Loans and Advances in India – Complete Banking Awareness Notes 2026 for IBPS and SBI

Loans and Advances is one of the most directly tested chapters in banking awareness. This chapter covers every type of credit facility offered by Indian banks — fund-based (overdraft, cash credit, term loans, demand loans, bill discounting, packing credit) and non-fund-based (letters of credit, bank guarantees, co-acceptance), the legal basis for creating security (hypothecation, pledge, mortgage, lien, assignment), all key lending concepts (EMI, moratorium, amortization, DRI scheme, reverse mortgage, ALCO), the complete evolution of India's lending rate benchmarks from BPLR to Base Rate to MCLR to External Benchmark Rate, and a detailed comparison of all four benchmarks.

Jump to section

- Loans and Advances - Introduction

- Fund-Based Credit Facilities - Complete Details

- Non-Fund Based Credit Facilities

- Methods of Creating Security (Charges on Assets)

- Key Lending Concepts — Detailed Explanations

- Evolution of Lending Rate Benchmarks in India

- Special Lending Programmes

- Memory Tricks — Loans and Advances

- One-Liners for Quick Revision

Loans and Advances - Introduction

Loans and Advances represent the primary business of any commercial bank — they constitute the single largest component of bank assets and generate the majority of bank income through interest. When banks deploy depositors' funds into loans, they enable economic activity — businesses finance working capital and capital expenditure, individuals buy homes and vehicles, farmers fund their crop cycle, and governments build infrastructure. Understanding the complete spectrum of credit facilities, security mechanisms and lending rate frameworks is essential for IBPS PO, SBI PO, SBI Clerk, RBI Grade B and all government banking examinations.

Fund-Based Credit Facilities - Complete Details

Fund-Based facilities involve the actual deployment of bank funds — the bank physically lends money to the borrower. The bank's balance sheet expands and the bank bears the credit risk of the loan.

1. Overdraft (OD)

An Overdraft is a pre-approved credit facility linked to a current or savings account that allows the account holder to withdraw more money than is available in the account, up to a pre-sanctioned limit. The account balance can go negative — into the red — up to the overdraft limit.

| Feature | Details |

|---|---|

| Interest charged on | Daily outstanding debit balance only — not on the full sanctioned limit; if the account is in credit, no interest is charged |

| Repayment | Flexible — any credits to the account automatically reduce the outstanding overdraft; no fixed EMI schedule |

| Security types | Fixed deposits (very common — FD overdraft), insurance policies, property, gold, shares, NSC, KVP, salary (for employees) |

| Common users | Businesses for short-term cash flow management; salaried individuals for emergency needs; traders for seasonal funding |

| Revolving nature | Yes — can be drawn, repaid and drawn again repeatedly within the validity period |

2. Cash Credit (CC)

Cash Credit is a specialized working capital facility exclusively for businesses. It is typically secured by the hypothecation of current assets — stock of raw materials, work-in-progress, finished goods, stores and spares, and book debts (outstanding receivables). The maximum drawing limit at any time is based on the Drawing Power (DP) — calculated as a percentage of the value of the hypothecated current assets as declared by the borrower in monthly stock statements.

| Feature | Details |

|---|---|

| Security | Hypothecation of current assets — stock, raw materials, WIP, finished goods, book debts |

| Drawing Power (DP) | Calculated as: (Value of stock + Book debts at 90 days or less) × Margin %; Drawing limit cannot exceed DP even if sanctioned limit is higher |

| Margin | RBI and bank policies set minimum margin requirements — typically 25-40% depending on the commodity category |

| Stock Statement | Borrowers must submit monthly stock statements to the bank for DP calculation |

| Interest | Charged on daily outstanding debit balance only |

| Renewal | CC limits are typically sanctioned for one year and renewed annually after review of the borrower's financial performance |

3. Term Loan

A Term Loan is a loan for a fixed principal amount, disbursed in one or more tranches, and repaid through regular installments (EMI — Equated Monthly Installments or quarterly installments) over a fixed repayment period (tenor).

