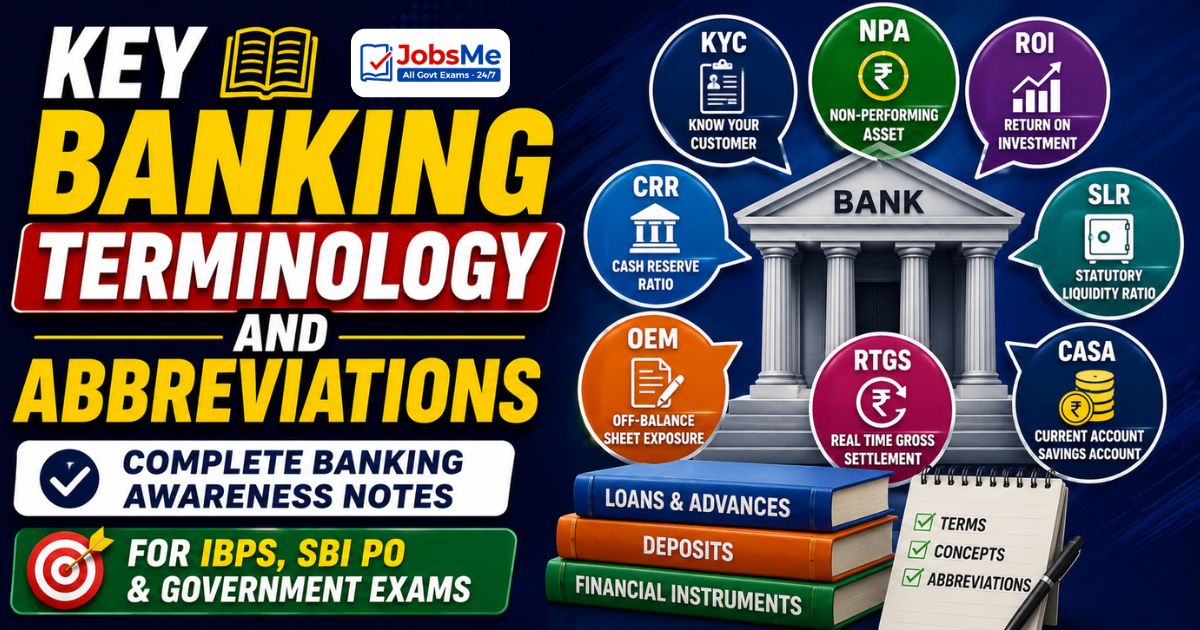

Basel Norms — Basel I, II and III — Complete Banking Awareness Notes 2026 for IBPS and SBI

Basel Norms covers the three international capital adequacy frameworks issued by the Basel Committee on Banking Supervision (BCBS) under the Bank for International Settlements (BIS). This chapter explains Basel I (1988, credit risk, 8% CAR), Basel II (2004, three pillars — minimum capital, supervisory review and market discipline, operational and market risk added), and Basel III (2010, post-financial crisis reform — LCR, NSFR, leverage ratio, capital conservation buffer, countercyclical buffer, CET1). India's specific requirements (9% CAR, 5.5% CET1) and the D-SIB surcharge are also covered with all exam-relevant detail.

Jump to section

- Basel Norms — Introduction and Historical Background

- Basel Committee on Banking Supervision (BCBS) — Key Facts

- Basel I (1988) — The First Capital Accord

- Basel II (2004) — Three Pillars Framework

- Basel III (2010-2017) — Post-Financial Crisis Comprehensive Reform

- Comparison of Basel I, II and III

- Memory Tricks — Basel Norms

- One-Liners for Quick Revision — Basel Norms

Basel Norms — Introduction and Historical Background

Banking crises have historically caused tremendous economic damage — destroying savings, disrupting credit flows, requiring costly government bailouts and sometimes triggering recessions. After the collapse of Herstatt Bank in Germany in 1974 — which caused significant disruption in international foreign exchange settlements — the G10 central bank governors established the Basel Committee on Banking Supervision (BCBS) under the Bank for International Settlements (BIS) in Basel, Switzerland.

The BCBS has since issued three progressively more comprehensive international capital and liquidity frameworks — collectively called the Basel Accords or Basel Norms. These are not laws — they are international standards that member countries voluntarily adopt through their own regulatory processes. India's RBI implements Basel Norms for all scheduled commercial banks and has in many cases applied even more conservative requirements than the global minimums.

