Priority Sector Lending (PSL) – Complete Banking Awareness Notes 2026 for IBPS and SBI

Priority Sector Lending (PSL) is a high-frequency topic in all banking awareness examinations. This chapter covers the complete PSL framework — the policy rationale, all PSL categories and sub-targets for domestic banks (agriculture 18%, MSME 7.5%, weaker sections 12%, total 40% of ANBC), PSL targets for foreign banks, the RIDF penalty mechanism, Priority Sector Lending Certificates (PLSCs), the Kisan Credit Card scheme in full detail (eligibility, issuing banks, credit limit structure, interest subvention), Self-Help Groups (SHG) and Joint Liability Groups (JLG), microfinance regulations, MUDRA loans and their relationship to PSL, and all related PSL concepts tested in IBPS PO, SBI PO, RBI Grade B and NABARD examinations.

Jump to section

- Priority Sector Lending — Introduction and Policy Rationale

- PSL Targets for Domestic Scheduled Commercial Banks

- PSL Sub-Categories — Detailed Definitions

- Penalty for PSL Shortfall — RIDF and Other Funds

- Priority Sector Lending Certificates (PLSCs)

- Kisan Credit Card (KCC) Scheme — Complete Coverage

- Self-Help Groups (SHGs) and Joint Liability Groups (JLGs)

- Microfinance — NBFC-MFI Framework

- MUDRA Loans and PSL

- Farmer Producer Organizations (FPOs) and PSL

- Memory Tricks — Priority Sector Lending

- One-Liners for Quick Revision

Priority Sector Lending — Introduction and Policy Rationale

India's commercial banking system, if left purely to profit-maximising behaviour, would naturally concentrate its lending in low-risk, high-return urban corporate and consumer segments. Agriculture — which employs over 40% of India's workforce — would receive inadequate credit because agricultural loans are often small-ticket, high-risk (dependent on rainfall and crop prices) and lack strong collateral. Micro and small enterprises would struggle to compete with large corporations for bank attention. The rural poor would remain excluded from formal finance.

To correct this market failure and direct credit to sectors essential for India's inclusive development, the Reserve Bank of India mandates that all scheduled commercial banks maintain Priority Sector Lending (PSL) — a minimum percentage of their loan books must go to specified priority sectors. This is not a subsidy — banks earn market-appropriate interest on PSL loans — but it is a directed credit requirement that ensures credit reaches underserved areas of the economy.