| Category | Tenor | Common Use |

|---|---|---|

| Short-Term Loan | Up to 1 year | Seasonal working capital, bridge financing |

| Medium-Term Loan | 1 to 5 years | Vehicle loans, equipment purchase, small business expansion |

| Long-Term Loan | 5 to 30 years | Home loans (housing), large infrastructure projects, ship financing |

4. Demand Loan

A Demand Loan is a loan granted for a fixed amount that is repayable on demand by the bank — there is no fixed repayment schedule and the bank can call back the entire amount at any time with a demand notice. Demand loans are typically sanctioned against marketable securities (shares, bonds, gold) where the bank can quickly liquidate the security if the borrower defaults or if the security value falls below the required margin.

5. Bill Discounting (Inland and Export Bills)

Under Bill Discounting, the bank purchases a trade bill (bill of exchange or promissory note) from the seller (drawer/payee) before its due date, at a discount. The bank pays the seller the face value of the bill minus the discount charge (representing interest for the remaining tenor). At maturity, the bank presents the bill to the buyer (drawee/acceptor) and collects the full face value.

- Inland Bill Discounting: Bills drawn by domestic sellers on domestic buyers; governed by the Negotiable Instruments Act 1881

- Export Bill Discounting: Bills drawn by Indian exporters on foreign importers; governed by FEMA and RBI forex regulations; eligible for interest subvention schemes

- LCBD (Letter of Credit Bill Discounting): Discounting of bills drawn under Letters of Credit — considered safer as the issuing bank guarantees payment

6. Packing Credit

Packing Credit is a pre-shipment export finance facility extended to exporters to enable them to procure raw materials, manufacture, process and pack goods for export, against a confirmed export order or Letter of Credit. It is available at concessional interest rates as part of the government's export promotion policy. After the goods are shipped and the export bill is presented, the packing credit is liquidated against the proceeds of the export bill.

7. Hypothecation Loan (Against Vehicle, Machinery)

Under hypothecation, the borrower creates a charge on movable assets in favour of the bank without transferring possession. The borrower retains use of the asset — a business continues using the hypothecated machinery; an individual continues driving the hypothecated car — but cannot sell it without bank consent. If the borrower defaults, the bank can invoke SARFAESI powers to take possession and sell the hypothecated asset.

Non-Fund Based Credit Facilities

Non-Fund Based facilities are contingent commitments — the bank makes a promise and earns a fee (commission), but deploys no funds unless the customer defaults on their obligation. They appear as "off-balance-sheet" contingent liabilities in the bank's books.

1. Letter of Credit (LC)

A Letter of Credit is a financial instrument issued by a bank (the Issuing Bank) on behalf of a buyer (the Applicant) in favour of a seller (the Beneficiary), promising to pay the seller a specified amount upon presentation of specified documents confirming that the goods have been shipped or the service has been delivered as agreed. LCs eliminate the counterparty risk between trading parties — the seller gets the bank's guarantee of payment (removing reliance on the unknown buyer's creditworthiness) and the buyer gets the assurance that the bank will only pay if the seller presents documents proving delivery of goods as specified.

| Parties to an LC | Role |

|---|---|

| Applicant (Buyer) | Requests the bank to issue an LC; pays commission to the bank |

| Issuing Bank | Opens the LC on behalf of the buyer; commits to pay the beneficiary against compliant documents |

| Beneficiary (Seller) | Receives the LC; ships goods/delivers services; presents documents to claim payment |

| Advising Bank | Bank in the seller's country that forwards the LC to the beneficiary; may also confirm the LC |

| Confirming Bank | Adds its own payment guarantee to the LC (optional); used when seller doesn't trust the issuing bank's country risk |

| Negotiating Bank | Purchases the export documents from the beneficiary and presents to the issuing bank for payment |

Governing Rules: LCs are governed internationally by UCP 600 (Uniform Customs and Practice for Documentary Credits, 2007 revision) published by the International Chamber of Commerce (ICC).