Basel Committee on Banking Supervision (BCBS) — Key Facts

| Parameter | Details |

|---|---|

| Established | 1974 — by G10 central bank governors after Herstatt Bank collapse |

| Parent Institution | Bank for International Settlements (BIS), Basel, Switzerland |

| Headquarters of BIS | Basel, Switzerland |

| Current Membership | 45 institutions from 28 jurisdictions (as of 2025) |

| India's Representation | Reserve Bank of India is a member of BCBS |

| Authority | No formal supranational legal authority — standards are voluntary but widely adopted |

| Key Publications | Basel I (1988), Basel II (2004), Basel III (2010-2017), Basel III final rule (2023) |

Basel I (1988) — The First Capital Accord

Background

By the 1980s, international banks were growing rapidly and their capital levels were widely considered inadequate relative to their risk exposures. Different countries had different capital rules, creating an uneven competitive playing field and systemic risks. The 1988 Basel Capital Accord (Basel I) was the first attempt to establish minimum capital standards on a globally harmonized basis.

Key Features of Basel I

- Focus: Credit risk only — the risk that borrowers default on their loans

- Risk Weighting: Assets classified into four risk weight categories — 0% (government securities), 20% (inter-bank claims, OECD government agency claims), 50% (residential mortgages) and 100% (commercial loans, most other assets)

- Minimum CAR: Banks must hold capital equal to at least 8% of total Risk-Weighted Assets (RWA)

- Capital Definition: Two tiers — Tier 1 (core capital: paid-up equity + disclosed reserves) and Tier 2 (supplementary capital: undisclosed reserves, revaluation reserves, general provisions, subordinated debt); Tier 2 cannot exceed Tier 1

- Implementation Timeline: Countries had until 1992 to fully implement; adopted by 100+ countries

Limitations of Basel I

- Covered only credit risk — ignored operational risk and market risk, which proved significant

- Same 100% risk weight for all corporate loans regardless of actual creditworthiness — a loan to a highly rated corporation treated the same as a loan to a highly speculative borrower

- Encouraged regulatory arbitrage — banks used securitization and off-balance-sheet structures to reduce their apparent RWA while maintaining the same actual risk

- No recognition of credit risk mitigation techniques like netting agreements and financial collateral

