Non-Performing Assets (NPA) and Resolution – Complete Banking Awareness Notes 2026 for IBPS and SBI

Non-Performing Assets (NPA) and Resolution is a critical chapter in banking awareness for all competitive banking examinations. This chapter covers the complete definition of NPA and the 90-day rule, the three-stage asset classification (sub-standard, doubtful and loss assets), provisioning norms for each category, the causes of rising NPAs in India, all NPA resolution mechanisms including IBC 2016, SARFAESI Act, DRT, CDR, SDR, S4A and Asset Reconstruction Companies, the CAMELS rating framework used by RBI to assess bank health, and the GNPA and NNPA ratios that measure overall asset quality of the banking system.

Jump to section

- Non-Performing Assets (NPA) - Introduction

- Definition of NPA - The 90-Day Rule

- Classification of NPAs into Three Categories

- Standard Asset Provisioning

- Causes of Rising NPAs in India

- NPA Resolution Mechanisms - Complete Coverage

- GNPA and NNPA Ratios - Measuring Asset Quality

- CAMELS Rating System - Supervisory Assessment

- Prompt Corrective Action (PCA) Framework

- Special Mention Accounts (SMA)

- Memory Tricks - NPA and Resolution

- One-Liners for Quick Revision - NPA and Resolution

Non-Performing Assets (NPA) - Introduction

Non-Performing Assets represent one of the most serious and recurring challenges facing the Indian banking system. When banks extend loans, they expect regular interest and principal repayments from borrowers. When a borrower stops making these payments, the loan stops performing — it no longer generates income for the bank. Such a loan is called a Non-Performing Asset (NPA). A high NPA ratio signals poor asset quality, reduces bank profitability, constrains the bank's ability to lend further and can threaten the stability of the entire banking system if it spreads.

For banking examinations — IBPS PO, SBI PO, SBI Clerk, RBI Grade B, NABARD Grade A — the NPA chapter is tested across multiple dimensions: NPA definition, classification, provisioning norms, causes of NPAs, resolution mechanisms and the CAMELS supervisory rating system. This chapter provides comprehensive coverage of all these aspects.

Definition of NPA - The 90-Day Rule

According to the Reserve Bank of India's prudential norms, a loan or advance is classified as a Non-Performing Asset when:

- Interest or principal installment remains overdue for more than 90 days in respect of a term loan

- The account remains out of order for more than 90 days in respect of an overdraft or cash credit account (out of order means the outstanding balance is continuously exceeding the sanctioned limit, or there are no credits in the account for 90 days, or the credits are insufficient to cover interest debited)

- A bill remains overdue for more than 90 days in case of bills purchased and discounted

- Interest or installment is overdue for two crop seasons for short-duration agricultural crops

- Interest or installment is overdue for one crop season for long-duration agricultural crops

Standard Asset: Any loan that is performing — interest and principal payments are being made regularly and there is no overdue for more than 90 days — is classified as a Standard Asset. Standard assets are healthy loans from the bank's perspective.

