Financial Markets, FDI and FPI – Complete Banking Awareness Notes 2026 for IBPS, SBI PO and RBI Grade B

Financial Markets, FDI and FPI covers all aspects of India's financial market ecosystem that are tested in banking awareness exams. Topics include money market instruments (T-Bills, Cash Management Bills, Commercial Paper, Certificate of Deposit, Call Money, Notice Money, TREPS), capital market instruments (equity, debentures, government securities, mutual funds), SEBI's role and structure, the FDI vs FPI comparison, types of foreign investment, Balance of Payments (BoP), Capital Account and Current Account, GIFT City International Financial Services Centre, FII vs FPI distinction and the Liberalised Remittance Scheme (LRS).

Jump to section

- Financial Markets - Introduction and Classification

- Money Market Instruments - Detailed Coverage

- Capital Market - Instruments and Structure

- SEBI - Securities and Exchange Board of India

- Foreign Investment - FDI and FPI Detailed Comparison

- Balance of Payments (BoP)

- GIFT City - India's International Financial Services Centre

- LRS - Liberalised Remittance Scheme

- Important Market Indices

- Memory Tricks - Financial Markets

- One-Liners for Quick Revision

Financial Markets - Introduction and Classification

A financial market is a platform where buyers and sellers of financial assets — securities, currencies, commodities — interact to determine prices and transfer ownership. Financial markets perform the critical economic function of channeling savings from those who have surplus funds into productive investments by those who need funds. They are classified primarily into two broad categories based on the maturity of instruments traded.

| Feature | Money Market | Capital Market |

|---|---|---|

| Maturity of Instruments | Less than 1 year (short-term) | More than 1 year (long-term) |

| Instruments | T-Bills, CP, CD, Call Money, TREPS | Equity shares, bonds, G-Secs, debentures |

| Risk Level | Low — short tenure, mostly government-backed | Higher — long tenure, market risk and credit risk |

| Return | Lower — commensurate with lower risk | Higher potential — commensurate with higher risk |

| Primary Regulator | Reserve Bank of India (RBI) | Securities and Exchange Board of India (SEBI) |

| Purpose | Short-term liquidity management; working capital financing | Long-term capital raising; infrastructure and business financing |

| Participants | Banks, corporates, NBFCs, mutual funds, primary dealers | Corporates, FIIs/FPIs, retail investors, institutional investors |

Money Market Instruments - Detailed Coverage

1. Treasury Bills (T-Bills)

| Parameter | Details |

|---|---|

| Issuer | Government of India; auctioned by RBI on behalf of the government |

| Tenures | 91-day, 182-day and 364-day |

| Nature | Zero-coupon instruments — issued at a discount to face value; no periodic interest payment; redeemed at face value at maturity |

| Return | The difference between the issue price (discount) and the face value received at maturity is the investor's return |

| Risk | Zero credit risk — backed by the full faith and credit of the Government of India |

| Auction | RBI conducts weekly auctions; yields are market-determined; 91-day T-Bill yield is a key benchmark rate |

| Who Buys | Banks (SLR maintenance), insurance companies, mutual funds, provident funds, foreign portfolio investors |

| Exam Note | 91-day T-Bill yield is one of the approved external benchmarks for EBR (External Benchmark Rate) for bank loans |

2. Cash Management Bills (CMBs)

- Short-term government borrowing instruments with maturity of less than 91 days

- Issued by the Government of India through RBI to meet temporary cash flow mismatches in government receipts and payments

- Not issued on a regular schedule — issued as and when needed

- Zero-coupon like T-Bills; issued at discount; redeemed at face value

- Not part of the government's market borrowing program — purely a cash management tool