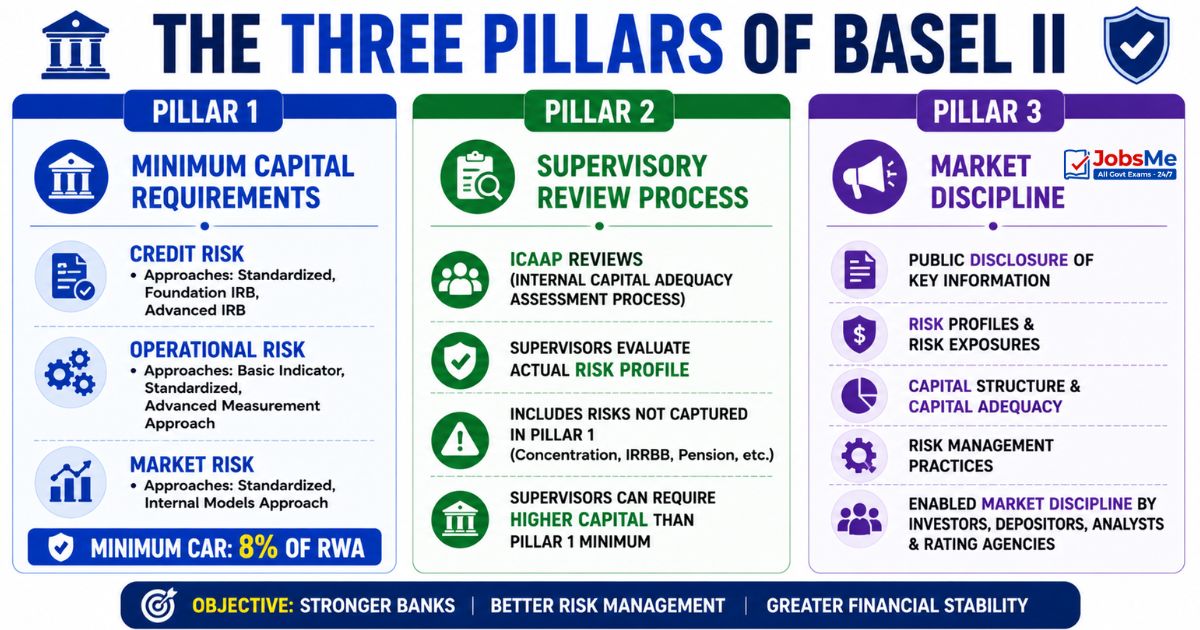

Basel II (2004) — Three Pillars Framework

Background

The limitations of Basel I became increasingly apparent through the 1990s. Rapid financial innovation, the growth of derivatives markets and the use of internal credit models by sophisticated banks made Basel I's crude risk weighting system inadequate. The LTCM (Long-Term Capital Management) hedge fund crisis in 1998 highlighted systemic risks. Basel II, finalized in June 2004, introduced a much more comprehensive and risk-sensitive framework.

The Three Pillars of Basel II

| Pillar | Name | Content and Purpose |

|---|---|---|

| Pillar 1 | Minimum Capital Requirements | Extends Basel I by requiring capital for three types of risk: Credit Risk (can use Standardized, Foundation IRB or Advanced IRB approach), Operational Risk (using Basic Indicator, Standardized or Advanced Measurement Approach) and Market Risk (Standardized or Internal Models approach). Minimum CAR remains 8% of RWA |

| Pillar 2 | Supervisory Review Process | Requires regulators (RBI in India) to conduct Internal Capital Adequacy Assessment Process (ICAAP) reviews — supervisors must actively evaluate whether each bank's capital is adequate for its actual risk profile including risks not captured in Pillar 1 (concentration risk, interest rate risk in banking book, pension risk, etc.). Supervisors can require banks to hold more capital than the Pillar 1 minimum |

| Pillar 3 | Market Discipline | Requires banks to publicly disclose comprehensive, standardized information about their risk profiles, capital structure, capital adequacy, risk exposures and risk management practices. Public disclosure enables investors, depositors, analysts and rating agencies to assess the bank's risk-taking and exercise market discipline — complementing supervisory oversight |

Basel II Approaches for Credit Risk Capital

| Approach | Description | Sophistication Level |

|---|---|---|

| Standardized Approach (SA) | Uses risk weights prescribed by the regulator; external credit ratings (from agencies like CRISIL, ICRA, CARE) used to differentiate risk weights for corporate exposures | Simpler; suitable for smaller banks |

| Foundation Internal Ratings-Based (F-IRB) | Banks use their own internal credit models to estimate Probability of Default (PD); regulatory estimates used for other parameters | Intermediate sophistication |

| Advanced Internal Ratings-Based (A-IRB) | Banks use own models for PD, Loss Given Default (LGD) and Exposure at Default (EAD); requires RBI approval and validation | Highest sophistication; only for large sophisticated banks |

Limitations of Basel II — Exposed by the 2008 Crisis

- Excessive reliance on banks' own internal risk models — banks had incentives to underestimate risk to reduce capital requirements

- Capital requirements were procyclical — fell during good times (when risk seemed low) and rose during bad times (when banks were least able to raise capital)

- Did not adequately address liquidity risk — banks were well-capitalized but became illiquid during the 2008 crisis

- Did not capture systemic risk adequately — focused on individual bank risk without considering interconnections

- Off-balance-sheet exposures (securitization structures like SIVs and CDOs) were under-capitalized

Basel III (2010-2017) — Post-Financial Crisis Comprehensive Reform

Background

The 2007-2009 global financial crisis was the most severe financial crisis since the Great Depression of the 1930s. Major banks like Lehman Brothers (USA) failed; Citigroup, Bank of America, UBS and many European banks required massive government bailouts. The crisis exposed deep weaknesses in the pre-crisis Basel II framework — inadequate capital quality, excessive leverage, insufficient liquidity buffers and failure to address systemic risk. The G20 leaders instructed the BCBS to design a stronger, more comprehensive framework. Basel III was announced in December 2010 and phased in through 2019 (with further refinements to 2023).