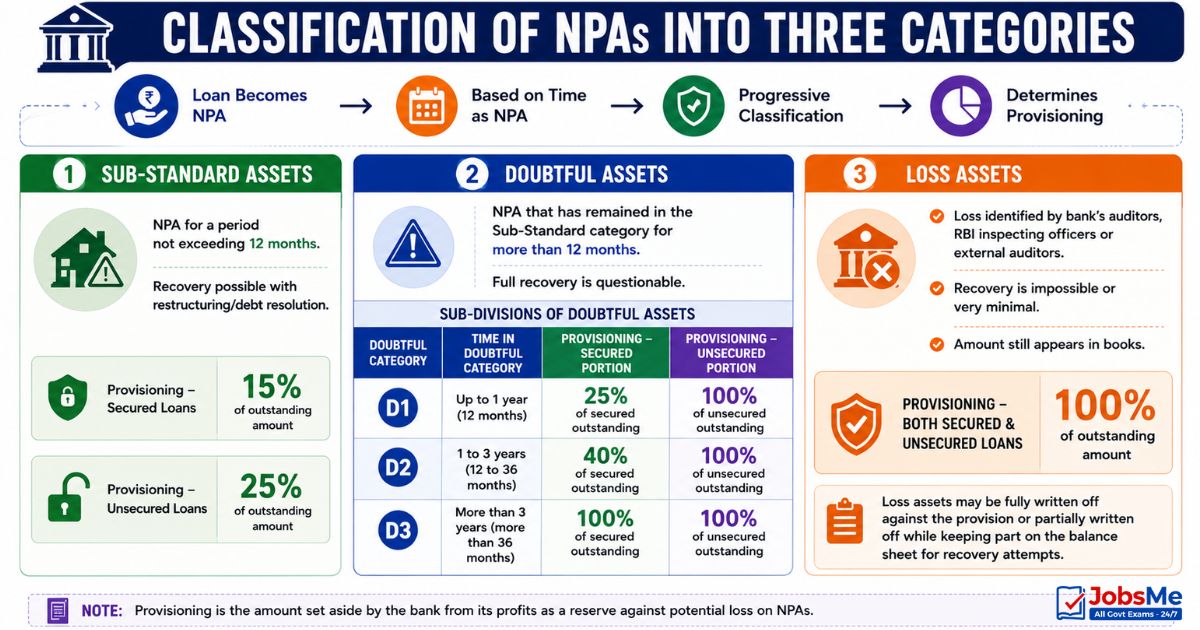

Classification of NPAs into Three Categories

Once a loan becomes an NPA, it is further classified based on how long it has been non-performing. This progressive classification determines the provisioning requirement — the amount of money the bank must set aside from its profits as a reserve against potential loss.

1. Sub-Standard Assets

A Sub-Standard Asset is an NPA for a period not exceeding 12 months. These are assets where the credit weakness that led to the default is clearly identifiable but the bank believes some recovery is possible with restructuring or debt resolution. The bank has not yet given up on recovering the full amount.

- Provisioning — Secured Loans: 15% of the outstanding amount

- Provisioning — Unsecured Loans: 25% of the outstanding amount

2. Doubtful Assets

A Doubtful Asset is an NPA that has remained in the Sub-Standard category for more than 12 months. The doubtful classification signals that full recovery is questionable — the bank has significant doubts about recovering the principal in full. Doubtful assets are further sub-divided into three categories:

| Doubtful Category | Time in Doubtful Category | Provisioning — Secured Portion | Provisioning — Unsecured Portion |

|---|---|---|---|

| Doubtful 1 (D1) | Up to 1 year (12 months) | 25% of secured outstanding | 100% of unsecured outstanding |

| Doubtful 2 (D2) | 1 to 3 years (12 to 36 months) | 40% of secured outstanding | 100% of unsecured outstanding |

| Doubtful 3 (D3) | More than 3 years (more than 36 months) | 100% of secured outstanding | 100% of unsecured outstanding |

3. Loss Assets

A Loss Asset is one where the loss has been identified by the bank's own auditors, the RBI's inspecting officers or by external auditors but the amount has not yet been written off completely from the bank's books. In practical terms, this is a loan where recovery is considered impossible or very minimal. Even though the amount still appears in the bank's books, 100% provisioning is required — meaning the bank must set aside an amount equal to the entire outstanding loan as a reserve for potential loss.

- Provisioning — Both Secured and Unsecured: 100% of the outstanding amount

- Loss assets may be fully written off against the provision or partially written off while keeping part on the balance sheet for recovery attempts

Standard Asset Provisioning

Even standard (performing) assets require a minimum amount of provisioning under RBI guidelines as a general precaution:

| Loan Category | Standard Asset Provisioning Rate |

|---|---|

| Direct advances to agriculture and SME sectors | 0.25% |

| Advances to CRE (Commercial Real Estate) sector | 1.00% |

| All other loans and advances | 0.40% |

| Restructured standard assets | 5.00% (initially; reduces over time if account performs) |

Causes of Rising NPAs in India

India's banking system, particularly public sector banks, witnessed a dramatic rise in NPAs between 2012 and 2018. Understanding the causes of NPA buildup is important for both examination questions and for understanding the broader banking landscape.

