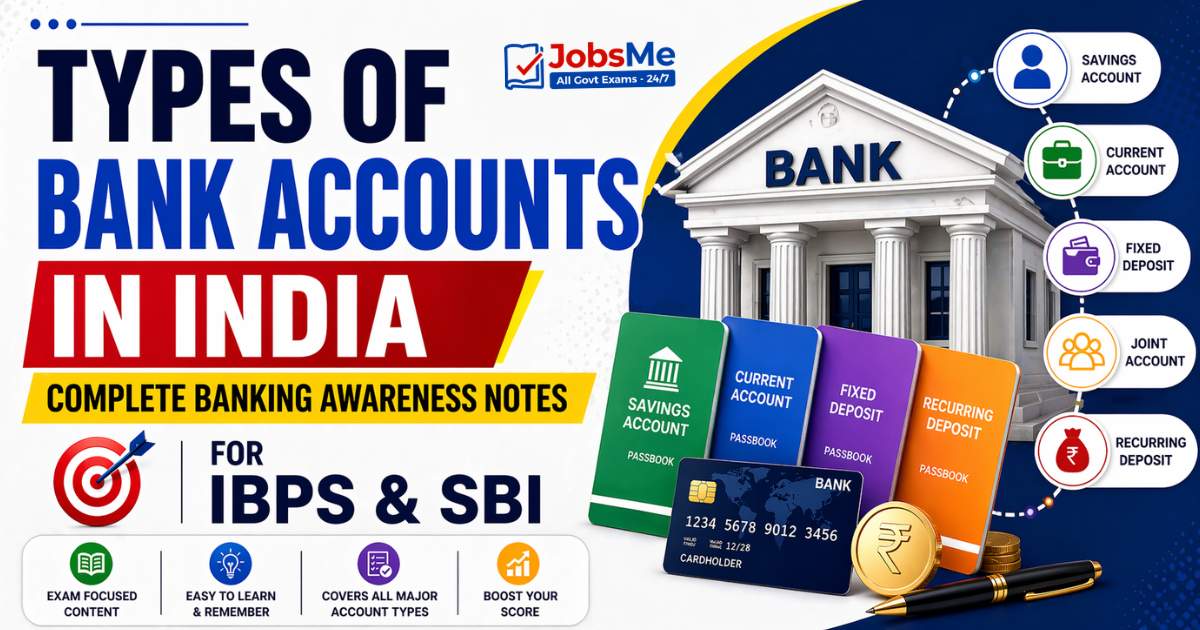

Types of Bank Accounts in India – Complete Banking Awareness Notes 2026 for IBPS and SBI

Types of Bank Accounts is a high-frequency chapter in banking awareness for all competitive banking exams. This chapter covers every type of bank account in India including savings account, current account, fixed deposit, recurring deposit, BSBDA, PMJDY account, small account, bulk deposits, inactive and dormant accounts, special accounts like DEMAT, Escrow and GILT accounts, NRI accounts and the nomination facility. Key features, interest rates, withdrawal limits, TDS rules and exam-relevant differences between account types are covered in detail.

Jump to section

- Types of Bank Accounts in India - Introduction

- 1. Savings Account

- 2. Current Account

- 3. Fixed Deposit (FD)

- 4. Recurring Deposit (RD)