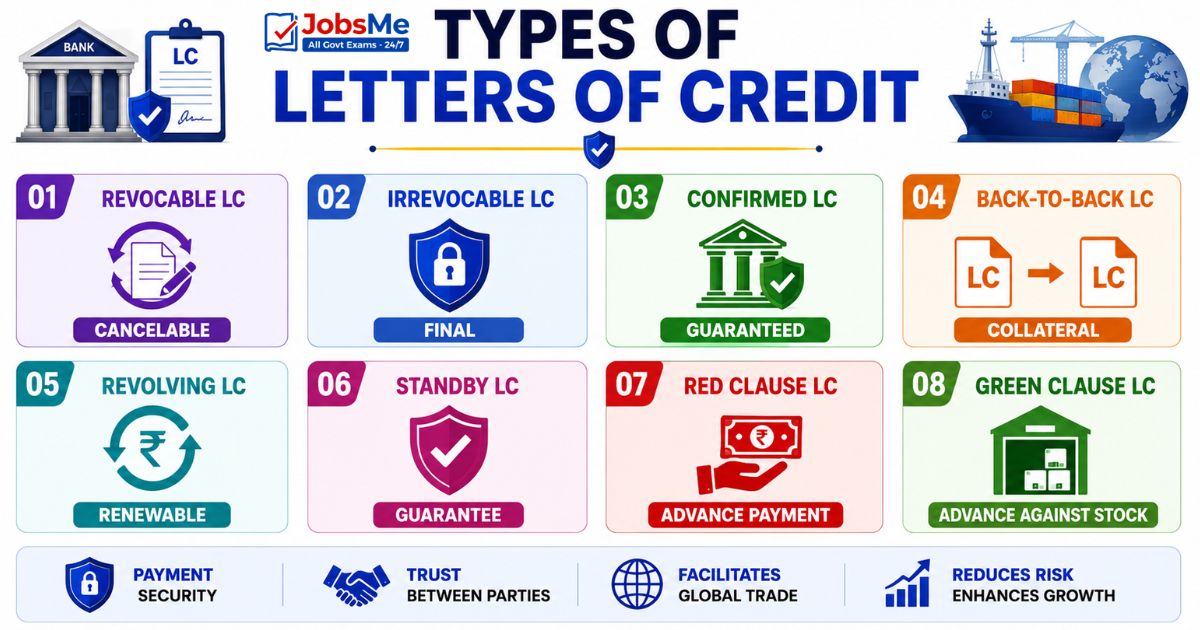

Types of Letters of Credit

| Type | Description |

|---|---|

| Revocable LC | Can be amended or cancelled by the issuing bank at any time without notice to the beneficiary; rarely used; provides little security to seller |

| Irrevocable LC | Cannot be cancelled or amended without the consent of all parties; provides definitive payment assurance to the seller; all modern LCs under UCP 600 are irrevocable by default |

| Confirmed LC | A confirming bank (in seller's country) adds its own payment guarantee — seller can present documents to local confirming bank and receive payment immediately, without waiting for the foreign issuing bank |

| Back-to-Back LC | A second LC opened by an intermediary trader using an existing LC as collateral — enables intermediaries without own funds to complete export transactions |

| Revolving LC | Automatically reinstates to original value after each utilization — suitable for regular repeat transactions between the same buyer and seller |

| Standby LC | Functions as a guarantee — payable only on default by the buyer; not intended for routine payment but as a backup assurance |

| Red Clause LC | Allows seller to receive advance payment (pre-shipment finance) before presenting shipping documents; the clause was historically written in red ink |

| Green Clause LC | Extends the Red Clause concept to allow advances against warehouse receipts for goods already manufactured and stored before shipment |

2. Bank Guarantee (BG)

A Bank Guarantee is a commitment by a bank to pay the beneficiary (the party in whose favour the guarantee is issued) a specified sum of money if the bank's customer (the principal debtor) fails to fulfil their contractual obligation to the beneficiary. Bank guarantees are widely used in commerce and government procurement to ensure contractor performance.