3. Commercial Paper (CP)

| Parameter | Details |

|---|---|

| Definition | An unsecured short-term promissory note issued by highly rated corporates, NBFCs and Primary Dealers to raise working capital directly from the market |

| Maturity | Minimum 7 days to maximum 1 year |

| Eligible Issuers | Listed companies with minimum net worth of Rs. 100 crore; NBFCs; All-India Financial Institutions; Primary Dealers |

| Credit Rating | Must have minimum P2 rating from an approved credit rating agency (CRISIL, ICRA, CARE, FITCH) |

| Nature | Issued at discount; redeemed at face value; no periodic coupon payments |

| Denomination | Minimum denomination of Rs. 5 lakh; issued in multiples of Rs. 5 lakh |

| Purpose | Cheaper source of short-term working capital for corporates compared to bank loans; bypasses bank intermediation |

| Key Advantage | Corporates can access funds at money market rates (cheaper than bank lending rates) if they have a high credit rating |

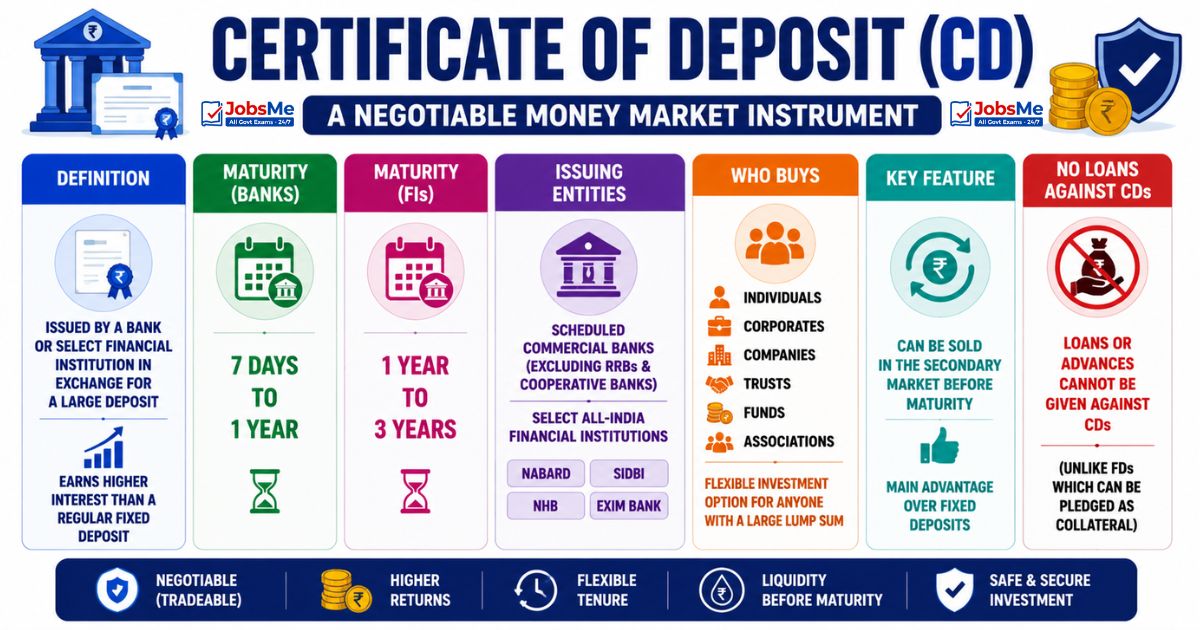

4. Certificate of Deposit (CD)

| Parameter | Details |

|---|---|

| Definition | A negotiable (tradeable) money market instrument issued by a bank or select financial institution in exchange for a large deposit; earns higher interest than a regular fixed deposit |

| Maturity (Banks) | 7 days to 1 year |

| Maturity (FIs) | 1 year to 3 years |

| Issuing Entities | Scheduled commercial banks (excluding RRBs and cooperative banks) and select All-India Financial Institutions (NABARD, SIDBI, NHB, EXIM Bank) |

| Who Buys | Individuals, corporates, companies, trusts, funds, associations — CDs are a flexible investment option for anyone with a large lump sum |

| Key Feature | Can be sold in the secondary market before maturity — unlike regular FDs which cannot be transferred. This liquidity is the main advantage over FDs |

| No Loans Against CDs | Loans or advances cannot be given against CDs (unlike FDs which can be pledged as collateral) |