Basel III — Capital Requirements

| Capital Requirement | Global Minimum (Basel III) | India's Requirement |

|---|---|---|

| Common Equity Tier 1 (CET1) | 4.5% of RWA | 5.5% of RWA |

| Additional Tier 1 (AT1) | 1.5% of RWA (to bring Tier 1 to 6%) | 1.5% of RWA |

| Tier 1 Capital Ratio | 6.0% of RWA (CET1 + AT1) | 7.0% of RWA |

| Tier 2 Capital | 2.0% of RWA (to bring total to 8%) | 2.0% of RWA |

| Total Capital Adequacy Ratio (CAR) | 8.0% of RWA | 9.0% of RWA |

| Capital Conservation Buffer (CCB) | 2.5% of RWA (additional CET1) | 2.5% of RWA |

| Countercyclical Capital Buffer (CCyB) | 0% to 2.5% of RWA (set by national regulator) | 0% currently; can be raised by RBI |

| Effective Total Minimum (with CCB) | 10.5% of RWA (8% + 2.5%) | 11.5% of RWA (9% + 2.5%) |

Basel III — Capital Quality Tiers Explained

| Tier | Instruments | Key Characteristics |

|---|---|---|

| CET1 (Common Equity Tier 1) | Ordinary (common) shares + Retained earnings + Other comprehensive income | Highest quality; always available to absorb losses; no maturity; no fixed dividend obligation; forms core of bank's loss-absorbing capacity on going-concern basis |

| AT1 (Additional Tier 1) | Perpetual bonds with write-down or conversion to equity trigger at point of non-viability (PONV); also called Contingent Convertible bonds (CoCo bonds) or Basel III bonds | Absorbs losses when bank reaches point of non-viability trigger; write-down or conversion to equity triggered; no maturity date; distributions can be cancelled; subordinate to depositors and senior creditors |

| Tier 2 Capital | Subordinated debt with minimum 5-year original maturity; general provisions and loan loss reserves (within limits); revaluation reserves | Absorbs losses on gone-concern basis (during liquidation); lower quality than Tier 1; cannot be used to cover losses during ongoing operations; redeemable after 5 years |

Basel III — Capital Buffers

Capital Conservation Buffer (CCB)

- Additional CET1 of 2.5% of RWA to be maintained above the minimum capital requirements

- Purpose: to ensure banks accumulate capital in good times to be drawn down during economic downturns without breaching minimum regulatory capital

- If a bank's CET1 falls within the buffer zone (between minimum + 0% to minimum + 2.5%), automatic restrictions kick in on dividend payments, share buybacks and discretionary bonuses — creating strong incentives to maintain capital above the minimum at all times

- Fully implemented; cannot be waived

Countercyclical Capital Buffer (CCyB)

- Additional CET1 buffer of 0% to 2.5% of RWA, set by national regulators based on credit cycle conditions

- Purpose: build up capital buffers during periods of excessive credit growth (when systemic risk is building) and release them during economic downturns (to support continued lending)

- Each country's banking regulator sets the CCyB rate for their jurisdiction

- RBI currently maintains the CCyB at 0% for Indian banks — meaning it has not yet activated this buffer

Basel III — Leverage Ratio

The Leverage Ratio was introduced as a non-risk-based backstop to complement the risk-weighted capital ratios. It prevents banks from building up excessive leverage in their balance sheets by focusing purely on Tier 1 capital as a percentage of total exposure (not risk-weighted — all exposures counted at full face value without risk weighting).

- Global minimum: 3% of total exposure

- India's requirement: 4% for domestic banks; 3.5% for certain categories

- Simple to calculate and harder to game through risk model manipulation

- Serves as a check on banks that might have low risk-weighted ratios because of favorable internal risk models but very high actual balance sheet size