- Economic slowdowns: When the economy slows — as it did post the 2008 global financial crisis — businesses face revenue shortfalls and lose the ability to service debt. Power companies, steel manufacturers and infrastructure developers were particularly affected.

- Lax credit appraisal: During periods of high growth (2004-2008), banks extended large corporate loans with inadequate appraisal, insufficient due diligence and over-optimistic project assumptions, especially for infrastructure and mining projects.

- Wilful default: Several large promoters diverted loan funds to related parties, personal expenses or overseas accounts while refusing to inject equity to support their companies during stress.

- Regulatory and environmental hurdles: Many infrastructure projects — power plants, mines, highways — got stuck due to environmental clearance denials, land acquisition problems and policy changes (for example coal mine allocation cancellation by the Supreme Court in 2014), causing project failures and loan defaults.

- Promoter over-leverage: Many business groups borrowed excessively across multiple entities, creating a fragile debt structure that collapsed when cash flows were disrupted.

- Agricultural distress: Crop failures due to drought, floods or pest attacks prevent farmers from repaying agricultural loans.

- Political interference: Allegations of political pressure on public sector bank managements to extend loans to specific borrowers without adequate scrutiny.

- Evergreening: Some banks hid NPAs by extending fresh loans to enable borrowers to repay old ones — artificially keeping accounts "standard" while underlying stress mounted. RBI's Asset Quality Review (AQR) in 2015-16 forced banks to recognize and disclose these hidden NPAs, causing a sharp reported rise in GNPA ratios.

NPA Resolution Mechanisms - Complete Coverage

1. Insolvency and Bankruptcy Code (IBC) 2016

The IBC 2016 is the most powerful and comprehensive NPA resolution mechanism available to Indian banks. It provides a time-bound, market-driven process for resolving corporate insolvency at the National Company Law Tribunal (NCLT).

| Parameter | Details |

|---|---|

| Enacted | May 2016 |

| Administered by | Ministry of Corporate Affairs |

| Adjudicating Authority | NCLT (National Company Law Tribunal) for companies; DRT for individuals |

| Insolvency Regulator | IBBI (Insolvency and Bankruptcy Board of India) |

| Minimum Default Threshold | Rs. 1 crore (raised from Rs. 1 lakh in March 2020 to prevent misuse during COVID-19) |

| Resolution Timeline | 180 days from NCLT admission, extendable by another 90 days (total 270 days); Supreme Court later amended to maximum 330 days |

| CIRP | Corporate Insolvency Resolution Process — the main process for corporate debtors |

| Resolution Professional (IP) | Appointed by NCLT to manage operations and invite resolution plans from bidders |

| Committee of Creditors (CoC) | Financial creditors form the CoC; vote on resolution plans (75% vote required to approve) |

| If no resolution plan | Company goes into liquidation; assets distributed in prescribed waterfall order |

| Waterfall Order | CIRP costs → Secured creditors → Unsecured creditors → Government dues → Equity shareholders |

2. SARFAESI Act 2002

The SARFAESI Act (Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002) empowers banks to take possession of secured assets — property, machinery, vehicles — pledged as collateral and sell them to recover dues without requiring a court order. This dramatically speeds up the NPA recovery process for secured loans.