5. Call Money and Notice Money

| Feature | Call Money | Notice Money |

|---|---|---|

| Tenure | Overnight (1 day) | 2 to 14 days |

| Participants | Banks and Primary Dealers only | Banks and Primary Dealers only |

| Collateral | Uncollateralized — no security required | Uncollateralized — no security required |

| Rate | Call Rate — market-determined overnight rate; fluctuates within LAF corridor (Reverse Repo to MSF) | Market-determined rate for 2-14 day borrowings |

| Purpose | Banks with CRR/SLR shortfalls or sudden liquidity needs borrow; banks with surplus funds lend | Same as call money but for slightly longer periods |

| RBI Role | RBI monitors and publishes call rates; intervenes through LAF operations if call rates deviate too far | Same monitoring by RBI |

6. TREPS - Tri-Party Repo

- Full Form: Tri-Party Repo System

- Replaced CBLO (Collateralized Borrowing and Lending Obligation) from November 2018

- A collateralized overnight to short-term (up to 90 days) borrowing and lending instrument — unlike call money which is uncollateralized

- Three parties: the borrower (pledges G-Secs as collateral), the lender (provides funds) and CCIL (Clearing Corporation of India Limited) as the tri-party agent (central counterparty that manages collateral).

- CCIL guarantees all TREPS transactions — so it is effectively risk-free from counterparty default perspective

- Open to a wider range of participants than call money — banks, NBFCs, mutual funds, insurance companies, corporates can all participate

- Most liquid short-term money market segment after call money; key reference rate for overnight secured lending

Capital Market - Instruments and Structure

Primary Market vs Secondary Market

| Feature | Primary Market | Secondary Market |

|---|---|---|

| Definition | Market where new securities are issued for the first time; companies raise fresh capital directly from investors | Market where already-issued securities are bought and sold between investors; company does not receive any new funds |

| Instruments | IPOs (Initial Public Offerings), FPOs (Follow-on Public Offerings), Rights Issues, Private Placements | Trading of stocks and bonds on NSE, BSE and other exchanges |

| Price | Fixed by the company (or through book building process) | Determined by demand and supply forces in the market |

| Liquidity | Low — investor must wait for allotment | High — can buy or sell at any time during trading hours |

Capital Market Instruments

| Instrument | Description | Risk Level | Returns |

|---|---|---|---|

| Equity Shares | Ownership stake in a company; shareholders vote on company decisions; receive dividends (variable) and capital appreciation | Highest — market-linked; can lose entire investment | Potentially highest — no upper limit |

| Preference Shares | Hybrid security — gets preference over equity shares in dividend payment and in case of company liquidation; fixed dividend; typically no voting rights | Lower than equity; higher than debt | Fixed dividend; no capital appreciation beyond redemption value |

| Debentures | Long-term debt instrument of a company; pays fixed interest (coupon) to holders; does not give ownership stake | Medium — depends on company's creditworthiness | Fixed coupon (interest) |

| Bonds | Long-term debt instruments; issued by governments, PSUs and corporates; pays periodic coupon; principal repaid at maturity | Low to medium | Fixed coupon; tax-free bonds earn tax-free interest |

| Government Securities (G-Secs) | Long-term debt securities issued by central and state governments; no credit risk; most secure fixed-income investment; used by banks for SLR compliance | Zero credit risk (sovereign) | Market-determined coupon; price fluctuates with interest rates |

| Mutual Funds | Pooled investment vehicles that invest in diversified portfolios; NAV-based; multiple categories: equity, debt, hybrid, index, ELSS | Varies by fund type | Market-linked; not guaranteed |

| ETFs (Exchange Traded Funds) | Funds that track an index (like Nifty 50 or Sensex); traded on stock exchange like a share; low cost | Same as underlying index | Index returns minus expense ratio |

| REITs (Real Estate Investment Trusts) | Investment vehicle for real estate; listed on exchanges; distributes 90% of income to unit holders; regulated by SEBI | Medium | Regular rental income + capital appreciation |

| InvITs (Infrastructure Investment Trusts) | Investment vehicle for infrastructure assets (roads, pipelines, power plants); listed on exchanges; regular income distribution; regulated by SEBI | Medium | Infrastructure revenue distributions |