- 5. BSBDA - Basic Savings Bank Deposit Account

- 6. PMJDY Account - Pradhan Mantri Jan Dhan Yojana

- 7. Small Account

- 8. Inactive and Dormant Accounts

- 9. Special Account Types

- 10. NRI Accounts - Detailed Comparison

- 11. Nomination Facility

- Memory Tricks - Types of Bank Accounts

- One-Liners for Quick Revision - Types of Bank Accounts

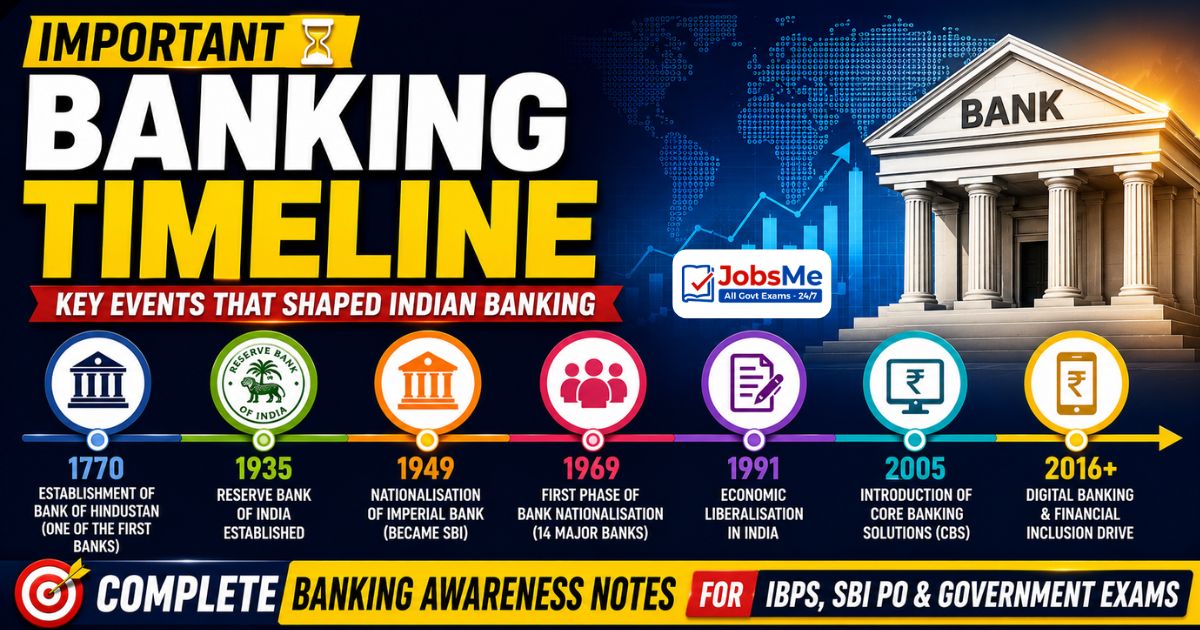

Types of Bank Accounts in India - Introduction

Types of bank accounts is one of the most consistently tested chapters in the banking awareness sections of IBPS PO, IBPS Clerk, SBI PO, SBI Clerk, RBI Grade B and all government banking exams. Understanding each account type — its features, interest rates, transaction limits, tax implications and special conditions — is essential for scoring well in this section. This chapter covers every category of bank account from basic savings accounts to specialized NRI accounts.

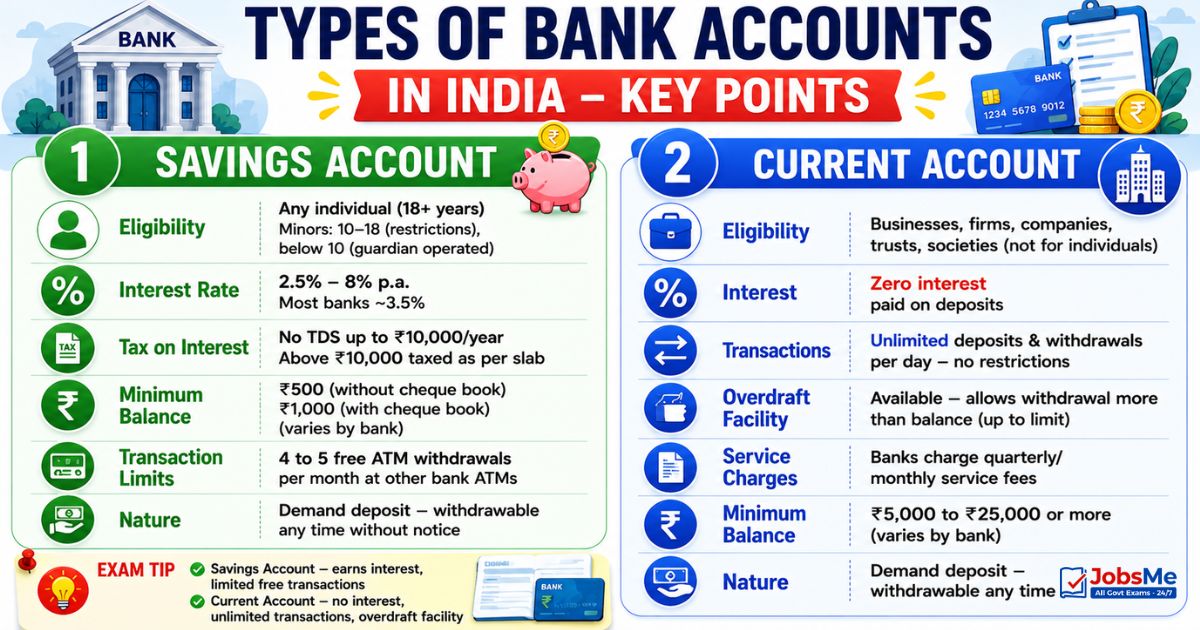

1. Savings Account

A Savings Account is the most commonly held bank account in India. It is designed to encourage savings habits among individuals and small businesses. The key characteristics of a savings account are:

- Eligibility: Any individual resident Indian aged 18 years and above. For minors between 10 and 18 years, accounts with certain restrictions are permitted. Below 10 years, a minor account must be operated by a guardian.