- Applicable for: NPAs of Rs. 1 lakh and above; secured loans

- Not applicable for: Unsecured loans, agricultural land, loans below Rs. 1 lakh

- Process: Bank issues a 60-day demand notice → if borrower does not repay or take corrective action → bank takes possession of secured assets → sells assets to recover dues

- Borrower's right: Can represent to the bank within 60 days; if rejected, can appeal to Debt Recovery Tribunal (DRT)

- Three roles of SARFAESI: Securitization (converting NPAs into tradeable securities), Asset Reconstruction (ARCs take over NPAs) and Enforcement (direct sale of collateral)

3. Debt Recovery Tribunal (DRT)

The Debt Recovery Tribunal (DRT) was established under the Recovery of Debts Due to Banks and Financial Institutions Act, 1993. DRTs are specialized fast-track quasi-judicial bodies designed to adjudicate bank loan recovery cases faster than regular civil courts.

- Applicable for bank dues of Rs. 20 lakh and above

- DRT passes a Recovery Certificate; the Recovery Officer can then attach and sell the debtor's properties

- Borrowers can appeal DRT orders to the Debt Recovery Appellate Tribunal (DRAT)

- India has 39 DRTs and 5 DRATs across the country

4. Corporate Debt Restructuring (CDR)

CDR is a voluntary, non-statutory mechanism where multiple lenders to a common borrower come together to restructure the outstanding debt — renegotiating repayment schedules, interest rates, loan tenures and sometimes converting part of the debt to equity — to give a viable but financially distressed company a chance to recover without going through insolvency. CDR was largely superseded by the IBC framework after 2016.

5. Strategic Debt Restructuring (SDR)

SDR is an RBI-introduced mechanism allowing a consortium of lenders to convert outstanding loan debt into equity shares of the distressed company, giving the lenders a majority equity stake and effective management control. Once in control, lenders can bring in a new management team or find a strategic buyer. SDR was introduced in 2015 and has been largely replaced by IBC proceedings.

6. Scheme for Sustainable Structuring of Stressed Assets (S4A)

S4A is an optional restructuring scheme for large stressed assets — projects with total loans of Rs. 500 crore and above — that are still viable as ongoing concerns but have unsustainable debt levels. Under S4A, the debt is divided into a sustainable portion (which continues as debt) and an unsustainable portion (which is converted into equity or quasi-equity instruments). This preserves the company as a going concern while reducing the debt burden to sustainable levels.

