SARFAESI Act 2002 and DICGC – Complete Banking Awareness Notes 2026 for IBPS and SBI

SARFAESI Act and DICGC covers two critical banking laws. SARFAESI (Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002) enables banks to recover NPAs by taking possession of secured assets without court intervention. DICGC (Deposit Insurance and Credit Guarantee Corporation) protects depositors by insuring their deposits up to Rs. 5 lakh per depositor per bank. Both topics are frequently tested in IBPS PO, SBI Clerk, RBI Grade B and NABARD examinations. The chapter covers complete SARFAESI provisions, the process of enforcement, ARC structure, Security Receipts, DICGC establishment, coverage, premium structure, institutions covered and not covered, the depositor protection timeline and international deposit insurance comparisons.

Jump to section

- SARFAESI Act 2002 - Introduction and Background

- SARFAESI Act - Key Provisions and Parameters

- What SARFAESI Does NOT Cover

- Three Roles of SARFAESI - Detailed Explanation

- DICGC - Deposit Insurance and Credit Guarantee Corporation

- History of Deposit Insurance Coverage Limits in India

- Unclaimed Deposits and DEAF

- International Deposit Insurance Comparison

- Memory Tricks - SARFAESI and DICGC

- One-Liners for Quick Revision - SARFAESI and DICGC

SARFAESI Act 2002 - Introduction and Background

The SARFAESI Act (Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002) was a watershed legislation in India's banking and credit recovery framework. Before its enactment, banks had to rely on slow and cumbersome civil court processes to recover loans — cases routinely took 10 to 15 years to reach resolution, by which time the collateral had deteriorated, the borrower had dissipated assets and recovery rates were dismal.

SARFAESI changed this completely by giving secured creditors (primarily banks) a powerful extra-judicial remedy — the ability to take possession of and sell collateral without any court order, simply by following a defined notice process. The Act was based on recommendations from the Narasimham Committee (Second Report on Banking Sector Reforms, 1998) and the T.R. Andhyarujina Committee.

SARFAESI Act - Key Provisions and Parameters

| Parameter | Details |

|---|---|

| Full Name | Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest Act |

| Year Enacted | 2002 |

| Based on recommendations of | Narasimham Committee II (1998) and T.R. Andhyarujina Committee |

| Minimum NPA Amount | Rs. 1,00,000 (Rupees One Lakh) — loans below this amount are not covered |

| Pre-Notice Requirement | NPA must be more than 90 days overdue and must be a secured loan — collateral must exist |

| 60-Day Notice | Bank must serve formal demand notice to borrower and guarantors; demands repayment within 60 days |

| Borrower's Representation Rights | Borrower can make written representation to bank within 60 days; bank must respond within 15 days |

| After 60 days (if no repayment) | Bank can take possession of secured assets, manage the assets or appoint a manager, and sell the assets through public auction or private treaty |

| Borrower's Appeal | Can appeal to Debt Recovery Tribunal (DRT) within 45 days of possession notice; must deposit 50% of dues as pre-deposit to file appeal |

| Applicability to NBFCs | NBFCs with asset size of Rs. 100 crore and above can also invoke SARFAESI powers |

What SARFAESI Does NOT Cover

SARFAESI is a powerful but limited law — it applies only in specific circumstances. It does NOT apply to:

- Unsecured loans: If the bank gave a loan without taking any collateral security, SARFAESI cannot be invoked — no secured asset exists to be seized

- Loans below Rs. 1 lakh: The law sets a minimum threshold — very small loans are excluded

- Agricultural land: Agricultural land cannot be seized or sold under SARFAESI even if it was mortgaged as collateral — this protects the livelihoods of farmers

- Security interest created in aircraft or vessels: Separately governed by aviation and shipping laws

- Any lien on goods

- Rights of unpaid sellers

- Cases pending before courts: If a court or DRT has already taken up the matter, SARFAESI enforcement may be stayed

Three Roles of SARFAESI - Detailed Explanation

Role 1: Securitization

Securitization is the process of converting illiquid bank loans (especially NPAs) into tradeable financial instruments called Security Receipts (SRs). The bank or an ARC pools NPAs together, creates a special purpose vehicle (SPV), and issues SRs against this NPA pool. These SRs are then sold to investors — typically banks, other financial institutions and qualified institutional buyers (QIBs). The investors receive returns as and when the underlying NPAs are recovered.