- Interest Rate: Typically 2.5% to 8% per annum depending on the bank. Most banks offer around 3.5%. Interest is calculated on the daily closing balance since April 1, 2020.

- Tax on Interest: No TDS on interest up to Rs. 10,000 per year. Interest above Rs. 10,000 is added to income and taxed as per the applicable slab.

- Minimum Balance: Typically Rs. 500 without a cheque book and Rs. 1,000 with a cheque book — varies by bank.

- Transaction Limits: Banks may restrict the number of free monthly transactions — typically 4 to 5 free ATM withdrawals per month at other bank ATMs.

- Nature: Demand deposit — can be withdrawn at any time without prior notice.

2. Current Account

A Current Account is designed for businesses, firms, companies and other entities that have a high volume and frequency of banking transactions.

- Eligibility: Businesses, firms, companies, trusts, societies — not typically for individual savings purposes.

- Interest: Zero interest paid on current account deposits — this is a critical exam point.

- Transactions: Unlimited deposits and withdrawals per day — no restrictions.

- Overdraft Facility: Current accounts often come with an overdraft facility allowing the business to withdraw more than the account balance up to an approved limit.

- Service Charges: Banks charge quarterly or monthly service fees for current account maintenance.

- Minimum Balance: Typically higher than savings accounts — ranging from Rs. 5,000 to Rs. 25,000 or more depending on the bank and type of current account.

- Nature: Demand deposit — withdrawable at any time.

CASA Ratio - Savings and Current Accounts Combined

The CASA Ratio measures the proportion of a bank's total deposits held in current and savings accounts. Since current accounts pay zero interest and savings accounts pay only about 3.5%, CASA deposits are the cheapest source of funds for a bank. A CASA ratio above 40% is considered healthy. Banks actively try to increase their CASA ratio to improve profitability.

3. Fixed Deposit (FD)

A Fixed Deposit (FD) — also called a Term Deposit or Time Deposit — is a financial instrument where a customer deposits a fixed amount with the bank for a predetermined period and earns a higher interest rate than a savings account.

| Parameter | Details |

|---|---|

| Interest Rate | 4% to 7.25% per annum; higher than savings accounts; senior citizens get additional 0.25% to 0.5% |

| Tenure | 7 days to 10 years |

| Early Withdrawal | Allowed with penalty — typically 0.5% to 1% reduction in the applicable interest rate |

| Loan Against FD | Available up to 85% to 95% of the FD amount including accrued interest |

| TDS Threshold | TDS deducted if interest exceeds Rs. 50,000/year (Rs. 1,00,000 for senior citizens) |

| TDS Rate | 10% with PAN; 20% without PAN |

| Avoid TDS | Submit Form 15G (non-senior citizens) or Form 15H (senior citizens) if income is below taxable limit |

| Bulk Deposit | FD of Rs. 3 crore and above is classified as a bulk deposit with separately negotiated interest rates |

Types of Fixed Deposits

- Standard FD: Interest paid at regular intervals — monthly, quarterly, half-yearly or annually. Principal returned at maturity.

- Cumulative FD: Interest is accumulated and compounded until maturity. Both interest and principal are paid together at the end of the tenure. Earns higher effective yield due to compounding.

- Tax-Saving FD: Tenure of exactly 5 years; eligible for tax deduction under Section 80C of the Income Tax Act up to Rs. 1.5 lakh; early withdrawal not permitted.

- Flexi FD: Linked to a savings account; excess funds above a threshold are automatically converted to FD and broken back when needed.

4. Recurring Deposit (RD)

A Recurring Deposit (RD) is a savings scheme where a customer deposits a fixed amount every month for a predetermined period and earns interest on the accumulated amount.

- Minimum deposit: As low as Rs. 100 per month in most banks

- Tenure: 6 months to 10 years

- Minimum age: 10 years

- Interest rates: 3.5% to 8.5% per annum — similar to FD rates for the same tenure

- TDS: Applicable on interest earned if it exceeds the threshold in a financial year

- Designed for: Small savers who cannot make a lump sum deposit but can commit to regular monthly savings

5. BSBDA - Basic Savings Bank Deposit Account

The BSBDA (Basic Savings Bank Deposit Account) is a zero-minimum-balance savings account introduced by RBI in August 2012, replacing the earlier No-Frills Account scheme introduced in November 2005. BSBDA is designed to bring the unbanked population into the formal banking system.