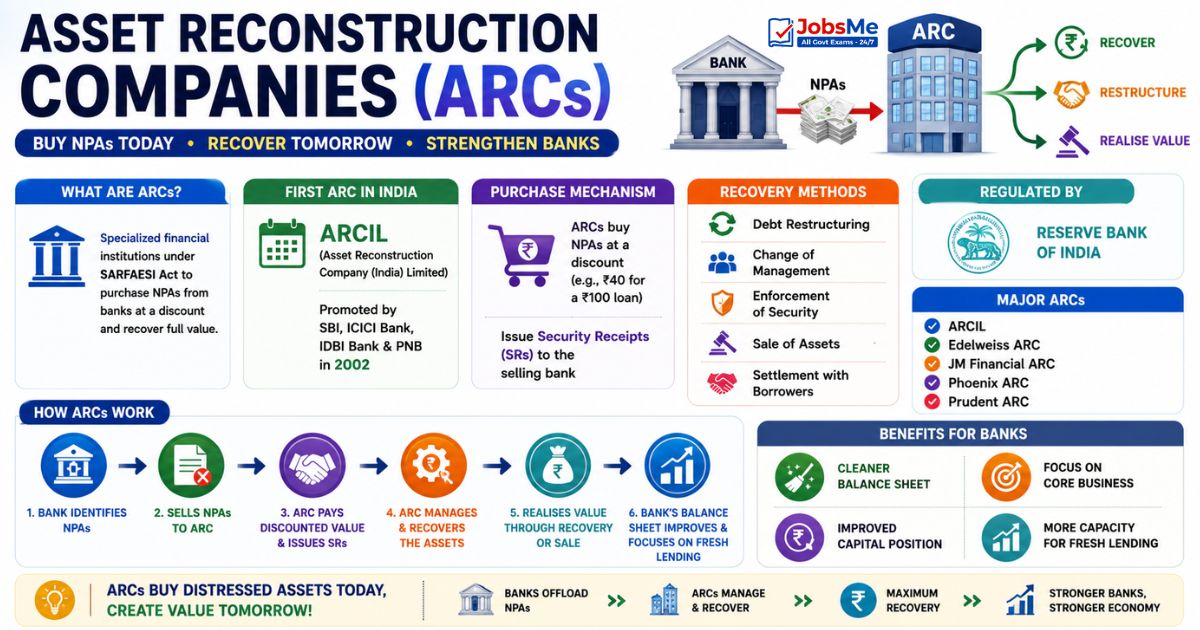

7. Asset Reconstruction Companies (ARCs)

Asset Reconstruction Companies are specialized financial institutions established under the SARFAESI Act to purchase NPAs from banks at a discount and attempt to recover the full value through debt restructuring, asset management or sale. By selling NPAs to ARCs, banks clean up their balance sheets and can focus on fresh lending.

| Parameter | Details |

|---|---|

| First ARC in India | ARCIL (Asset Reconstruction Company (India) Limited) — promoted by SBI, ICICI Bank, IDBI Bank and PNB in 2002 |

| Purchase mechanism | ARCs buy NPAs at a discount (for example, Rs. 40 for a Rs. 100 loan) and issue Security Receipts (SRs) to the selling bank |

| Recovery methods | Debt restructuring, change of management, enforcement of security, sale of assets, settlement with borrowers |

| Regulated by | Reserve Bank of India |

| Major ARCs | ARCIL, Edelweiss ARC, JM Financial ARC, Phoenix ARC, Prudent ARC |

GNPA and NNPA Ratios - Measuring Asset Quality

| Metric | Formula | What It Measures |

|---|---|---|

| GNPA Ratio | Gross NPA / Gross Advances × 100 | Total NPA exposure before provisions as a percentage of all loans — shows the scale of the NPA problem |

| NNPA Ratio | Net NPA / Net Advances × 100 | NPA exposure after deducting provisions — represents the bank's actual uncovered credit risk; more conservative and accurate measure |

| Provisioning Coverage Ratio (PCR) | Provisions / Gross NPA × 100 | Percentage of NPAs covered by provisions — higher PCR means the bank is better prepared for write-offs; RBI recommends PCR of at least 70% |

| Slippage Ratio | Fresh NPAs during the period / Standard Assets at beginning of period × 100 | Rate at which healthy loans are turning into NPAs — rising slippage ratio signals deteriorating credit quality |

India's NPA Journey: Indian banks' GNPA ratio peaked at approximately 11.5% in FY18 — driven by the RBI's Asset Quality Review (AQR) of 2015-16 which forced banks to recognize hidden NPAs. By FY25, the system-wide GNPA ratio had improved dramatically to approximately 2.7-3%, the lowest in many years, driven by IBC resolutions, write-offs, recoveries and improved credit quality of fresh disbursements.

CAMELS Rating System - Supervisory Assessment

The CAMELS rating system is a comprehensive supervisory framework used by the Reserve Bank of India to assess the overall financial health, risk profile and operational soundness of banks under its supervision. CAMELS ratings are assigned during RBI's Annual Financial Inspections (AFI) of banks.