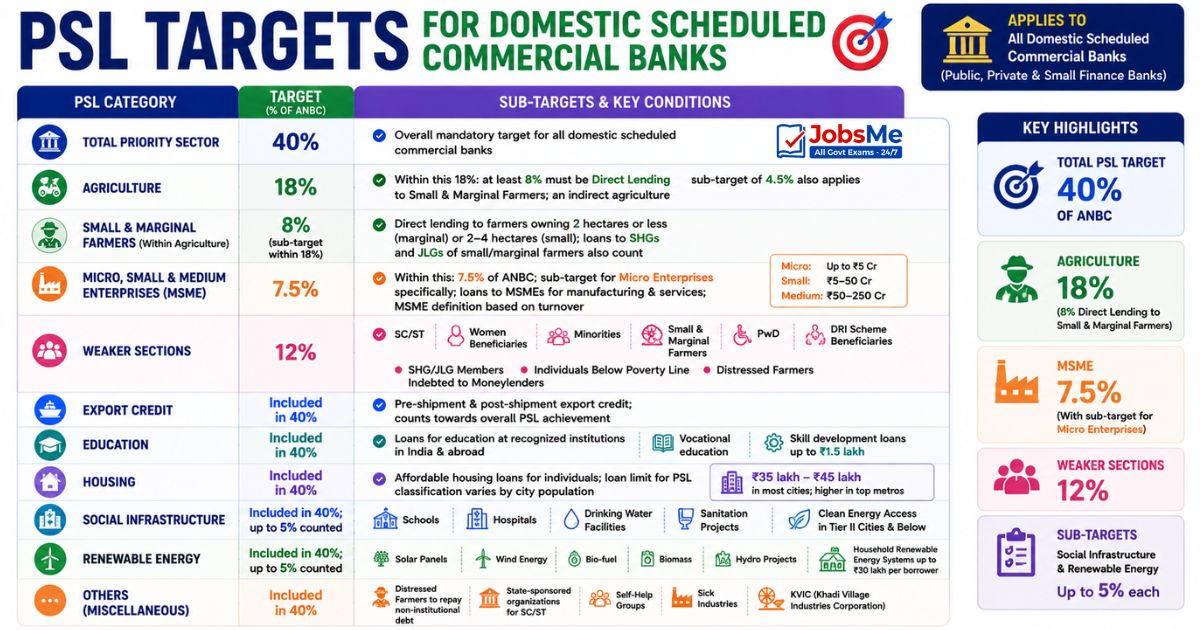

PSL Targets for Domestic Scheduled Commercial Banks

| PSL Category | Target (% of ANBC) | Sub-Targets and Key Conditions |

|---|---|---|

| Total Priority Sector | 40% | Overall mandatory target for all domestic scheduled commercial banks — public sector, private sector and small finance banks |

| Agriculture | 18% | Within this 18%: at least 8% must be Direct Lending to Small and Marginal Farmers; an indirect agriculture sub-target of 4.5% also applies |

| Small and Marginal Farmers (within Agriculture) | 8% (sub-target within 18%) | Direct lending to farmers owning 2 hectares or less (marginal) or 2-4 hectares (small); loans to SHGs and JLGs of small/marginal farmers also count |

| Micro, Small and Medium Enterprises (MSME) | 7.5% | Within this: 7.5% of ANBC; sub-target for Micro Enterprises specifically; loans to MSMEs for manufacturing and service activities; MSME definition based on turnover (micro: up to Rs. 5 crore, small: Rs. 5-50 crore, medium: Rs. 50-250 crore) |

| Weaker Sections | 12% | Includes: SC/ST, women beneficiaries, minorities, small and marginal farmers, Persons with Disabilities (PwD), DRI scheme beneficiaries, SHG/JLG members, individuals below poverty line, distressed farmers indebted to moneylenders |

| Export Credit | Included in 40%; no specific sub-target | Pre-shipment and post-shipment export credit; counts towards overall PSL achievement |

| Education | Included in 40%; no specific sub-target | Loans for education at recognized institutions in India and abroad; vocational education; skill development loans up to Rs. 1.5 lakh |

| Housing | Included in 40%; no specific sub-target | Affordable housing loans for individuals; loan limit for PSL classification varies by city population (Rs. 35 lakh to Rs. 45 lakh in most cities; higher in top metros) |

| Social Infrastructure | Included in 40%; up to 5% counted | Loans for construction of schools, hospitals, drinking water facilities, sanitation projects, clean energy access in Tier II cities and below |

| Renewable Energy | Included in 40%; up to 5% counted | Loans for solar panels, wind energy, bio-fuel, biomass, hydro projects; household renewable energy systems up to Rs. 30 lakh per borrower |

| Others (miscellaneous) | Included in 40% | Loans to distressed farmers to repay non-institutional debt; loans to state-sponsored organizations for SC/ST; loans to self-help groups; loans to sick industries; loans to KVIC (Khadi Village Industries Corporation) |

PSL Targets for Foreign Banks in India

| Foreign Bank Category | Total PSL Target | Sub-Targets |

|---|---|---|

| Foreign Banks with 20 or more branches in India | 40% of ANBC | Same sub-targets as domestic banks — agriculture 18%, small and marginal farmers 8%, MSME 7.5%, weaker sections 12% |

| Foreign Banks with fewer than 20 branches | 40% of ANBC | Relaxed sub-target composition; higher export credit weight; phased achievement of agriculture and weaker section sub-targets by 2025 |

Note: Regional Rural Banks (RRBs) have separate, higher PSL targets — 75% of ANBC, with specific sub-targets appropriate to their rural mandate. Small Finance Banks (SFBs) must maintain 75% PSL, with sub-targets including 40% to micro enterprises.