- Converts stuck bad loans into liquid securities that can be sold to investors willing to take on recovery risk

- Banks receive cash upfront (sometimes partial) or SRs in exchange for NPAs — this helps clean up their balance sheets

- SRs are regulated by RBI — banks must mark SRs to market based on recovery performance

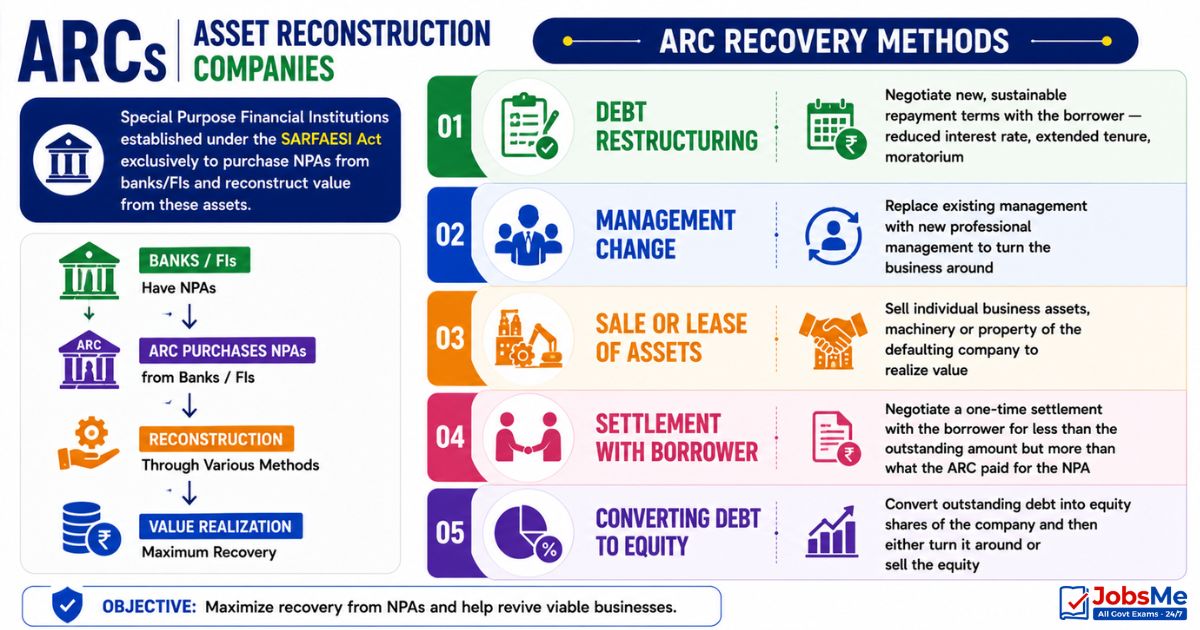

Role 2: Asset Reconstruction

Asset Reconstruction Companies (ARCs) are special purpose financial institutions established under the SARFAESI Act exclusively to purchase NPAs from banks and financial institutions and to reconstruct value from these assets through various methods:

| ARC Recovery Method | Description |

|---|---|

| Debt restructuring | Negotiate new, sustainable repayment terms with the borrower — reduced interest rate, extended tenure, moratorium |

| Management change | Replace existing management with new professional management to turn the business around |

| Sale or lease of assets | Sell individual business assets, machinery or property of the defaulting company to realize value |

| Settlement with borrower | Negotiate a one-time settlement with the borrower for less than the outstanding amount but more than what the ARC paid for the NPA |

| Converting debt to equity | Convert outstanding debt into equity shares of the company and then either turn it around or sell the equity |

ARCIL - First ARC in India

ARCIL (Asset Reconstruction Company (India) Limited) was the first ARC established in India, incorporated in 2002 immediately after the enactment of SARFAESI. It was promoted by four major public sector banks:

- State Bank of India (SBI)

- ICICI Bank

- IDBI Bank

- Punjab National Bank (PNB)

Other significant ARCs operating in India include Edelweiss ARC, JM Financial ARC, Phoenix ARC, Prudent ARC, CFM ARC, INvAsc ARC and ACRE (Asset Care and Reconstruction Enterprise).

