NRI Accounts in India – NRE NRO FCNR and Special Accounts | Banking Awareness 2026

NRI Accounts and Special Accounts covers all bank account types relevant to Non-Resident Indians and special-purpose accounts tested in banking awareness sections. This chapter explains the full comparison between NRE (Non-Resident External), NRO (Non-Resident Ordinary) and FCNR(B) (Foreign Currency Non-Resident Bank) accounts including currency, tax treatment, repatriation limits and tenure. Special accounts covered include Nostro, Vostro, DEMAT, Escrow and GILT accounts. The chapter also covers DTAA, LRS and remittance statistics important for exam-level awareness.

Jump to section

NRI Accounts - Introduction

Non-Resident Indians (NRIs) have special banking needs — they earn income in foreign countries, need to maintain connections with India through financial assets, and require accounts that facilitate both foreign currency management and Indian rupee operations. RBI has established three specific types of accounts for NRIs to cater to these diverse needs. Understanding the differences between NRE, NRO and FCNR(B) accounts is a must for banking awareness sections in all competitive examinations.

Who is an NRI?

For banking purposes, a Non-Resident Indian (NRI) is an Indian citizen who:

- Resides outside India for employment, business or vocation in circumstances indicating an indefinite or long-term stay abroad, OR

- Has been outside India for more than 182 days during the preceding financial year

- Holds a valid Indian passport (or is a Person of Indian Origin — PIO)

An existing resident Indian account automatically becomes an NRO account when the account holder acquires NRI status by going abroad for the long term.

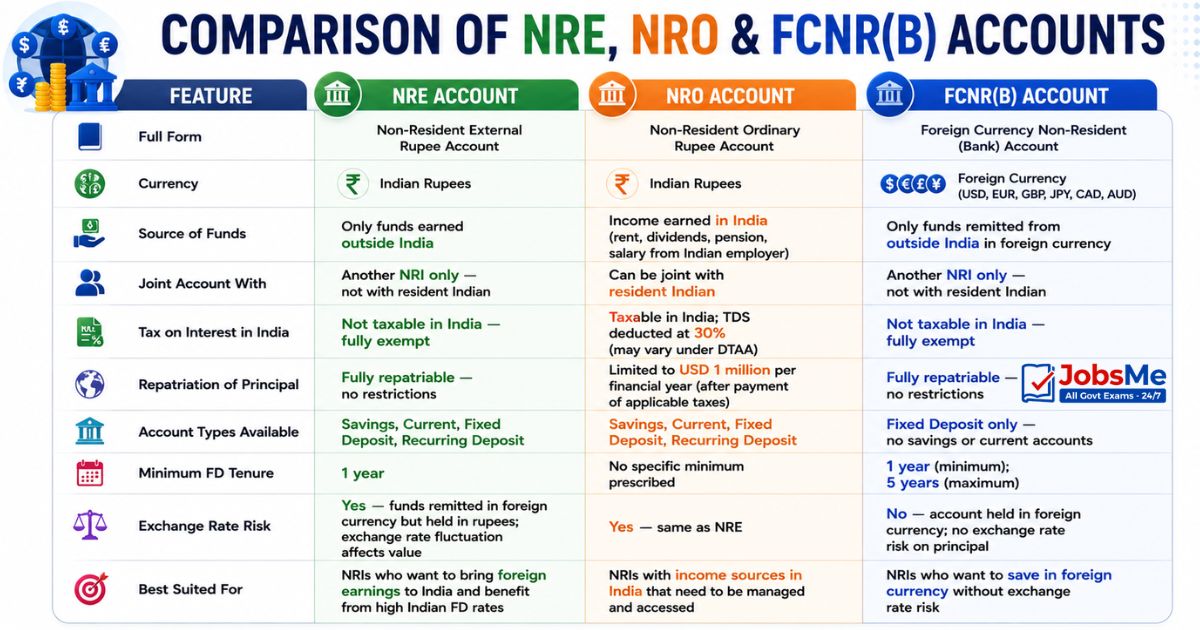

Comparison of NRE, NRO and FCNR(B) Accounts

| Feature | NRE Account | NRO Account | FCNR(B) Account |

|---|---|---|---|

| Full Form | Non-Resident External Rupee Account | Non-Resident Ordinary Rupee Account | Foreign Currency Non-Resident (Bank) Account |

| Currency | Indian Rupees | Indian Rupees | Foreign Currency (USD, EUR, GBP, JPY, CAD, AUD) |

| Source of Funds | Only funds earned outside India | Income earned in India (rent, dividends, pension, salary from Indian employer) | Only funds remitted from outside India in foreign currency |

| Joint Account With | Another NRI only — not with resident Indian | Can be joint with resident Indian | Another NRI only — not with resident Indian |

| Tax on Interest in India | Not taxable in India — fully exempt | Taxable in India; TDS deducted at 30% (may vary under DTAA) | Not taxable in India — fully exempt |

| Repatriation of Principal | Fully repatriable — no restrictions | Limited to USD 1 million per financial year (after payment of applicable taxes) | Fully repatriable — no restrictions |

| Account Types Available | Savings, Current, Fixed Deposit, Recurring Deposit | Savings, Current, Fixed Deposit, Recurring Deposit | Fixed Deposit only — no savings or current accounts |

| Minimum FD Tenure | 1 year | No specific minimum prescribed | 1 year (minimum); 5 years (maximum) |

| Exchange Rate Risk | Yes — funds remitted in foreign currency but held in rupees; exchange rate fluctuation affects value | Yes — same as NRE | No — account held in foreign currency; no exchange rate risk on principal |

| Best Suited For | NRIs who want to bring foreign earnings to India and benefit from high Indian FD rates | NRIs with income sources in India that need to be managed and accessed | NRIs who want to save in foreign currency without exchange rate risk |