PSL Sub-Categories — Detailed Definitions

Agriculture — Direct vs Indirect Lending

| Type | What Counts | PSL Sub-target |

|---|---|---|

| Direct Agriculture Lending | Loans directly to farmers for crop production (KCC, crop loans), purchase of farm inputs, allied activities (animal husbandry, fisheries, sericulture), purchase of land development machinery, irrigation infrastructure; loans to SHGs and JLGs of farmers; FPO (Farmer Producer Organization) loans | 8% for small and marginal farmers within overall 18% |

| Indirect Agriculture Lending | Loans to agri-processing industries, agri-input dealers, agri-infrastructure (warehouses, cold storage, market yards), micro-irrigation, MFIs lending to agriculture, and agri-export companies | Counts towards overall 18% agriculture target; sub-target of 4.5% for indirect agriculture |

MSME — Definition Update (2020)

The MSME definition was revised by the Government of India in May 2020 to expand the scope of MSME classification:

| Category | Investment in Plant and Machinery (Manufacturing / Services) | Annual Turnover |

|---|---|---|

| Micro Enterprise | Up to Rs. 1 crore (manufacturing and services — unified) | Up to Rs. 5 crore |

| Small Enterprise | Up to Rs. 10 crore | Up to Rs. 50 crore |

| Medium Enterprise | Up to Rs. 50 crore | Up to Rs. 250 crore |

Penalty for PSL Shortfall — RIDF and Other Funds

Banks that fail to achieve their PSL targets or sub-targets at the end of a financial year are required to contribute the shortfall amount to specified funds. These contributions earn a return lower than direct PSL lending — acting as an effective financial penalty:

| PSL Shortfall Category | Fund to Contribute To | Maintained by |

|---|---|---|

| Agriculture (including small and marginal farmers sub-target) | RIDF (Rural Infrastructure Development Fund) | NABARD |

| Micro enterprises and MSME shortfall | MUDRA Fund | MUDRA (Micro Units Development and Refinance Agency) |

| Housing shortfall | National Housing Bank (NHB) Fund | National Housing Bank |

| Overall shortfall (not covered above) | SIDBI Fund | Small Industries Development Bank of India (SIDBI) |

The RIDF (Rural Infrastructure Development Fund) was established in FY1995-96 with NABARD as the implementing agency. Banks contribute to RIDF at interest rates below what they would earn from direct PSL loans — typically the bank rate minus a specified spread. NABARD uses RIDF funds to extend loans to State Governments and State-owned corporations for rural infrastructure projects (roads, bridges, rural electrification, watershed development, irrigation) in amounts up to their PSL shortfalls.

Priority Sector Lending Certificates (PLSCs)

PLSCs are tradeable instruments that create a market-based mechanism for efficient PSL compliance. Introduced by RBI in 2016, PLSCs allow banks to buy and sell PSL achievement across sub-categories.

How PLSC Trading Works

- Bank A exceeds its small and marginal farmer sub-target — it has achieved 10% of ANBC against a mandatory 8% target; it has a 2% surplus

- Bank B has achieved only 6% of ANBC in the small and marginal farmer category — it has a 2% shortfall

- Bank A can issue PLSCs for its 2% surplus and sell them to Bank B on the PLSC trading platform

- Bank B counts the purchased PLSCs as part of its small and marginal farmer achievement — meeting its 8% target

- Bank A receives the market price for the PLSCs; Bank B avoids RIDF contribution for the sub-target shortfall

PLSC Categories

PLSCs are available for the following sub-categories:

- Agriculture (direct)

- Small and Marginal Farmers

- Micro Enterprises

- Weaker Sections

PLSCs have a validity of one financial year — they are issued and must be traded within the same financial year for which the PSL targets are being computed.