- Free ATM-cum-debit card without any charges

- No limit on the number of deposits in a month

- Maximum of four withdrawals per month at branches or ATMs (including ATM withdrawals of other banks)

- No minimum balance requirement

- KYC norms must be complied with

- If KYC norms are not fully satisfied, the account is treated as a BSBDA-Small Account

- A customer can hold only one BSBDA in one bank

- If a customer has a BSBDA in a bank, they cannot open any other savings account in the same bank

6. PMJDY Account - Pradhan Mantri Jan Dhan Yojana

The PMJDY Account is a special type of basic savings account introduced under the Pradhan Mantri Jan Dhan Yojana, launched by Prime Minister Narendra Modi on August 28, 2014.

| Feature | Details |

|---|---|

| Minimum Balance | None — zero minimum balance |

| Interest | Interest paid on deposits as per savings account rate |

| Accident Insurance | Rs. 2,00,000 (Rupees two lakh) for all account holders with RuPay card |

| Life Insurance | Rs. 30,000 for accounts opened between August 15, 2014 and January 31, 2015 |

| Overdraft Facility | Rs. 10,000 after 6 months of satisfactory operation — preferably to the lady of the household |

| Debit Card | Free RuPay debit card issued to all account holders |

| Age Limit | 18 to 65 years |

| Mobile Banking | Available including for feature phones via USSD |

7. Small Account

A Small Account is opened when a customer cannot fully satisfy the KYC (Know Your Customer) documentation requirements. It is a restricted account with specific limitations to control risk.

- Aggregate deposits shall not exceed Rs. 1 lakh per annum

- Aggregate withdrawals and transfers in a month shall not exceed Rs. 10,000

- Maximum balance at any point of time shall not exceed Rs. 50,000

- Withdrawals can only be made at the base branch through withdrawal slip

- Foreign remittances cannot be credited without completing full KYC

- Initially valid for 12 months — extendable by another 12 months if proof of OVD (Officially Valid Document) application is provided

- Can only be opened at CBS-linked branches of the bank

8. Inactive and Dormant Accounts

| Status | Condition | What Happens |

|---|---|---|

| Inactive (Inoperative) | No customer-initiated transactions for 12 months | Bank marks account as inactive; interest still credited; customer can reactivate by making a transaction |

| Dormant | No customer-initiated transactions for 24 months | Account further restricted; additional verification required to reactivate |

| Unclaimed Deposits | Deposits unclaimed for more than 10 years | Transferred to RBI's DEAF (Depositor Education and Awareness Fund); can be claimed from RBI via bank |

UDGAM Portal: RBI launched the UDGAM (Unclaimed Deposits Gateway to Access inforMation) portal to help individuals search for their unclaimed deposits across multiple banks. As of July 2025, over 8.59 lakh users had registered on UDGAM.

9. Special Account Types

| Account Type | Description | Key Purpose |

|---|---|---|

| DEMAT Account | Dematerialized account that holds shares, bonds and mutual funds in electronic form | Trading and holding securities without physical share certificates; BSDA (Basic Service Demat Account) limit raised to Rs. 10 lakh in September 2024 |

| Escrow Account | Account held by a neutral third party during a transaction between two parties | Funds held safely until all conditions of a transaction are met — used in real estate, mergers and acquisitions |

| GILT Account | Account maintained by investors with Primary Dealers for holding government securities and treasury bills in Demat form | Enables retail investors to hold government securities electronically through RBI Retail Direct platform |

| Nostro Account | Account that a domestic bank holds in a foreign bank in the foreign currency | Facilitates international trade and foreign exchange settlements; for example HDFC Bank's USD account with Citibank New York |

| Vostro Account | The mirror of a Nostro account — account that a foreign bank holds with a domestic bank in the domestic currency | Same relationship viewed from the other bank's perspective; used in correspondent banking |

10. NRI Accounts - Detailed Comparison

Non-Resident Indians (NRIs) — Indian citizens residing outside India — can maintain three types of bank accounts in India:

| Feature | NRE Account | NRO Account | FCNR(B) Account |

|---|---|---|---|

| Full Form | Non-Resident External Rupee Account | Non-Resident Ordinary Rupee Account | Foreign Currency Non-Resident (Bank) Account |

| Currency | Indian Rupees | Indian Rupees | Foreign currency (USD, EUR, GBP, JPY, CAD, AUD) |

| Source of Funds | Only income earned abroad | Income earned in India — rent, dividends, pension | Only funds remitted from outside India |

| Joint with Resident Indian | No — only with another NRI | Yes — can be joint with resident Indian | No — only with another NRI |

| Tax in India | No income tax on interest | Interest is taxable in India; TDS deducted | No income tax on interest |

| Repatriation | Fully repatriable — principal and interest | Repatriation limited to USD 1 million per year | Fully repatriable — principal and interest |

| Account Types Available | Savings, Current, FD, RD | Savings, Current, FD, RD | Fixed Deposit only |

| Minimum FD Tenure | 1 year | No specific minimum | 1 year; maximum 5 years |

11. Nomination Facility

The Nomination Facility in banking is governed by the Banking Companies (Nomination) Rules, 1985. It allows an account holder to nominate a person who will receive the account balance in case of the account holder's death, without requiring a succession certificate or probate from a court.