Special Account Types

Nostro Account

A Nostro Account is a bank account that a domestic bank holds in a foreign bank, denominated in the foreign bank's currency. The word "Nostro" comes from Latin meaning "ours." Nostro accounts are used to facilitate foreign exchange settlements, international trade payments and cross-border remittances.

Example: HDFC Bank's US Dollar account held with Citibank New York is HDFC Bank's Nostro account. When HDFC needs to make a USD payment to a US company, it uses its Nostro account balance.

Vostro Account

A Vostro Account is the mirror image of a Nostro account — it is the account that a foreign bank holds with an Indian bank in Indian rupees. The word "Vostro" comes from Latin meaning "yours." From the Indian bank's perspective, the foreign bank's account held with it is a Vostro account.

Example: Citibank's Indian Rupee account held with HDFC Bank in Mumbai is Citibank's Vostro account (and HDFC's Nostro from Citibank's perspective). Special Rupee Vostro Accounts (SRVAs) were introduced by RBI in 2022 to facilitate trade settlements in Indian Rupees — AD Category-I banks can now open SRVAs without prior RBI approval (updated in August 2025).

DEMAT Account

A DEMAT (Dematerialized) Account is an electronic account that holds shares, bonds, mutual fund units and other securities in digital form, eliminating the need for physical share certificates. DEMAT accounts are maintained by depositories — NSDL (National Securities Depository Limited) and CDSL (Central Depository Services Limited) — through Depository Participant (DP) banks and brokers.

- BSDA (Basic Service Demat Account): For small investors; SEBI raised the BSDA eligibility limit from Rs. 2 lakh to Rs. 10 lakh portfolio value effective September 1, 2024

- Required for trading in stocks and bonds on NSE (National Stock Exchange) and BSE (Bombay Stock Exchange)

- RBI's Retail Direct platform allows government securities (G-Secs) to be held in a GILT account — a type of DEMAT account for government bonds

Escrow Account

An Escrow Account is a temporary account held by a neutral third party (the escrow agent — typically a bank or legal entity) during a transaction between two parties. The funds are held safely in escrow until all conditions of the transaction are fulfilled, at which point they are released to the appropriate party.

- Commonly used in real estate transactions — buyer deposits purchase money in escrow; released to seller only when title is clear

- Used in mergers and acquisitions — acquisition consideration held in escrow pending regulatory approvals

- Used in government infrastructure projects to ensure contractor payment security

GILT Account

A GILT Account is maintained by investors with Primary Dealers (PDs) for holding government securities (G-Secs) and treasury bills in Dematerialized form. Through RBI's Retail Direct Scheme, individual retail investors can open a GILT account directly with the RBI to buy and sell government securities without any intermediary.