Kisan Credit Card (KCC) Scheme — Complete Coverage

| Parameter | Details |

|---|---|

| Launched | 1998 |

| Recommended by | R.V. Gupta Working Group (set up by RBI and NABARD) |

| Objective | Provide farmers with a flexible, revolving credit card-based facility to meet their entire crop production credit needs — including short-term and consumption needs — eliminating their dependence on informal moneylenders |

| Eligible Borrowers | Individual farmers (owner cultivators); joint borrower farmers; tenant farmers; oral lessees; share croppers; SHGs and JLGs of farmers; allied activity participants (horticulture, sericulture, animal husbandry, fisheries) |

| Issuing Institutions | Scheduled Commercial Banks (SCBs); Regional Rural Banks (RRBs); Small Finance Banks (SFBs); Cooperative Banks; Primary Agricultural Credit Societies (PACS) |

| Credit Limit — Year 1 | Scale of Finance (SF) for crop × Acreage + 10% of SF for post-harvest expenses + 20% of SF for maintenance and repair of farm assets + consumption needs (subject to bank policy) + short-term credit for allied activities |

| Annual Limit Increase | The credit limit increases by 10% per year for the first five years to account for increased scale of finance, input cost escalation and enhanced operations |

| Term Credit Component | For allied activities and non-farm activities, a term credit component is added for asset acquisition (purchase of equipment, machinery, cattle) — repaid through crop sale proceeds over a defined schedule |

| Validity | 5 years (subject to annual review and enhancement based on performance) |

| Nature of Credit | Revolving — farmers can draw, repay after harvest and redraw before the next season, multiple times within the sanctioned limit; works exactly like a revolving credit card for farmers |

| Interest Rate | Applicable bank lending rate; Government of India provides interest subvention (2% p.a. plus additional 3% for prompt repayment = effective rate as low as 4% for prompt repayers) on KCC loans up to Rs. 3 lakh under Kisan Loan Interest Subvention Scheme |

| Personal Accident Insurance | KCC borrowers are covered under Personal Accident Insurance Scheme for death/disability: Rs. 50,000 for death/permanent disability and Rs. 25,000 for partial disability; premium paid by bank |

| Crop Insurance | KCC holders are eligible for crop insurance under Pradhan Mantri Fasal Bima Yojana (PMFBY) — premium is partly subsidized by government |

| PSL Classification | KCC loans qualify as Direct Agriculture lending under PSL; loans to small and marginal farmers under KCC count towards the 8% small and marginal farmer sub-target |

KCC for Allied Activities and Non-Farm Activities

The KCC scheme was extended beyond crop production to cover:

- Animal Husbandry: Dairy farmers, poultry farmers, sheep and goat rearers — short-term credit for purchase of feed, medicines and other operational inputs

- Fisheries: Inland fishers, marine fishers, fish farmers — credit for purchase of nets, fuel, bait and maintenance of boats

- Self Help Groups (SHGs) and Joint Liability Groups (JLGs): SHG/JLG members engaged in agriculture and allied activities can collectively access KCC

Self-Help Groups (SHGs) and Joint Liability Groups (JLGs)