| Type of Bank Guarantee | Purpose | Used In |

|---|---|---|

| Performance Guarantee | Guarantees that the contractor will complete the project as per contract terms | Construction contracts, engineering projects, turnkey projects |

| Financial Guarantee (Payment Guarantee) | Guarantees that the principal will make specified financial payments | Deferred payment guarantees, loan guarantees, payment to suppliers |

| Bid Bond / Tender Guarantee | Guarantees the bidder will honour their bid and sign the contract if selected | Government tenders, large procurement; bidder submits BG with bid |

| Advance Payment Guarantee | Protects the buyer who has paid an advance — if seller fails to deliver, bank refunds the advance | Large equipment purchases, infrastructure projects |

| Retention Money Guarantee | Releases retained amounts (usually 5-10% of project value) held by the employer; contractor submits BG to receive retention money before project warranty period expires | Construction and infrastructure projects |

| Customs Duty Guarantee | Guarantees payment of customs duty on goods imported under deferred payment schemes | Import transactions; in favour of Customs Department |

3. Co-Acceptance of Bills

Under Co-Acceptance, the bank co-signs (co-accepts) a trade bill of exchange drawn by the seller on the buyer. The bank's co-acceptance transforms the bill into a bank-guaranteed instrument, making it easier for the seller to discount the bill in the market at lower discount rates. The bank earns a commission for its co-acceptance and bears the contingent liability of paying if the buyer defaults at maturity.

Methods of Creating Security (Charges on Assets)

When banks extend secured credit, they create a legal charge over the borrower's assets as security. Different types of assets require different types of charges:

| Type of Charge | Assets Covered | Possession Transferred? | Key Point |

|---|---|---|---|

| Hypothecation | Movable assets — stocks, raw materials, machinery, vehicles, receivables | No — borrower retains possession and use | Most common for business working capital (CC/OD); bank relies on borrower's integrity; inspects periodically; SARFAESI can be invoked on default |

| Pledge | Movable assets — gold jewellery, shares, commodities, documents of title to goods | Yes — possession transferred to the bank (bank physically holds the asset) | Bank has direct control; on default bank can sell the pledged asset; common for gold loans and loans against shares |

| Mortgage | Immovable property — land, buildings, flats | Depends on type of mortgage | Most common is Simple Mortgage (borrower promises to sell property on default without transferring possession) and Equitable Mortgage (deposit of title deeds with bank — most used for home loans in India) |

| Lien | Goods or securities already in the bank's possession | Yes — bank already has possession | Bank has the right to retain assets until dues are paid; cannot sell without notice; Banker's Lien extends to all assets of the borrower held by the bank |

| Set-Off | Bank deposits / credit balances in the borrower's own accounts with the bank | N/A — bank debits the account directly | Bank can set off a credit balance in the borrower's savings/FD account against an overdue loan; requires notice in most jurisdictions |

| Assignment | Intangible assets — insurance policies, book debts, fixed deposit receipts, intellectual property rights | Rights transferred, not physical possession | Borrower transfers right to receive proceeds to the bank; life insurance policy assigned to bank as security for home loan is a common example |

Key Lending Concepts — Detailed Explanations

EMI — Equated Monthly Installment

An EMI is a fixed amount paid by the borrower to the bank every month throughout the loan repayment period. Each EMI comprises two components: interest on the outstanding loan balance and repayment of a portion of the principal. In the early months, the interest component is higher (because the outstanding principal is large) and the principal repayment component is lower. As the loan progresses, the outstanding principal reduces with each payment, so the interest component falls and the principal component rises — even though the total EMI amount remains constant. This is called the Reducing Balance method of interest calculation and is used for home loans, auto loans and personal loans.

EMI Formula: EMI = [P × r × (1+r)^n] / [(1+r)^n - 1] where P = Principal, r = Monthly interest rate (annual rate / 12), n = Number of monthly installments

Moratorium

A moratorium is a period at the beginning of a loan during which the borrower is not required to make any principal repayments (and sometimes not even interest payments). Moratoriums are common in education loans (students don't repay while studying), project loans (repayment starts only after the project is commissioned and generating cash flows) and home loans under construction (interest-only payments or full moratorium during construction period).