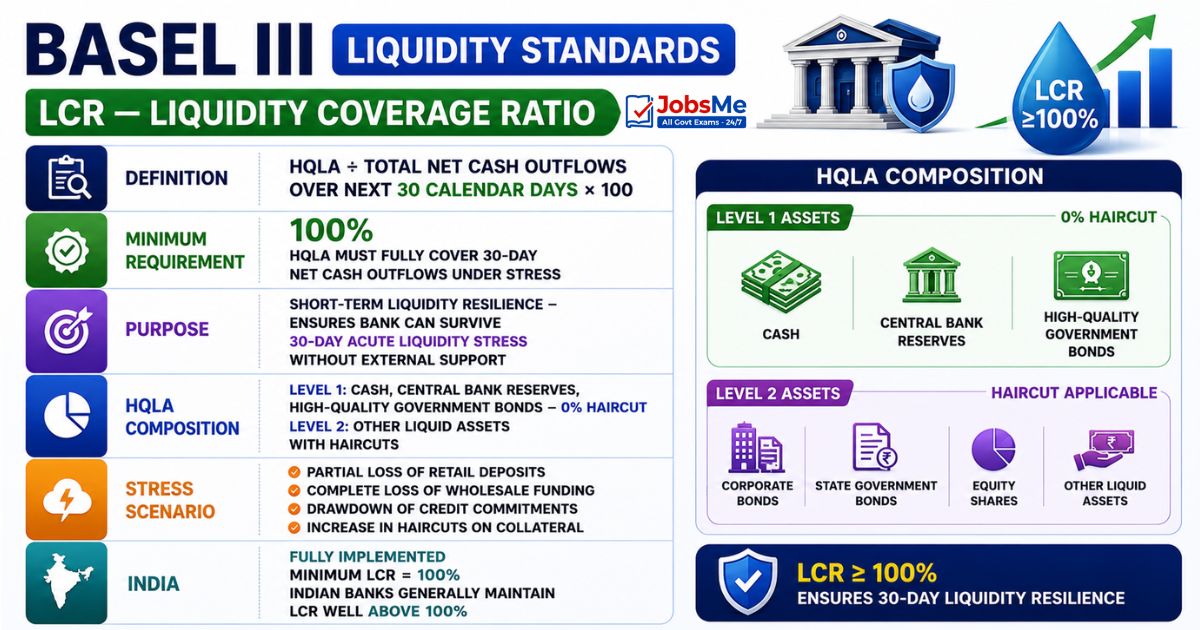

Basel III — Liquidity Standards

LCR — Liquidity Coverage Ratio

| Parameter | Details |

|---|---|

| Definition | High-Quality Liquid Assets (HQLA) ÷ Total Net Cash Outflows over next 30 calendar days × 100 |

| Minimum Requirement | 100% — HQLA must fully cover 30-day net cash outflows under a stress scenario |

| Purpose | Short-term liquidity resilience — ensures bank can survive a 30-day acute liquidity stress without external support |

| HQLA Composition | Level 1 (cash, central bank reserves, high-quality government bonds — 0% haircut) and Level 2 (other liquid assets with haircuts) |

| Stress Scenario | Includes partial loss of retail deposits, complete loss of wholesale funding, drawdown of credit commitments, increase in haircuts on collateral |

| India | Fully implemented; minimum LCR = 100%; Indian banks generally maintain LCR well above 100% |

NSFR — Net Stable Funding Ratio

| Parameter | Details |

|---|---|

| Definition | Available Stable Funding (ASF) ÷ Required Stable Funding (RSF) × 100 |

| Minimum Requirement | 100% — ASF must exceed RSF over a one-year horizon |

| Purpose | Structural long-term liquidity resilience — promotes stable funding profiles to reduce reliance on short-term wholesale funding |

| ASF Sources | Equity capital, preferred stock, long-term liabilities (maturity over 1 year), stable retail deposits and wholesale deposits with high retention probability |

| RSF Items | Long-term illiquid assets (loans, fixed assets), off-balance-sheet exposures, high-quality liquid assets are partially exempted |

| India | Implemented; minimum NSFR = 100% |

Comparison of Basel I, II and III

| Feature | Basel I (1988) | Basel II (2004) | Basel III (2010) |

|---|---|---|---|

| Trigger | Herstatt Bank crisis 1974; inadequate global bank capital | Complexity of modern banks; Basel I's crude risk weighting; LTCM crisis 1998 | Global Financial Crisis 2007-2009; Basel II's capital quality and liquidity failures |

| Risks Covered | Credit risk only | Credit risk + Market risk + Operational risk | Credit + Market + Operational + Liquidity risk + Systemic risk |

| Capital Quality | Tier 1 and Tier 2 (broadly defined) | Tier 1 and Tier 2 (broadly defined; similar to Basel I) | CET1, AT1, Tier 2 — much stricter definitions; higher CET1 requirement |

| Minimum CAR | 8% | 8% | 8% (global) + 2.5% CCB = 10.5% effective minimum |

| Pillars | 1 (capital requirement) | 3 (capital + supervisory review + market discipline) | Builds on 3 pillars; adds capital buffers, leverage ratio and liquidity standards |

| Leverage Ratio | Not included | Not included | Included — minimum 3% |

| Liquidity Standards | Not included | Not included | LCR (30-day stress) and NSFR (1-year stable funding) |

Memory Tricks — Basel Norms

Remember Basel Trigger Events

Trick: Basel I (1974-1988) → Herstatt Bank. Basel II (1998-2004) → LTCM Fund crisis. Basel III (2008-2010) → Global Financial Crisis (Lehman Brothers). Each Basel norm followed a crisis that exposed the previous framework's gaps.