Self-Help Group (SHG) — Complete Framework

| Parameter | Details |

|---|---|

| Group Size | 10 to 20 members; RBI allows groups of 5-20 for special categories |

| Composition | Predominantly women; from similar socio-economic backgrounds (below poverty line or low-income households); from the same village or neighborhood |

| Formation | Self-formed by members; often facilitated by NGOs, government departments or bank staff; registered informally |

| Savings | Members save a fixed amount regularly (weekly, fortnightly or monthly) into a common SHG fund — typically Rs. 50 to Rs. 500 per period |

| Internal Lending | The pooled savings are lent to members for productive and consumption needs at rates decided by the group; this internal lending track record establishes the group's creditworthiness |

| Bank Linkage | After operating for 6+ months with good internal repayment records, the SHG is eligible for bank credit under the SHG-Bank Linkage Programme (SBLP); the bank extends credit to the SHG as a unit (not to individual members) |

| SHG-Bank Linkage Programme (SBLP) | Pioneered by NABARD in 1992; became the world's largest microfinance programme; over 130 lakh SHGs credit-linked with banks across India by 2024 |

| Credit-to-Savings Ratio | Banks typically lend 4 to 10 times the SHG's total savings balance; higher for well-performing groups with longer track records |

| PSL Classification | Bank loans to SHGs count as PSL under weaker sections and agriculture (if used for farm activities); also count towards the priority sector target for the bank |

| DAY-NRLM | Deendayal Antyodaya Yojana — National Rural Livelihoods Mission; government scheme that promotes SHG formation and bank linkage; facilitates credit linkage of SHGs through State Rural Livelihoods Missions (SRLMs) |

Joint Liability Group (JLG) — Key Facts

| Parameter | Details |

|---|---|

| Group Size | 4 to 10 members |

| Composition | Farmers, agricultural labourers, rural artisans, small traders; no savings requirement unlike SHGs |

| Mechanism | Members collectively borrow from a bank; each member is jointly and severally liable for repayment of all members' loans; peer pressure and social solidarity serve as collateral substitutes |

| Loan Size | Typically Rs. 50,000 to Rs. 5 lakh per member depending on the bank and purpose |

| Security | No physical collateral required; the joint liability of all members is the security; sometimes supported by group savings deposited with the bank |

| NABARD Promotion | NABARD actively promotes JLG formation, especially for tenant farmers and oral lessees who cannot prove land ownership and hence cannot access individual KCC limits |

Microfinance — NBFC-MFI Framework

Microfinance institutions (MFIs) provide small loans to low-income borrowers — primarily women in rural and semi-urban areas. In India, MFIs operating as NBFCs are classified as NBFC-MFIs and regulated by the RBI under the NBFC-MFI Master Directions.

Key NBFC-MFI Regulations

- At least 85% of net assets must be in qualifying microfinance assets

- Qualifying loan criteria: Borrower annual household income ≤ Rs. 3 lakh (rural and urban); loan amount ≤ Rs. 3 lakh; loan without collateral

- Maximum outstanding from all MFI sources for a single borrower: Rs. 3 lakh

- Loan repayment on weekly/fortnightly/monthly basis; borrower's choice of repayment frequency

- Pricing transparency: NBFC-MFIs must display effective interest rate, processing fees and total cost of credit

- Loans to NBFC-MFIs by banks count as PSL — classified under weaker sections and agriculture depending on end use