SEBI - Securities and Exchange Board of India

| Parameter | Details |

|---|---|

| Established | April 12, 1992 under the SEBI Act 1992 (initially set up as non-statutory body in 1988) |

| Headquarters | Mumbai (Bandra Kurla Complex) |

| Type | Statutory autonomous body — neither government department nor court; quasi-judicial, quasi-legislative, quasi-executive |

| Regional Offices | New Delhi, Kolkata, Chennai, Ahmedabad |

| Board Composition | Chairman (government nominee) + 2 members from Ministry of Finance + 1 from RBI + 5 other members |

SEBI's Three Functions

- Quasi-Legislative: Issues regulations, guidelines and circulars governing all market participants

- Quasi-Judicial: Adjudicates disputes; can impose penalties and ban market participants; orders can be appealed to Securities Appellate Tribunal (SAT)

- Quasi-Executive: Conducts investigations, inspections and enforcement actions; can attach bank accounts and properties of offenders

What SEBI Regulates

- Stock exchanges: NSE (National Stock Exchange) — Nifty 50 index; BSE (Bombay Stock Exchange) — Sensex; MCX (commodity futures)

- Brokers, sub-brokers and trading members

- Depositories: NSDL (National Securities Depository Limited) and CDSL (Central Depository Services Limited)

- Mutual funds, Portfolio Management Services (PMS), Investment Advisers

- Merchant bankers, underwriters, registrar to an issue

- Credit Rating Agencies: CRISIL, ICRA, CARE, FITCH India, Brickwork

- Alternate Investment Funds (AIFs): Category I (infrastructure, venture capital), Category II (private equity, debt), Category III (hedge funds)

- REITs and InvITs

Foreign Investment - FDI and FPI Detailed Comparison

| Parameter | FDI (Foreign Direct Investment) | FPI (Foreign Portfolio Investment) |

|---|---|---|

| Definition | Long-term investment by a foreign entity acquiring a significant and lasting interest in a business enterprise — typically 10% or more equity — with intent of management control | Investment by a foreign entity in Indian financial securities (stocks, bonds, mutual fund units) with purely financial return motive; no management control intended |

| Nature | Long-term; real economy investment (physical assets, technology, employment) | Short to medium term; financial securities; can be very short-term (hot money) |

| Management Control | Yes — FDI investor gets board representation and management involvement | No — FPI investor is a passive financial investor; no voting rights sought |

| Equity Threshold | 10% or more equity ownership (OECD/IMF definition) | Less than 10% equity holding in any company (SEBI FPI regulations) |

| Stability | Stable — real assets cannot be quickly liquidated; committed long-term presence | Volatile — can exit very quickly; large sudden FPI outflows cause currency depreciation and stock market crashes |

| Impact on Economy | Creates jobs, transfers technology, builds productive capacity; supplements domestic savings for real investment | Provides liquidity and price discovery in capital markets; does not directly create jobs or build productive capacity |

| Regulator | DPIIT (Department for Promotion of Industry and Internal Trade) for policy; RBI for FEMA compliance; CCI for competition issues | SEBI for equity and debt investments in markets; RBI for certain debt investment limits |

| Route | Automatic Route (pre-approved sectors, no government approval needed) or Government Route (approval from DIPP/concerned ministry) | Registration as Registered Foreign Portfolio Investor (RFPI) with a SEBI-designated depository participant |

| Formerly Called | FDI | FII (Foreign Institutional Investor) — term changed to FPI by SEBI in 2014 to align with global standards |

| Examples | Samsung's factory in Noida; Foxconn's manufacturing in India; Walmart's acquisition of Flipkart stake of 77% | Foreign mutual funds, pension funds, sovereign wealth funds buying Reliance or HDFC Bank shares on NSE |

