KYC and ATM Services in India – Banking Awareness Notes 2026 for IBPS and SBI

KYC and ATM Services covers two important sections of the banking awareness syllabus. KYC (Know Your Customer) explains the customer identification and verification process, officially valid documents, periodic verification timelines and the 2025 update allowing Aadhaar Face Authentication. ATM Services covers the full classification of ATMs in India including white label, brown label and biometric ATMs, RBI guidelines on failed transactions, the penalty for delayed reversal, card types including debit, credit, forex and prepaid cards, payment networks including RuPay, Visa and Mastercard, and EMV chip card technology.

Jump to section

KYC - Know Your Customer

KYC (Know Your Customer) is a mandatory due diligence process that banks and financial institutions must carry out to verify the identity and address of their customers before opening any account or providing any financial service. KYC is a critical tool in the fight against money laundering, terrorism financing, identity theft and financial fraud.

Legal Basis for KYC in India

- Section 35A of the Banking Regulation Act, 1949 — Empowers RBI to issue directives to banks on KYC

- Prevention of Money Laundering Act (PMLA), 2002 — Makes KYC mandatory for all regulated entities

- Rule 7 of the Prevention of Money Laundering (Maintenance of Records) Rules, 2005 — Specifies KYC requirements in detail

- RBI Master Direction on KYC — Comprehensive guidelines updated periodically

Objectives of KYC

- Prevent use of the banking system for money laundering and terrorism financing

- Verify the true identity of customers and beneficial owners

- Understand the nature of customers' activities and source of funds

- Protect banks from being used for illegal transactions

- Comply with international AML (Anti-Money Laundering) and CFT (Counter Financing of Terrorism) standards set by FATF