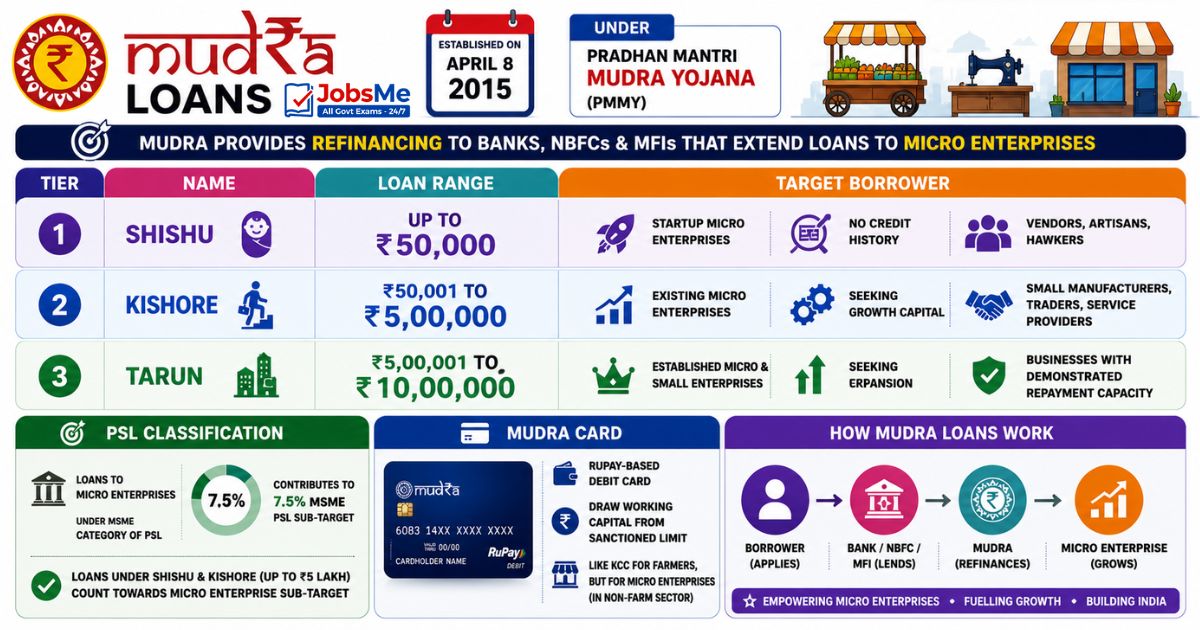

MUDRA Loans and PSL

MUDRA (Micro Units Development and Refinance Agency) was established on April 8, 2015 under the Pradhan Mantri MUDRA Yojana (PMMY). MUDRA provides refinancing to banks, NBFCs and MFIs that extend loans to micro enterprises. MUDRA loans are classified in three tiers:

| Tier | Name | Loan Range | Target Borrower |

|---|---|---|---|

| Tier 1 | Shishu | Up to Rs. 50,000 | Startup micro enterprises with no credit history; smallest and most nascent businesses; vendors, artisans, hawkers |

| Tier 2 | Kishore | Rs. 50,001 to Rs. 5,00,000 | Existing micro enterprises seeking growth capital; small manufacturers, traders, service providers with some business history |

| Tier 3 | Tarun | Rs. 5,00,001 to Rs. 10,00,000 | Established micro and small enterprises seeking expansion; businesses with demonstrated repayment capacity |

PSL Classification: MUDRA loans are classified as loans to Micro Enterprises under the MSME category of PSL — they contribute to the 7.5% MSME PSL sub-target. Loans under Shishu and Kishore categories (up to Rs. 5 lakh) specifically count towards the micro enterprise sub-target within MSME.

MUDRA Card: MUDRA provides a RuPay-based debit card (MUDRA Card) to eligible MUDRA borrowers to draw working capital from the sanctioned limit — similar to how a KCC works for farmers but for micro enterprises in the non-farm sector.

Farmer Producer Organizations (FPOs) and PSL

Farmer Producer Organizations (FPOs) are collective entities (usually registered as companies or cooperatives) formed by farmers to pool their produce, access better input pricing, improve market linkages and collectively bargain with buyers. Loans extended by banks directly to FPOs for agricultural activities are classified as Direct Agriculture under PSL. The government has a scheme to promote 10,000 FPOs across India, supported by NABARD, SFAC (Small Farmers Agribusiness Consortium) and state governments.

Memory Tricks — Priority Sector Lending

Remember Core PSL Numbers

Trick: "40-18-7.5-12." Total = 40%. Agriculture = 18%. MSME = 7.5%. Weaker Sections = 12%. Say these four numbers like a mantra: FORTY → EIGHTEEN → SEVEN-POINT-FIVE → TWELVE. Within agriculture, remember the 8% (small and marginal farmers) separately.

Remember KCC

Trick: KCC = 1998 + R.V. Gupta + Revolving Credit for Kisan. Three R's: 1998, R.V. Gupta, Revolving. The card revolves like the crop seasons — farmers draw for sowing and repay after harvest repeatedly.