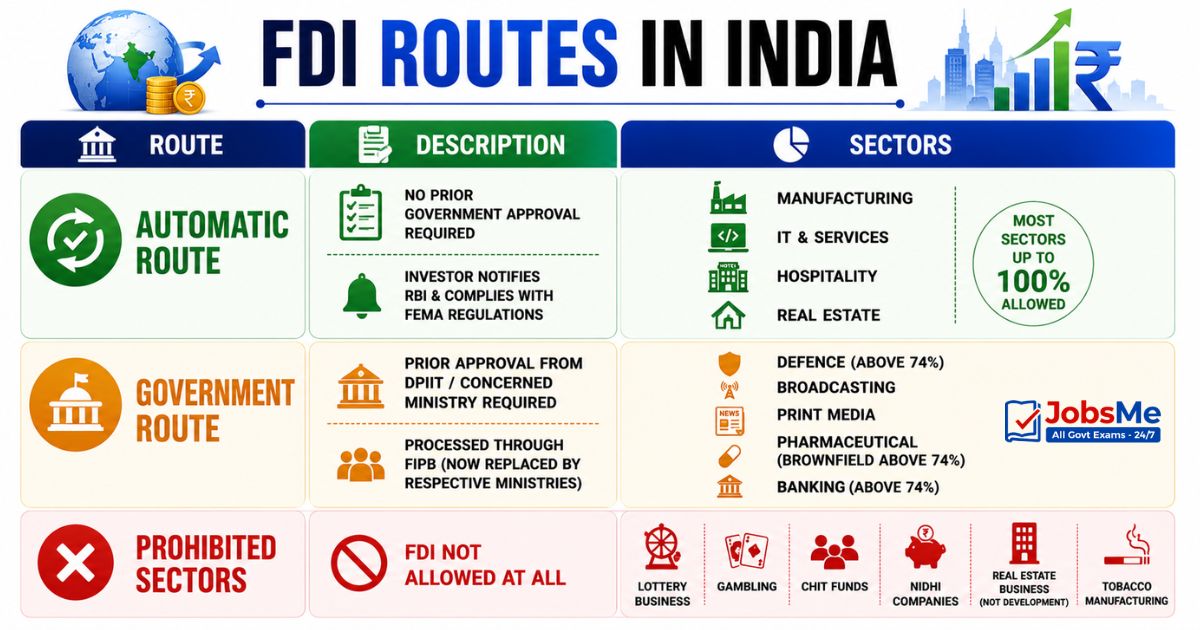

FDI Routes in India

| Route | Description | Sectors |

|---|---|---|

| Automatic Route | No prior government approval required; investor only needs to notify RBI and comply with FEMA regulations; covers most sectors | Manufacturing, IT, services, hospitality, real estate (most sectors up to 100% allowed) |

| Government Route | Prior approval from DPIIT / concerned ministry required before making investment; processed through FIPB (now replaced by respective ministries) | Defence (above 74%), broadcasting, print media, pharmaceutical (brownfield above 74%), banking (above 74%) |

| Prohibited Sectors | FDI not allowed at all | Lottery business, gambling, chit funds, Nidhi companies, real estate business (not development), tobacco manufacturing |

Balance of Payments (BoP)

The Balance of Payments (BoP) is a systematic record of all economic transactions between residents of a country and the rest of the world during a given period (typically one year). It reflects the country's international financial position.