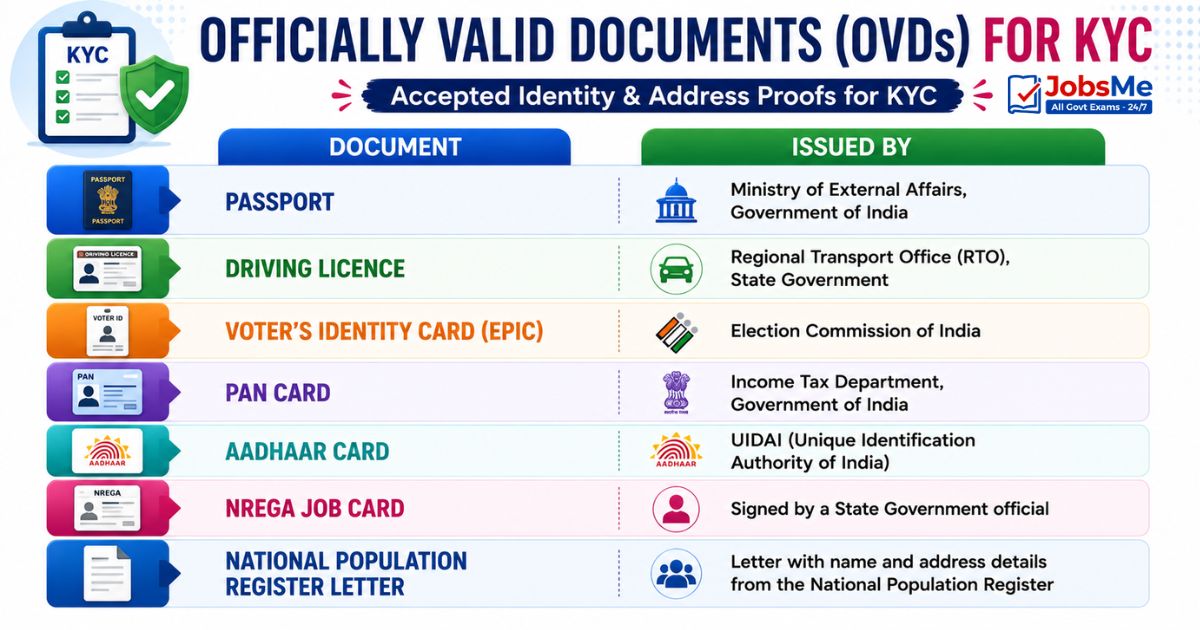

Officially Valid Documents (OVDs) for KYC

| Document | Issued By |

|---|---|

| Passport | Ministry of External Affairs, Government of India |

| Driving Licence | Regional Transport Office (RTO), State Government |

| Voter's Identity Card (EPIC) | Election Commission of India |

| PAN Card | Income Tax Department, Government of India |

| Aadhaar Card | UIDAI (Unique Identification Authority of India) |

| NREGA Job Card | Signed by a State Government official |

| National Population Register Letter | Letter with name and address details from the National Population Register |

KYC Periodic Verification - Risk-Based Approach

| Customer Risk Category | KYC Update Frequency |

|---|---|

| Low Risk | Once every 10 years |

| Medium Risk | Once every 8 years |

| High Risk | Once every 2 years |

2025 KYC Update - Aadhaar Face Authentication

In 2025, the RBI updated KYC norms to allow Aadhaar Face Authentication as a valid KYC method. This enables banks to verify customer identity remotely using the customer's Aadhaar-linked photograph through UIDAI's face authentication API. This is a significant development for digital account opening and reduces the need for physical document verification. The 2025 update also mandated that banks must provide mandatory reasons for KYC rejection and ensure accessibility for Persons with Disabilities (PwDs) in digital KYC systems, following Supreme Court directions.

ATM Services in India

ATMs (Automated Teller Machines) are self-service electronic banking channels that allow customers to perform basic banking transactions without visiting a bank branch. The first ATM in India was introduced by HSBC in Mumbai in 1987.

Basic ATM Services Available

- Cash withdrawal

- Cash deposit (at CDMs — Cash Deposit Machines)

- Account balance inquiry

- Mini statement (last 5 to 10 transactions)

- Fund transfer between linked accounts

- Cheque book request

- Mobile recharge and bill payments

- Fixed deposit creation

- PIN change

Classification of ATMs in India

| ATM Type | Description | Example |

|---|---|---|

| Onsite ATM | Located within bank premises or adjacent to bank branch | ATM inside or just outside any bank branch |

| Offsite ATM | Located away from bank premises — shopping malls, airports, railway stations | ATMs in malls, petrol pumps, hospitals |

| White Label ATM (WLA) | Owned and operated by Non-Banking Financial Companies (NBFCs); no specific bank branding | Indicash (Tata Communications), India One |

| Brown Label ATM | Hardware and ATM lease managed by a service provider; but cash management and network connectivity provided by a sponsor bank; the bank's logo appears on the ATM | Many ATMs operated by third-party vendors on behalf of public sector banks |

| Green Label ATM | Specially designated for agricultural transactions and services for farmers | ATMs in agricultural cooperative or NABARD-linked locations |

| Orange Label ATM | Designated for share and stock market transactions | Used by investors for stock purchase and share transfer transactions |

| Yellow Label ATM | Designed specifically for e-commerce transactions | Online shopping payment terminals |

| Pink Label ATM | Designated exclusively for women customers; monitored by female guards to ensure safety | Women-only ATMs in urban areas |

| Biometric ATM | Uses fingerprint or iris scanner instead of PIN for customer authentication | Used in tribal and rural areas where customers may not remember PINs; connected with Aadhaar |

RBI Guidelines on ATM Transactions

- Failed Transaction Reversal: Banks must reverse failed ATM transactions within T+5 calendar days (T = transaction date). Failure attracts a penalty of Rs. 100 per day of delay.

- Compensation: Automatically credited to the customer's account — no separate claim required for compensation itself, but the initial complaint must be lodged within 30 days.

- Free ATM Transactions: Customers are entitled to a minimum number of free ATM transactions per month — 5 free transactions at own bank ATMs and 3 free transactions at other bank ATMs in metro cities (5 in non-metro cities). Beyond free transactions, banks can charge up to Rs. 21 per transaction (revised from Rs. 20 effective August 2021).

- Interchange Fee: Banks pay an interchange fee of Rs. 17 per financial transaction and Rs. 6 per non-financial transaction between banks when customers use other banks' ATMs.