- Simple Moratorium: No payments at all during the period; interest is capitalized (added to principal)

- Interest Moratorium: No principal repayment; only interest is paid during the period

- RBI COVID-19 Moratorium (March-August 2020): RBI allowed all banks to grant a 6-month EMI moratorium to all retail and MSME borrowers due to the COVID-19 economic disruption — the largest national loan moratorium in India's banking history

Amortization

Amortization is the process of gradually paying off a loan through regular installments over time. A fully amortizing loan is one where the regular payments are sufficient to reduce the principal to zero by the end of the loan tenure — the borrower owes nothing at maturity. Amortization schedules (repayment tables) show the breakdown of each payment into interest and principal components, and the declining outstanding balance over the life of the loan.

Bullet Repayment

In a Bullet Repayment structure, the entire principal is repaid as a single lump sum at the end of the loan tenure. During the tenure, the borrower only makes interest payments. Bullet repayment loans are common in the capital markets (bonds typically pay coupons periodically and return the full face value at maturity) and in some project finance structures.

Balloon Payment

A Balloon Payment loan involves regular payments (usually smaller than full amortization would require) throughout the tenure, followed by a large final "balloon" payment to retire the remaining principal. The balloon payment is larger than regular payments but smaller than a bullet repayment. This structure reduces regular payment burden while ensuring some amortization occurs.

DRI Scheme — Differential Rate of Interest

The Differential Rate of Interest (DRI) scheme is a mandated social lending programme under which banks must extend credit to the most economically disadvantaged sections of society at a concessional flat interest rate of 4% per annum.

| Parameter | Details |

|---|---|

| Interest Rate | 4% per annum flat — regardless of the prevailing market lending rate |

| Mandatory Allocation | Banks must lend at least 1% of their total advances of the previous year under DRI |

| Within DRI | At least 40% of DRI lending must go to SC/ST borrowers |

| Maximum Loan | Rs. 15,000 for agriculture and allied activities; Rs. 15,000 for non-farm activities; Rs. 20,000 for housing |

| Eligible Borrowers | Annual family income ≤ Rs. 18,000 in rural areas; ≤ Rs. 24,000 in urban/semi-urban areas; SC/ST borrowers with slightly relaxed income norms; beneficiaries of government poverty programs |

| Applicable Banks | All public sector banks and private sector banks (not RRBs and cooperative banks under separate schemes) |

Reverse Mortgage Loan

A Reverse Mortgage Loan is designed for senior citizens aged 60 years and above who own residential property. Instead of the conventional loan where the borrower receives a lump sum and makes monthly payments, in a Reverse Mortgage the bank makes regular monthly payments to the senior citizen borrower and the loan is repaid from the property after the borrower's death or permanent vacating of the property.

| Parameter | Details |

|---|---|

| Eligible Borrowers | Senior citizens aged 60 years and above; for joint applicants, spouse aged 55+ is allowed |

| Maximum Monthly Payment | Rs. 50,000 per month |

| Maximum Loan Tenor | 20 years |

| Loan-to-Value | Up to 90% of the property value (RML-specific LTV guidelines from NHB) |

| Repayment | No repayment during borrower's lifetime while occupying property; loan repaid from property sale proceeds after death or vacation |

| Heirs' rights | Heirs can repay the bank and retain the property; if heirs do not repay, the bank sells the property; any surplus after repayment goes to heirs |

| Governed by | National Housing Bank (NHB) guidelines; RBI Circular on Reverse Mortgage for Senior Citizens 2007 |

ALCO — Asset Liability Management Committee

The ALCO is a mandatory senior management committee in every bank, responsible for managing the structural risks arising from mismatches between the bank's assets and liabilities in terms of interest rate sensitivity, maturity profile and currency. Key responsibilities of ALCO include:

- Setting deposit and lending rate pricing strategy in response to RBI policy changes and market conditions

- Managing the bank's interest rate risk in the banking book (IRRBB) — ensuring that interest rate movements don't adversely squeeze the bank's Net Interest Margin (NIM)

- Managing liquidity risk — ensuring the bank always has sufficient liquid assets to meet funding obligations

- Monitoring the Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR) compliance

- Reviewing the maturity profile of assets (loans, investments) and liabilities (deposits, borrowings) to identify and manage gaps