| Letter | Component | What is Assessed | Key Ratios / Indicators |

|---|---|---|---|

| C | Capital Adequacy | Whether the bank has sufficient capital to absorb losses, support growth and meet regulatory requirements | CAR (Capital Adequacy Ratio), Tier 1 Ratio, CET1 Ratio, Leverage Ratio |

| A | Asset Quality | Quality of the bank's loan and investment portfolio — level of NPAs, concentrations, provisioning adequacy | GNPA Ratio, NNPA Ratio, Provisioning Coverage Ratio, Slippage Ratio |

| M | Management Quality | Effectiveness, integrity and competence of the bank's board and senior management in setting strategy and managing risk | Qualitative assessment by RBI inspectors — governance, compliance culture, risk management framework |

| E | Earnings | The bank's ability to generate sufficient earnings to fund operations, support capital growth and provide returns to shareholders | NIM (Net Interest Margin), ROA (Return on Assets), ROE (Return on Equity), Cost-to-Income Ratio |

| L | Liquidity | The bank's ability to meet its financial obligations as they fall due without incurring significant losses | LCR (Liquidity Coverage Ratio), NSFR (Net Stable Funding Ratio), CD Ratio (Credit-Deposit Ratio) |

| S | Sensitivity to Market Risk | The bank's vulnerability to adverse changes in market conditions — interest rates, foreign exchange rates, equity prices | Duration Gap, Value at Risk (VaR), Forex Open Position, Investment portfolio quality |

CAMELS Rating Scale

| Rating | Interpretation | RBI Response |

|---|---|---|

| 1 | Strong — sound performance on virtually every measure | Minimal regulatory attention; highest confidence |

| 2 | Satisfactory — fundamentally sound; minor weaknesses correctable | Normal supervisory attention |

| 3 | Fair — some degree of supervisory concern; weaknesses if not corrected could worsen | Enhanced monitoring and corrective action required |

| 4 | Marginal — significant financial problems; unsafe practices; high risk of failure if not corrected | Close supervision; restrictions may be imposed |

| 5 | Unsatisfactory — extremely high risk of failure; survival in doubt without immediate remedial action | Maximum regulatory intervention; possible moratorium or merger |

Prompt Corrective Action (PCA) Framework

The Prompt Corrective Action (PCA) Framework is a structured early warning and intervention system introduced by RBI to identify and correct financial weaknesses in banks before they become severe. Banks are placed under PCA when they breach certain trigger thresholds:

| Indicator | PCA Trigger Threshold |

|---|---|

| Capital Adequacy (CAR) | CAR falls below 10.25% (Minimum Regulatory Capital + CCB) |

| Net NPA Ratio | NNPA exceeds 6% of net advances |

| Return on Assets (RoA) | Negative RoA for two consecutive years |

| Tier 1 Leverage Ratio | Falls below prescribed minimum |

Restrictions Under PCA

- No dividend payments to shareholders

- No new branch expansion

- Restrictions on lending to high-risk borrowers and sectors

- Halt on recruitment and increase in staff expenses

- No new capital-consuming products or activities

- Management bonuses and discretionary expenses capped or stopped

- Possible reduction in the scope of operations

Banks are taken out of the PCA framework once they demonstrate sustained improvement across all trigger indicators over a minimum period and RBI is satisfied that the risk to the bank is contained.

Special Mention Accounts (SMA)

Even before a loan becomes an NPA (after 90 days), RBI requires banks to classify stressed accounts as Special Mention Accounts (SMAs) from the very first day of irregularity. This early warning system helps banks take proactive steps to prevent NPAs.

| SMA Category | Overdue Period | Action Required |

|---|---|---|

| SMA-0 | Principal or interest overdue for 1-30 days | Bank monitors closely; initiates contact with borrower |

| SMA-1 | Principal or interest overdue for 31-60 days | Enhanced monitoring; recovery steps initiated |

| SMA-2 | Principal or interest overdue for 61-90 days | Intensive follow-up; restructuring options explored |

| NPA | Overdue for more than 90 days | Account classified as Sub-Standard NPA; provisioning begins |

Memory Tricks - NPA and Resolution

Remember NPA Definition

Trick: NPA = 90-Day Rule. Think of 90 as three months (3 × 30 = 90). If a borrower misses three monthly payments, the loan becomes non-performing. Agricultural exception: two crop seasons (short-duration) or one crop season (long-duration).