Structure of BoP

| Account | What It Records | Examples |

|---|---|---|

| Current Account | Trade in goods and services, primary income and secondary income (transfers) | Export/import of goods; software exports; tourism earnings; NRI remittances; dividend income from abroad |

| Current Account — Merchandise (Visible Trade) | Export and import of physical goods | Petroleum imports; electronics imports; engineering goods exports; pharma exports |

| Current Account — Invisibles (Services + Transfers) | Services, investment income and transfers | IT/BPM service exports; interest payments on external debt; NRI remittances |

| Capital and Financial Account | Cross-border flows of financial assets — investments, loans, banking capital | FDI, FPI, ECB (External Commercial Borrowings), banking capital flows, official reserve changes |

| Errors and Omissions | Statistical discrepancy; balancing item | Unrecorded transactions; estimation errors |

Current Account Deficit (CAD)

India typically runs a Current Account Deficit (CAD) — imports of goods and services exceed exports. This CAD is financed by net inflows in the Capital and Financial Account (FDI, FPI, ECB, NRI deposits). When capital inflows are insufficient to cover CAD, India draws on its foreign exchange reserves to meet the gap.

- India's current account deficit is primarily driven by the large oil import bill and gold imports

- IT/software exports and NRI remittances are the two largest sources of foreign exchange for India, partially offsetting the trade deficit

- India is the world's largest recipient of remittances — NRI remittances exceed USD 100 billion per year

GIFT City - India's International Financial Services Centre

| Parameter | Details |

|---|---|

| Full Name | Gujarat International Finance Tec-City |

| Location | Gandhinagar, Gujarat |

| Status | India's first and only operational International Financial Services Centre (IFSC) |

| Regulator | International Financial Services Centres Authority (IFSCA) — established under IFSCA Act 2019; unified regulator for all financial services in GIFT City IFSC |

| Currency | All transactions in foreign currencies (USD primarily); no Indian Rupee transactions |

| Key Features | Banking, insurance, capital markets and fund management allowed; liberalised regulatory regime; significant tax incentives (10-year tax holiday for units) |

| Purpose | Capture offshore financial transactions involving India that currently happen in Singapore, Dubai, Mauritius and London — bring them back to India |

| NSE and BSE Presence | Both NSE (India International Exchange — INX) and BSE (India International Exchange — India INX) have exchanges at GIFT City IFSC |

LRS - Liberalised Remittance Scheme

| Parameter | Details |

|---|---|

| Introduced | 2004 by RBI |

| Who Can Use | Resident individual Indians (not companies or firms) |

| Annual Limit | USD 2,50,000 per financial year per person |

| Permissible Uses | Foreign education, medical treatment abroad, travel, purchase of foreign securities, opening foreign bank accounts, gifts to foreign relatives, maintenance of close relatives abroad |

| Prohibited Under LRS | Remittance to countries under FATF watch, remittance for lottery, prohibited investments |

| TCS on LRS | Tax Collected at Source applies on LRS remittances — 20% TCS on remittances above Rs. 7 lakh per year (except education and medical treatment which have lower TCS rates); TCS is adjustable against income tax |

| Route | Must be through an Authorized Dealer (AD) bank in India |

Important Market Indices

| Index | Exchange | Composition | Base Year |

|---|---|---|---|

| Sensex | BSE (Bombay Stock Exchange) | 30 largest and most actively traded stocks on BSE | 1979 (Base value 100) |

| Nifty 50 | NSE (National Stock Exchange) | 50 largest companies by market capitalization across 13 sectors | 1995 (Base value 1000) |

| Nifty Bank | NSE | 12 most liquid and large-cap banking stocks listed on NSE | 2000 |

| BSE 100 / BSE 200 | BSE | 100 / 200 largest companies by market cap on BSE | Various |

Memory Tricks - Financial Markets

Remember Money Market Instruments

Trick: T-C-C-N-T = T-Bills, Commercial Paper, Certificate of Deposit, Notice/Call Money, TREPS. Five instruments, starting with T-C-C-N-T. "The Corporation Calls No Trouble" — each first letter matches.