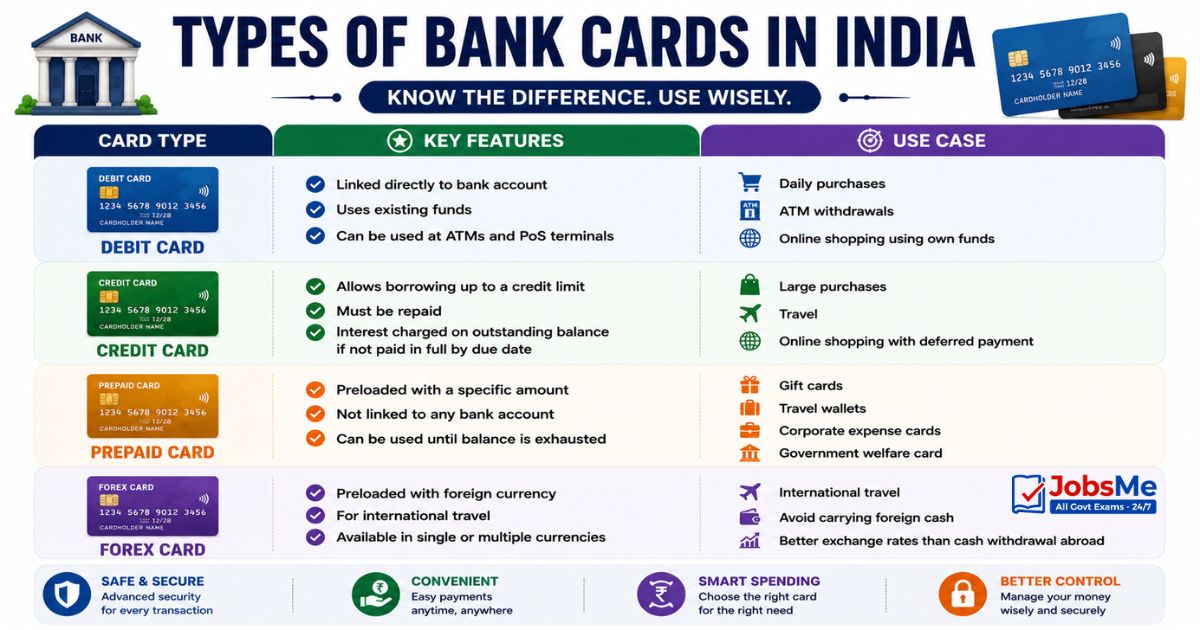

Types of Bank Cards in India

| Card Type | Key Features | Use Case |

|---|---|---|

| Debit Card | Linked directly to bank account; uses existing funds; can be used at ATMs and PoS terminals | Daily purchases, ATM withdrawals, online shopping using own funds |

| Credit Card | Allows borrowing up to a credit limit; must be repaid; interest charged on outstanding balance if not paid in full by due date | Large purchases, travel, online shopping with deferred payment |

| Prepaid Card | Preloaded with a specific amount; not linked to any bank account; can be used until balance is exhausted | Gift cards, travel wallets, corporate expense cards, government welfare card |

| Forex Card | Preloaded with foreign currency; for international travel; available in single or multiple currencies | International travel — avoid carrying foreign cash; better exchange rates than cash withdrawal abroad |

Payment Networks in India and Globally

| Network | Origin | Key Feature |

|---|---|---|

| RuPay | India — developed by NPCI, launched May 8, 2014 | Domestic Indian network; lower transaction cost for banks; accepted internationally via partnerships |

| Visa | USA | World's largest payment network by transactions; widely accepted globally |

| Mastercard | USA | Second largest global payment network; strong in Europe and emerging markets |

| American Express (Amex) | USA | Premium credit card network; higher merchant fees; strong in business and travel segment |

| Diners Club | USA | Charge card (must pay full balance monthly); limited acceptance compared to Visa or Mastercard |

EMV Chip Cards - Security Explained

EMV stands for Europay, Mastercard and Visa — the three companies that created the global standard for chip-based payment cards. EMV chip cards contain a microprocessor chip that generates a unique cryptographic code for every single transaction, making card cloning virtually impossible.