Remember the Three Pillars

Trick: Pillar 1 = Minimum Money (capital for risks). Pillar 2 = Supervisor Scrutiny (regulatory review). Pillar 3 = Market Monitoring (public disclosure). MSD = Money, Supervision, Disclosure. Three pillars hold up the Basel II house.

Remember Capital Requirements

Trick: CET1 minimum = 4.5%. Add AT1 1.5% = Tier 1 total 6%. Add Tier 2 2% = Total CAR 8% (global). India adds 1% = 9%. Then add CCB 2.5% = effective minimum 10.5% (global) or 11.5% (India).

Remember LCR vs NSFR

Trick: LCR = Liquid assets for 30 DAYS (short-term emergency cash). NSFR = Stable funding for 1 YEAR (long-term structural balance). L = Liquid (short). N = Not short (long). Both must be at least 100%.

Remember India's Higher CAR

Trick: India = 9% CAR. Global = 8% CAR. India adds 1% extra safety buffer — RBI is more conservative than the global standard because Indian banks operate in a riskier developing economy environment.

One-Liners for Quick Revision — Basel Norms

- BCBS established: 1974; after Herstatt Bank collapse; under BIS, Basel, Switzerland.

- BIS headquarters: Basel, Switzerland; often called the "bank for central banks."

- Basel I (1988): credit risk only; minimum CAR 8% of RWA.

- Basel II (2004): three pillars; added operational risk and market risk to capital requirements.

- Three Pillars of Basel II: Minimum Capital, Supervisory Review, Market Discipline.

- Basel II approaches for credit risk: Standardized, Foundation IRB, Advanced IRB.

- Basel III (2010): post-GFC reform; added LCR, NSFR, Leverage Ratio, CCB, CCyB.

- Global minimum CAR: 8%; India's minimum: 9%.

- Global CET1 minimum: 4.5%; India's CET1 minimum: 5.5%.

- Global Tier 1 capital minimum: 6%; India: 7%.

- Capital Conservation Buffer (CCB): 2.5% of RWA; mandatory CET1.

- Countercyclical Capital Buffer (CCyB): 0-2.5% of RWA; India's CCyB = 0% currently.

- Leverage Ratio minimum: 3% globally; 4% in India.

- LCR: HQLA for 30-day stress; minimum 100%.

- NSFR: stable funding for 1 year; minimum 100%.

- AT1 bonds also called CoCo bonds (Contingent Convertible bonds).

- D-SIBs in India: SBI, HDFC Bank, ICICI Bank; face additional CET1 surcharge.

- RBI implements Basel III for all scheduled commercial banks in India.

Preparing for competitive exams requires consistent revision. Platforms like JobsMe simplify preparation through:

- Daily Current Affairs

- Weekly Current Affairs

- Monthly Current Affairs

- Static GK for Competitive Exams

- Latest Government Jobs Notifications

- Computer Awareness

Stay updated, revise regularly, and attempt quizzes for better accuracy in UPSC, SSC CGL, IBPS PO/Clerk, SBI, RBI Grade B, RRB NTPC, Defence, and State PSC exams.

Free quiz • No signup required

Put this topic into practice with Current Affairs Quiz 20 June 2026 | UPSC, SSC, Banking, Railways & State PSC MCQs with Answers. It is the quickest way to reinforce what you just learned.

Frequently Asked Questions

What is the BCBS and how is it related to BIS?

What are the three pillars of Basel II?

What is the Capital Adequacy Ratio (CAR) and why is India's minimum higher than the global minimum?

What are LCR and NSFR under Basel III?

What is the Capital Conservation Buffer (CCB)?

What is the difference between CET1, Additional Tier 1 and Tier 2 capital?

About the author