ARC Capital Requirements

- Minimum net owned funds (NOF): Rs. 100 crore for ARC registration with RBI

- ARCs can purchase NPAs from multiple banks; they are themselves regulated by RBI

- ARCs must invest at least 15% of each NPA lot they purchase as their own money (the remaining 85% can be through SRs to be recovered later)

- Banks must provision on SRs based on the ARC's actual recovery performance — if recovery is slow, banks must make higher provisions on SRs held

Role 3: Enforcement of Security Interest

The enforcement role is the most widely used and most powerful aspect of SARFAESI. It allows banks to directly enforce their security interest — take possession of and sell the collateral — without any court order. This is a completely extra-judicial remedy.

SARFAESI Enforcement Process - Step by Step

- Account classified as NPA — Loan overdue for 90+ days; amount Rs. 1 lakh+; secured by tangible collateral

- 60-day demand notice issued — Bank formally demands full repayment from borrower and guarantors within 60 days; notice must specify the amount due and the secured assets involved

- Borrower may represent — Within 60 days, borrower can submit a written explanation; bank must respond within 15 days

- No repayment after 60 days — If borrower does not repay or the bank rejects the representation, bank proceeds to take possession

- Possession notice — Bank issues a possession notice and takes physical possession of the secured asset (property, machinery, vehicle)

- Valuation — The bank gets the asset independently valued by a registered valuer

- Publication and public notice — Auction details published in two leading newspapers (one in English, one in vernacular language) with at least 30 days' notice to bidders

- Auction — Bank conducts a public auction (or private treaty) and sells the asset to the highest bidder above the reserve price

- Surplus to borrower — If the auction proceeds exceed the outstanding dues, the surplus is paid to the borrower

DICGC - Deposit Insurance and Credit Guarantee Corporation

Background and Establishment

Deposit insurance is a government-backed guarantee to bank depositors that their deposits are safe up to a specified amount even if the bank fails. India has had some form of deposit insurance since 1962. The DICGC as it exists today was formally established on July 15, 1978 under the DICGC Act, 1961, by merging the Deposit Insurance Corporation (established in 1962) and the Credit Guarantee Corporation of India (established in 1971).

| Parameter | Details |

|---|---|

| Full Name | Deposit Insurance and Credit Guarantee Corporation |

| Established | July 15, 1978 |

| Governed by | DICGC Act, 1961 |

| Ownership | Wholly-owned subsidiary of the Reserve Bank of India |

| Headquarters | Mumbai |

| Current Insurance Coverage | Rs. 5,00,000 (Rupees Five Lakh) per depositor per bank — covering both principal and interest |

| Previous Coverage | Rs. 1,00,000 (Rupees One Lakh) — raised to Rs. 5 lakh in Union Budget 2020 (presented February 1, 2020, effective from February 4, 2020) |

| Insurance Premium Rate | 12 paise per Rs. 100 of assessable deposits per annum — paid by the insured bank; depositors pay nothing |

| Proposed Reform (2025) | RBI proposed a risk-based differential premium system in October 2025 — stronger banks would pay lower premiums; weaker banks would pay higher premiums based on their risk profile |

How DICGC Protection Works

When a bank fails — either through liquidation, merger under government order, or cancellation of its banking licence — DICGC pays the insured deposits to eligible depositors. The process involves:

- RBI cancels the bank's licence or initiates liquidation/amalgamation

- The liquidator or the acquiring bank submits a claim list to DICGC with depositor details and amounts due

- DICGC verifies the claims and pays each eligible depositor up to Rs. 5 lakh (combining principal and accrued interest across all accounts in the same bank)

- DICGC then steps into the shoes of the paid depositors and lodges a claim against the failed bank's liquidation estate for its own reimbursement

Important: The Rs. 5 lakh limit applies per depositor per bank — meaning all accounts held in the same bank are aggregated. However, deposits in different banks are insured separately — Rs. 5 lakh each. A depositor with accounts in five banks is insured for up to Rs. 25 lakh total.