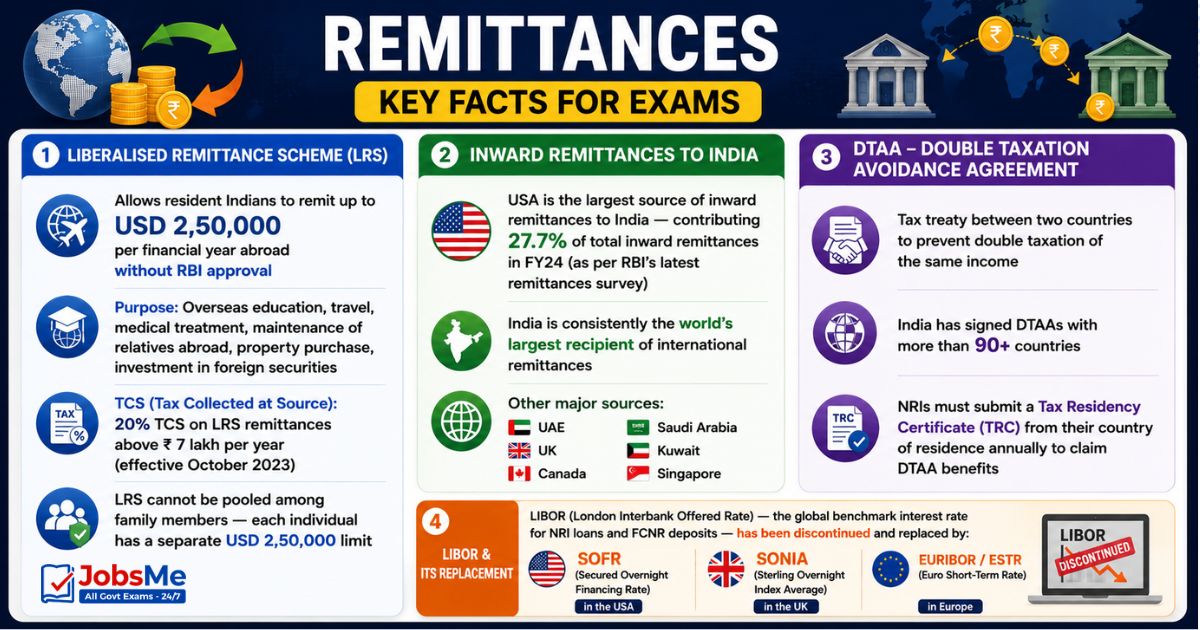

Remittances - Key Facts for Exams

Liberalised Remittance Scheme (LRS)

- Allows resident Indians to remit up to USD 2,50,000 per financial year abroad without RBI approval

- Purpose: Overseas education, travel, medical treatment, maintenance of relatives abroad, property purchase, investment in foreign securities

- TCS (Tax Collected at Source): 20% TCS on LRS remittances above Rs. 7 lakh per year (effective October 2023)

- LRS cannot be pooled among family members — each individual has a separate USD 2,50,000 limit

Inward Remittances to India

- USA is the largest source of inward remittances to India — contributing 27.7% of total inward remittances in FY24 (as per RBI's latest remittances survey)

- India is consistently the world's largest recipient of international remittances

- Other major sources: UAE, UK, Canada, Saudi Arabia, Kuwait, Singapore

DTAA - Double Taxation Avoidance Agreement

- Tax treaty between two countries to prevent double taxation of the same income

- India has signed DTAAs with more than 90 countries

- NRIs must submit a Tax Residency Certificate (TRC) from their country of residence annually to claim DTAA benefits

- LIBOR (London Interbank Offered Rate) — the global benchmark interest rate for NRI loans and FCNR deposits — has been discontinued and replaced by SOFR (Secured Overnight Financing Rate) in the USA, SONIA in the UK and EURIBOR/ESTR in Europe

Memory Tricks - NRI Accounts

NRE vs NRO - Three E's Rule

Trick: NRE has three E's — Earnings from abroad, Exempt from tax, Entirely repatriable. NRO = Ordinary Indian income, taxed, Only USD 1 million repatriation.

FCNR Unique Feature

Trick: FCNR = Foreign Currency, No Rupee risk. The only NRI account held in foreign currency. No exchange rate risk. Only Fixed Deposits. Minimum 1 year, maximum 5 years.

Nostro vs Vostro

Trick: Nostro = OUR account with THEM. Vostro = THEIR account with US. From the Indian bank's view: money held with a foreign bank = Nostro (our money with them). Foreign bank's money held with Indian bank = Vostro (their money with us).

One-Liners for Quick Revision

- NRE account: funds earned abroad; fully repatriable; interest not taxable in India.

- NRO account: Indian income like rent/dividends; repatriation limited to USD 1 million/year; interest taxable in India.

- FCNR(B) account: only Fixed Deposits in foreign currency; minimum tenure 1 year; maximum 5 years.

- NRE and FCNR(B) accounts can only be joint with another NRI — not with resident Indians.

- NRO account can be held jointly with a resident Indian.

- Nostro = domestic bank's account in foreign bank in foreign currency.

- Vostro = foreign bank's account in Indian bank in Indian rupees.

- BSDA eligibility limit raised to Rs. 10 lakh by SEBI effective September 1, 2024.

- LRS limit for resident Indians: USD 2,50,000 per financial year.

- USA is the largest source of inward remittances to India (27.7% in FY24).

- LIBOR replaced by SOFR (USD), SONIA (GBP), EURIBOR/ESTR (EUR).

- DTAA — India signed with more than 90 countries; NRIs must submit TRC annually.

Series: Complete Banking Awareness Notes 2026 for IBPS PO, IBPS Clerk, SBI PO, SBI Clerk, RBI Grade B, NABARD Grade A, IBPS RRB and all Government Banking Examinations | Jobsme.in

Preparing for competitive exams requires consistent revision. Platforms like JobsMe simplify preparation through:

- Daily Current Affairs

- Weekly Current Affairs

- Monthly Current Affairs

- Static GK for Competitive Exams

- Latest Government Jobs Notifications

- Computer Awareness

Stay updated, revise regularly, and attempt quizzes for better accuracy in UPSC, SSC CGL, IBPS PO/Clerk, SBI, RBI Grade B, RRB NTPC, Defence, and State PSC exams.

Free quiz • No signup required

Put this topic into practice with Current Affairs Quiz 13–15 June 2026 MCQs for UPSC, SSC, Banking, Railways, Defence & State PSC Exams. It is the quickest way to reinforce what you just learned.

Frequently Asked Questions

What is an NRI for banking purposes?

What is the difference between NRE and NRO accounts?

Can an NRI open a joint account with a resident Indian?

What is FCNR(B) account and who can open it?

What is a Nostro account?

What is the Liberalised Remittance Scheme (LRS)?

What is DTAA?

About the author