- Reporting to the Board's Risk Management Committee on balance sheet risk

Evolution of Lending Rate Benchmarks in India

The interest rate at which banks lend has evolved through four distinct phases in India — each change made lending rates more transparent and responsive to RBI monetary policy decisions.

| Benchmark | Period | Basis of Calculation | Key Problem |

|---|---|---|---|

| BPLR (Benchmark Prime Lending Rate) | Before July 1, 2010 | Each bank computed its own BPLR based on average cost of funds plus margin; no standardized formula; banks could lend below BPLR to large corporates | Completely opaque; massive sub-BPLR lending to large corporates; retail and small borrowers cross-subsidized corporate lending; RBI policy rate changes had almost no effect on lending rates |

| Base Rate | July 1, 2010 - March 31, 2016 | Standardized RBI formula: average cost of funds + negative carry on CRR and SLR + operating expenses + profit margin; banks cannot lend below Base Rate except specified exemptions | Based on average (not marginal) cost of funds — average cost changes slowly; when RBI cut repo rate, banks were slow to reduce Base Rate; poor monetary policy transmission |

| MCLR (Marginal Cost of Funds Based Lending Rate) | April 1, 2016 - September 30, 2019 | Four components: Marginal cost of funds (92% marginal borrowing + 8% return on equity) + Negative carry on CRR + Operating costs + Tenor premium; published monthly for all standard tenures | Improved but still an internal benchmark with bank discretion; one-year maximum reset period meant borrowers waited up to 12 months for benefits of RBI rate cuts; transmission incomplete |

| External Benchmark Rate (EBR) | October 1, 2019 onwards | Mandatory link to external, publicly observable benchmark: RBI Repo Rate (chosen by most banks), 91-day T-Bill yield, 182-day T-Bill yield, or any FBIL rate; reset mandatory every 3 months | Most transparent; fastest and most complete monetary policy transmission; when RBI changes repo rate, borrowers benefit within the next reset cycle (maximum 3 months) |

Who Still Uses Base Rate and MCLR?

The EBR mandate applies to all new floating rate retail loans and MSME loans sanctioned from October 1, 2019 onwards. Existing loans linked to BPLR, Base Rate or MCLR continue to operate under those benchmarks until the borrower exercises the option to switch to EBR (usually subject to a one-time conversion fee). Banks are required to provide existing borrowers the option to switch to EBR on mutually agreeable terms.

Special Lending Programmes

| Programme | Description | Key Exam Point |

|---|---|---|

| Consortium Lending | Multiple banks jointly finance a single large borrower — one bank is the lead bank (consortium leader) and others participate; used when the loan is too large for a single bank's prudential exposure limits | Lead bank coordinates appraisal, documentation and monitoring; individual banks share risk proportionally to their participation |

| Syndicated Lending | Similar to consortium lending but more formal structure; an arranger bank markets the loan to other banks globally; each participant lender has a direct legal relationship with the borrower; more flexible than consortium | Common for very large international loans; loan agreement is a single document; each bank funds its share independently |

| Bridge Loan | Short-term loan to bridge a funding gap — typically to cover an immediate payment need while permanent financing (equity issue, term loan) is being arranged | Short tenor, higher interest rate; repaid when permanent financing arrives |

| Take-out Financing | An arrangement where the long-term lender (typically an infrastructure finance institution) agrees in advance to take out (purchase) the loan from a bank after a specified period — allowing banks to provide long-term project financing without locking up funds permanently | Developed to help Indian banks fund long-tenor infrastructure projects; promoted by IIFCL (India Infrastructure Finance Company Limited) |

| Microfinance Loans | Very small loans (typically Rs. 10,000 to Rs. 3 lakh) to low-income borrowers — often women in rural and semi-urban areas — through Self-Help Group (SHG) or Joint Liability Group (JLG) models; no collateral required; repaid weekly or fortnightly | Regulated by RBI under NBFC-MFI framework; interest rate cap applies; qualifying assets: loan to single borrower not exceeding Rs. 3 lakh |

Memory Tricks — Loans and Advances

Remember Fund vs Non-Fund Based

Trick: Fund-Based = Bank GIVES money (OD, CC, Term Loan, Bill Discounting). Non-Fund Based = Bank PROMISES money (LC, BG). When you GIVE, funds flow. When you PROMISE, only the word flows — funds flow only on default. GIVE vs PROMISE.