Remember SHG vs JLG

Trick: SHG = Savings-first, 10-20 members, mostly women, saves then borrows. JLG = Joint Liability, 4-10 members, borrows directly, no savings requirement. SHG is bigger (10-20) and saves first; JLG is smaller (4-10) and borrows directly.

Remember RIDF

Trick: RIDF = Rural Infrastructure Development Fund = penalty parking for PSL shortfall. Banks that miss targets must park money in RIDF with NABARD at low interest — it's like a penalty box. RIDF money builds rural roads and bridges while the bank earns below-market returns.

Remember MUDRA Tiers

Trick: SKT = Shishu (Smallest — up to Rs. 50K), Kishore (Kid growing up — Rs. 50K to 5L), Tarun (Teenager expanding — Rs. 5L to 10L). Life stages of a micro enterprise: infant, adolescent, young adult.

One-Liners for Quick Revision

- Total PSL target: 40% of ANBC for all domestic scheduled commercial banks.

- Agriculture PSL: 18% of ANBC; sub-target of 8% directly to small and marginal farmers.

- MSME PSL: 7.5% of ANBC.

- Weaker Sections PSL: 12% of ANBC.

- Foreign banks with 20+ branches: same PSL targets as domestic banks — 40%.

- RRBs PSL target: 75% of ANBC; Small Finance Banks: 75%.

- PSL shortfall → contribute to RIDF (NABARD), MUDRA, NHB or SIDBI funds.

- RIDF: established FY1995-96; maintained by NABARD; funds rural infrastructure.

- PLSCs: tradeable PSL compliance certificates; category-specific; introduced 2016.

- KCC launched: 1998; R.V. Gupta Working Group.

- KCC credit: revolving; limit increases 10% per year for first 5 years.

- KCC validity: 5 years; interest subvention up to Rs. 3 lakh loans.

- KCC insurance: personal accident Rs. 50,000 death/permanent disability.

- KCC issuing institutions: SCBs, RRBs, SFBs, Cooperative Banks, PACS.

- SHG: 10-20 members; mostly women; saves first, then borrows.

- SBLP: SHG-Bank Linkage Programme pioneered by NABARD in 1992.

- JLG: 4-10 members; borrows directly; joint and several liability.

- NBFC-MFI qualifying loan: borrower income ≤ Rs. 3 lakh; loan ≤ Rs. 3 lakh; no collateral.

- MUDRA established: April 8, 2015 under PMMY.

- MUDRA Shishu: up to Rs. 50,000; Kishore: Rs. 50,001-Rs. 5 lakh; Tarun: Rs. 5 lakh-Rs. 10 lakh.

- Micro Enterprise MSME definition: investment ≤ Rs. 1 crore; turnover ≤ Rs. 5 crore.

Preparing for competitive exams requires consistent revision. Platforms like JobsMe simplify preparation through:

- Daily Current Affairs

- Weekly Current Affairs

- Monthly Current Affairs

- Static GK for Competitive Exams

- Latest Government Jobs Notifications

- Computer Awareness

Stay updated, revise regularly, and attempt quizzes for better accuracy in UPSC, SSC CGL, IBPS PO/Clerk, SBI, RBI Grade B, RRB NTPC, Defence, and State PSC exams.

Free quiz • No signup required

Put this topic into practice with Current Affairs Quiz 17 June 2026 MCQs for UPSC, SSC, Banking, Railways, Defence & State PSC Exams. It is the quickest way to reinforce what you just learned.

Frequently Asked Questions

What is Priority Sector Lending and why is it required?

What is ANBC and how is it calculated?

What is the consequence of not meeting PSL targets?

What are Priority Sector Lending Certificates (PLSCs)?

What is the Kisan Credit Card scheme?

What are SHGs and JLGs in the context of bank credit?

About the author