- Available for savings accounts, fixed deposits and recurring deposit accounts

- For current accounts, nomination is available only in limited cases

- Highly advisable for every bank account holder to register a nominee

- A nominee is a trustee for the legal heirs — the money can be claimed by legal heirs even after being paid to the nominee

- Maximum of one nominee per account (or per deposit)

- Nomination can be changed or cancelled at any time by the account holder

Memory Tricks - Types of Bank Accounts

Savings vs Current - Simple Rule

Trick: "Save = Interest. Current = No interest." Savings accounts pay interest because you are saving. Current accounts pay no interest because the bank is doing the business owner a favour by managing their constant flow of transactions.

Remember PMJDY Key Numbers

Trick: "PMJDY = 2 lakh accident cover, 10 thousand overdraft, August 28, 2014." The three numbers — Rs. 2 lakh, Rs. 10,000, August 28 (day 28 of month 8) — form a pattern to remember.

Remember NRE vs NRO

Trick: "NRE = Earned abroad, Exempt from tax, Entirely repatriable. NRO = Ordinary Indian income, taxed in india." NRE = all E's (Earned abroad, Exempt, Entire repatriation). NRO = Ordinary, taxable, restricted repatriation.

Remember FCNR

Trick: "FCNR = Foreign Currency, NRI, only Fixed deposits, Rupee exchange not needed." FCNR is the only NRI account held in foreign currency rather than rupees. Only available as fixed deposits. Minimum tenure 1 year, maximum 5 years.

One-Liners for Quick Revision - Types of Bank Accounts

- Savings account interest is calculated on the daily closing balance since April 1, 2020.

- Current accounts pay zero interest on deposits.

- Fixed deposit tenure: 7 days to 10 years.

- Bulk deposit: FD of Rs. 3 crore and above.

- TDS on FD interest if it exceeds Rs. 50,000/year (Rs. 1 lakh for senior citizens).

- Form 15G (non-seniors) and 15H (seniors) avoid TDS on FD interest.

- BSBDA introduced in August 2012 replacing No-Frills Account (November 2005).

- BSBDA withdrawal limit: 4 withdrawals per month.

- PMJDY launched: August 28, 2014 by PM Narendra Modi.

- PMJDY accident insurance: Rs. 2 lakh; overdraft: Rs. 10,000.

- Small account: maximum balance Rs. 50,000; maximum deposits Rs. 1 lakh/year.

- Dormant account: no transactions for 24 months.

- Unclaimed deposits transferred to DEAF (Depositor Education Awareness Fund) after 10 years.

- NRE account: funds earned abroad, fully repatriable, no tax in India.

- NRO account: Indian income, partially repatriable (USD 1 million/year), taxable in India.

- FCNR(B) account: foreign currency FD only; minimum tenure 1 year, maximum 5 years.

- Nomination facility governed by Banking Companies (Nomination) Rules, 1985.

Preparing for competitive exams requires consistent revision. Platforms like JobsMe simplify preparation through:

- Daily Current Affairs

- Weekly Current Affairs

- Monthly Current Affairs

- Static GK for Competitive Exams

- Latest Government Jobs Notifications

- Computer Awareness

Stay updated, revise regularly, and attempt quizzes for better accuracy in UPSC, SSC CGL, IBPS PO/Clerk, SBI, RBI Grade B, RRB NTPC, Defence, and State PSC exams.

Free quiz • No signup required

Put this topic into practice with Current Affairs Quiz 12 June 2026 MCQs for UPSC, SSC, Banking, Railways & State PSC Exams. It is the quickest way to reinforce what you just learned.

Frequently Asked Questions

What is the difference between a savings account and a current account?

What is the CASA Ratio?

What is a Fixed Deposit (FD) and what is the penalty for early withdrawal?

What is a BSBDA account?

What is the difference between inactive and dormant accounts?

What is the TDS rule on Fixed Deposit interest?

What are NRE, NRO and FCNR(B) accounts?

About the author