Remember Types of Security

Trick: HPM = Hypothecation (movable, NO possession transfer), Pledge (movable, possession transferred), Mortgage (Immovable property). H-P-M, like HiPpoMouse — H for Hypo (movable no transfer), P for Pledge (movable with transfer), M for Mortgage (immovable).

Remember LC Types

Trick: All modern LCs under UCP 600 are IRREVOCABLE by default. Confirmed = double guarantee (issuing bank + confirming bank). Revolving = automatically refills. Red Clause = advance before shipment (written in red historically).

Remember MCLR Components

Trick: MNOT — Marginal cost of funds, Negative carry on CRR, Operating costs, Tenor premium. "Must Not Overlook These" four components when calculating MCLR.

Remember Benchmark Evolution

Trick: BPLR → Base Rate (July 2010) → MCLR (April 2016) → EBR (October 2019). Each step = more transparent + faster transmission. Date pattern: 2010, 2016, 2019.

One-Liners for Quick Revision

- Overdraft: withdrawal beyond balance; interest on daily utilized amount only; linked to current/savings account.

- Cash Credit: working capital; drawing limit based on current assets (stock + book debts); interest on daily balance.

- Term Loan: fixed amount; fixed tenure; repaid through regular EMIs; for capital expenditure.

- Demand Loan: repayable on demand by bank; no fixed schedule; against marketable securities.

- Bill Discounting: bank buys bill at discount; collects full face value at maturity; immediate liquidity to seller.

- LC governed by UCP 600 (International Chamber of Commerce rules).

- All LCs under UCP 600 are irrevocable by default.

- BG types: Performance, Financial, Bid Bond, Advance Payment, Retention Money, Customs Duty.

- Hypothecation: movable assets; no possession transfer to bank.

- Pledge: movable assets; possession transferred to bank.

- Mortgage: immovable property; equitable mortgage (title deed deposit) most common in India.

- Assignment: intangible assets — insurance policies, book debts, FD receipts.

- EMI: fixed monthly payment = interest + principal; reducing balance method.

- DRI scheme: flat 4% per annum; banks must lend 1% of total advances under DRI.

- DRI within SC/ST: at least 40% of DRI lending to SC/ST borrowers.

- Reverse Mortgage: for seniors aged 60+; max payment Rs. 50,000/month; max tenor 20 years; governed by NHB.

- ALCO manages: interest rate risk, liquidity risk, currency risk in the bank's balance sheet.

- BPLR: replaced by Base Rate on July 1, 2010.

- Base Rate: replaced by MCLR on April 1, 2016.

- EBR mandatory: from October 1, 2019; reset every 3 months; linked to Repo Rate.

- Most banks chose RBI Repo Rate as their external benchmark under EBR.

Preparing for competitive exams requires consistent revision. Platforms like JobsMe simplify preparation through:

- Daily Current Affairs

- Weekly Current Affairs

- Monthly Current Affairs

- Static GK for Competitive Exams

- Latest Government Jobs Notifications

- Computer Awareness

Stay updated, revise regularly, and attempt quizzes for better accuracy in UPSC, SSC CGL, IBPS PO/Clerk, SBI, RBI Grade B, RRB NTPC, Defence, and State PSC exams.

Free quiz • No signup required

Put this topic into practice with Current Affairs Quiz 13–15 June 2026 MCQs for UPSC, SSC, Banking, Railways, Defence & State PSC Exams. It is the quickest way to reinforce what you just learned.

Frequently Asked Questions

What is the difference between a term loan and a cash credit?

What is the difference between an overdraft and a cash credit?

What is a Non-Fund Based credit facility?

What is the DRI scheme?

What is a Reverse Mortgage Loan?

What is Bill Discounting?

What is the ALCO and what does it do?

About the author