Remember FDI vs FPI

Trick: FDI = Direct = Durable = Factories = Develops economy. FPI = Portfolio = Paper assets = Passive = Potentially volatile. The D in FDI stands for "Direct, Durable, Develops." The P in FPI stands for "Portfolio, Passive, Potentially-hot-money."

Remember TREPS vs Call Money

Trick: Call = Uncollateralized. TREPS = Collateralized (uses G-Secs as collateral; CCIL is middle-man). Call is risky (no collateral); TREPS is safe (G-Sec backed). CBLO was the old name before TREPS replaced it in November 2018.

Remember SEBI

Trick: SEBI = April 12, 1992. Established 4+1+2=7 (12 April). Headquarters: Mumbai. Three functions: Legislative (makes rules), Judicial (punishes violators), Executive (investigates). Quasi means "sort of" — SEBI acts like all three but is not formally any of them.

Remember BoP Accounts

Trick: BoP = Current Account (goods, services, transfers) + Capital Account (investments, loans). Current = what you currently earn and spend. Capital = long-term financial flows. India: Current Account Deficit (spends more on imports than earns from exports); financed by Capital Account surplus (FDI, FPI, ECB inflows).

One-Liners for Quick Revision

- Money market: instruments with maturity under 1 year; regulated by RBI.

- Capital market: instruments with maturity over 1 year; regulated by SEBI.

- T-Bills: 91-day, 182-day, 364-day; zero-coupon; issued at discount; risk-free.

- 91-day T-Bill yield is an approved External Benchmark Rate (EBR) for bank loans.

- CMBs: maturity less than 91 days; for government cash flow mismatches.

- Commercial Paper: unsecured; issued by highly rated corporates, NBFCs, PDs; 7 days to 1 year.

- Certificate of Deposit: issued by banks; tradeable in secondary market; cannot pledge for loans.

- Call Money: overnight; uncollateralized; only banks and PDs.

- TREPS replaced CBLO in November 2018; CCIL is the tri-party agent.

- SEBI established: April 12, 1992; headquarters Mumbai.

- SEBI: quasi-legislative, quasi-judicial, quasi-executive.

- NSE index: Nifty 50; BSE index: Sensex (30 stocks).

- NSDL and CDSL are India's two depositories regulated by SEBI.

- FDI: long-term, real assets, management control; routes: Automatic or Government.

- FPI: short-term, financial assets, no management control; formerly called FII.

- FPI limit in any company: less than 10% equity (above 10% classified as FDI).

- GIFT City: Gandhinagar, Gujarat; regulated by IFSCA.

- LRS limit: USD 2,50,000 per resident Indian per financial year.

- LRS: TCS at 20% on remittances above Rs. 7 lakh/year (excluding education and medical).

- India: world's largest recipient of NRI remittances — over USD 100 billion per year.

Preparing for competitive exams requires consistent revision. Platforms like JobsMe simplify preparation through:

- Daily Current Affairs

- Weekly Current Affairs

- Monthly Current Affairs

- Static GK for Competitive Exams

- Latest Government Jobs Notifications

- Computer Awareness

Stay updated, revise regularly, and attempt quizzes for better accuracy in UPSC, SSC CGL, IBPS PO/Clerk, SBI, RBI Grade B, RRB NTPC, Defence, and State PSC exams.

Free quiz • No signup required

Put this topic into practice with Current Affairs Quiz 20 June 2026 | UPSC, SSC, Banking, Railways & State PSC MCQs with Answers. It is the quickest way to reinforce what you just learned.

Frequently Asked Questions

What is the difference between the Money Market and the Capital Market?

What is the difference between FDI and FPI?

What is SEBI and what does it regulate?

What is GIFT City and why is it significant for banking?

What is the Liberalised Remittance Scheme (LRS)?

What is the Balance of Payments (BoP)?

About the author