Remember NPA Classification

Trick: SSD = Sub-Standard (under 12 months, 15% provision) → Doubtful (over 12 months, 25-100%) → Loss (identified as unrecoverable, 100%). Think of the progression as Bad → Worse → Written-Off.

Remember Provisioning Rates

Trick: Sub-Standard secured = 15%, unsecured = 25%. D1 secured = 25%. D2 secured = 40%. D3 secured = 100%. Unsecured is always 100% for all Doubtful categories. Only Sub-Standard unsecured is 25%, not 100%.

Remember CAMELS

Trick: CAMELS = A camel has six features that help it survive harsh desert conditions — Capital, Assets, Management, Earnings, Liquidity, Sensitivity. Like a well-rated bank, a camel is built for survival under stress.

Remember IBC Timeline

Trick: IBC 2016 = 180 days + up to 150 more = 330 days maximum. Think of it as 6 months (180) plus 5 months (150). After 330 days total, liquidation if no plan approved. Minimum default for IBC: Rs. 1 crore.

One-Liners for Quick Revision - NPA and Resolution

- NPA definition: loan overdue for more than 90 days.

- Agricultural NPA: overdue for two crop seasons (short-duration) or one crop season (long-duration).

- Sub-Standard Asset: NPA for not exceeding 12 months; provision 15% (secured), 25% (unsecured).

- Doubtful D1: 1-12 months in Doubtful; secured provision 25%.

- Doubtful D2: 1-3 years in Doubtful; secured provision 40%.

- Doubtful D3: more than 3 years in Doubtful; secured provision 100%.

- Loss Asset: 100% provisioning on both secured and unsecured portions.

- Provisioning Coverage Ratio (PCR): RBI recommends minimum 70%.

- India's GNPA ratio peaked at ~11.5% in FY18; improved to ~3% by FY25.

- IBC enacted: May 2016; minimum default: Rs. 1 crore.

- IBC resolution timeline: 180 days (extendable to maximum 330 days).

- IBBI: Insolvency and Bankruptcy Board of India — regulates IBC framework.

- SARFAESI: banks recover NPAs without court order; 60-day notice; minimum Rs. 1 lakh NPA.

- SARFAESI does NOT cover agricultural land and unsecured loans.

- DRT handles recovery of dues above Rs. 20 lakh; 39 DRTs across India.

- ARCIL: first ARC in India (2002); promoted by SBI, ICICI Bank, IDBI Bank, PNB.

- ARCs purchase NPAs at a discount and issue Security Receipts (SRs) to selling banks.

- CAMELS rating: 1 = Strong (best); 5 = Unsatisfactory (worst).

- PCA trigger: CAR below 10.25% OR NNPA above 6% OR negative RoA for two years.

- SMA-0: overdue 1-30 days; SMA-1: 31-60 days; SMA-2: 61-90 days.

- Wilful defaulter: has capacity to pay but deliberately refuses; faces severe credit and legal restrictions.

Preparing for competitive exams requires consistent revision. Platforms like JobsMe simplify preparation through:

- Daily Current Affairs

- Weekly Current Affairs

- Monthly Current Affairs

- Static GK for Competitive Exams

- Latest Government Jobs Notifications

- Computer Awareness

Stay updated, revise regularly, and attempt quizzes for better accuracy in UPSC, SSC CGL, IBPS PO/Clerk, SBI, RBI Grade B, RRB NTPC, Defence, and State PSC exams.

Free quiz • No signup required

Put this topic into practice with Current Affairs Quiz 20 June 2026 | UPSC, SSC, Banking, Railways & State PSC MCQs with Answers. It is the quickest way to reinforce what you just learned.

Frequently Asked Questions

What is an NPA and what is the 90-day rule?

What are the three categories of NPAs?

What is the difference between GNPA and NNPA?

What is the IBC and how does it work?

What is a wilful defaulter?

What is the CAMELS rating system?

What is the Prompt Corrective Action (PCA) Framework?

About the author