- Each transaction generates a unique cryptogram — old data from one transaction cannot be reused

- Magnetic stripe cards are vulnerable to skimming — a device placed on the card reader captures static data that can be duplicated

- EMV cards make skimming useless — captured data cannot be replicated because each transaction code changes

- In India, RBI mandated migration to chip-and-PIN cards for all debit and credit cards for enhanced security

- Also called smart payment cards or IC (Integrated Circuit) cards

Card Transaction Modes at Point of Sale (PoS)

- Swipe — Magnetic stripe card swiped through the reader; least secure method

- Dip (Insert) — EMV chip card inserted into reader; chip processes the transaction; secure

- Tap (Contactless) — NFC-enabled card tapped on the reader; very fast; secure for low-value transactions; most modern cards and phones support this

Memory Tricks - KYC and ATM Services

Remember OVDs

Trick: "Please Drive Voters to PAN Aadhaar NREGA National." First letters: P (Passport), D (Driving Licence), V (Voters Card), P (PAN), A (Aadhaar), N (NREGA), N (National Population Register) = 7 OVDs.

Remember ATM Types by Color

Trick: White = No bank brand. Brown = Bank logo but third-party hardware. Green = Agriculture (nature). Orange = Stocks (stock market). Yellow = e-commerce (Amazon, Flipkart use yellow). Pink = Women only. Blue = Biometric (fingerprint uses blue digital theme).

Remember Failed ATM Transaction Rule

Trick: T+5 for reversal, Rs. 100/day penalty, 30 days for claim. The numbers 5, 100 and 30 form the key facts about failed ATM transactions. Five days to reverse. Hundred rupees per day if not done. Thirty days to complain.

One-Liners for Quick Revision

- KYC is governed by Section 35A of Banking Regulation Act 1949 and PMLA 2002.

- KYC periodic update: Low risk 10 years, Medium risk 8 years, High risk 2 years.

- There are 7 Officially Valid Documents (OVDs) for KYC in India.

- Aadhaar Face Authentication approved as KYC method in 2025.

- First ATM in India: HSBC, Mumbai, 1987.

- Failed ATM transaction must be reversed in T+5 calendar days.

- Penalty for delay: Rs. 100 per day, automatically credited.

- Customer must complain within 30 days to be eligible for compensation.

- White Label ATMs are owned by NBFCs — example: Indicash.

- Brown Label ATMs — hardware by service provider, cash by sponsor bank.

- RuPay card network developed by NPCI; launched May 8, 2014.

- EMV stands for Europay, Mastercard and Visa.

- EMV chip generates a unique cryptogram per transaction — prevents cloning.

- Three card tap/dip/swipe modes at PoS: Swipe (magnetic), Dip (chip), Tap (NFC contactless).

Series: Complete Banking Awareness Notes 2026 for IBPS PO, IBPS Clerk, SBI PO, SBI Clerk, RBI Grade B, NABARD Grade A, IBPS RRB and all Government Banking Examinations | Jobsme.in

Preparing for competitive exams requires consistent revision. Platforms like JobsMe simplify preparation through:

- Daily Current Affairs

- Weekly Current Affairs

- Monthly Current Affairs

- Static GK for Competitive Exams

- Latest Government Jobs Notifications

- Computer Awareness

Stay updated, revise regularly, and attempt quizzes for better accuracy in UPSC, SSC CGL, IBPS PO/Clerk, SBI, RBI Grade B, RRB NTPC, Defence, and State PSC exams.

Free quiz • No signup required

Put this topic into practice with Current Affairs Quiz 13–15 June 2026 MCQs for UPSC, SSC, Banking, Railways, Defence & State PSC Exams. It is the quickest way to reinforce what you just learned.

Frequently Asked Questions

What is KYC in banking?

What are Officially Valid Documents (OVDs) for KYC?

What is the RBI rule on failed ATM transactions?

What is a White Label ATM?

What is a RuPay card and how is it different from Visa and Mastercard?

What is an EMV chip card?

About the author