Deposits and Account Types Covered by DICGC

- Savings accounts

- Fixed deposits (term deposits)

- Recurring deposits

- Current accounts

- All types of accounts in branches within India

Institutions Covered by DICGC

- All scheduled commercial banks — public sector, private sector and foreign banks with branches in India

- Regional Rural Banks (RRBs)

- Local Area Banks (LABs)

- Small Finance Banks (SFBs)

- Payment Banks

- Cooperative banks that have opted into the DICGC scheme (most urban cooperative banks and state cooperative banks are covered)

Deposits and Institutions NOT Covered by DICGC

- Inter-bank deposits: Deposits placed by one bank with another bank are not insured

- Central Government deposits: Government's own deposits with banks are excluded

- State Government deposits: State Government funds deposited with banks are excluded

- State Land Development Bank deposits with State Cooperative Banks

- Foreign government deposits

- Any deposit specifically exempted by DICGC with RBI approval

- Primary Agricultural Credit Societies (PACS): These village-level cooperatives are not covered

- Cooperative banks in certain territories: Meghalaya, Chandigarh, Lakshadweep, Dadra and Nagar Haveli (for historical regulatory jurisdiction reasons)

- Non-Banking Financial Companies (NBFCs): Deposits with NBFCs are not covered by DICGC — a major risk for depositors in NBFCs compared to banks

History of Deposit Insurance Coverage Limits in India

| Period | Coverage Limit |

|---|---|

| 1962 (inception) | Rs. 1,500 per depositor per bank |

| 1968 | Rs. 5,000 per depositor per bank |

| 1970 | Rs. 10,000 per depositor per bank |

| 1976 | Rs. 20,000 per depositor per bank |

| 1980 | Rs. 30,000 per depositor per bank |

| 1993 | Rs. 1,00,000 (Rs. 1 lakh) per depositor per bank |

| February 2020 | Rs. 5,00,000 (Rs. 5 lakh) per depositor per bank — current limit |

The 2020 enhancement from Rs. 1 lakh to Rs. 5 lakh was the first increase in coverage since 1993 — a gap of 27 years. The trigger for this increase was the crisis at Punjab and Maharashtra Co-operative (PMC) Bank in 2019, which left over 900,000 depositors unable to access their savings. The increased coverage now protects approximately 98% of all depositors (by number) fully, though they account for a much smaller share of the total deposit value.

Unclaimed Deposits and DEAF

When bank deposits remain unclaimed for more than 10 years, banks are required under the Banking Regulation Act to transfer these funds to the DEAF (Depositor Education and Awareness Fund) maintained by the Reserve Bank of India. Key facts:

- DEAF was established under Section 26A of the Banking Regulation Act, 1949

- Banks must transfer unclaimed deposits to DEAF on a monthly basis

- The depositor or their legal heirs can claim the money from their bank at any time — even after transfer to DEAF — and the bank will reimburse them and claim back from DEAF

- Interest continues to accrue on deposits even after transfer to DEAF at the same rate as savings deposits

- RBI uses DEAF funds to run depositor education and financial literacy programs

- UDGAM Portal: RBI launched the UDGAM (Unclaimed Deposits Gateway to Access inforMation) portal as a centralized platform for depositors to search for their unclaimed deposits across multiple banks. As of July 2025, over 8.59 lakh users had registered on the UDGAM portal

International Deposit Insurance Comparison

| Country | Scheme Name | Coverage Amount | Year Established |

|---|---|---|---|

| India | DICGC (Deposit Insurance and Credit Guarantee Corporation) | Rs. 5 lakh (approximately USD 6,000) per depositor per bank | 1978 (precursor since 1962) |

| USA | FDIC (Federal Deposit Insurance Corporation) | USD 2,50,000 per depositor per bank per ownership category | 1933 (Great Depression era) |

| United Kingdom | FSCS (Financial Services Compensation Scheme) | GBP 85,000 per depositor per bank | 2001 |

| European Union | EDIS (European Deposit Insurance Scheme) / National DGS | EUR 1,00,000 per depositor per bank | EDIS proposed 2015; National DGS vary |

| Canada | CDIC (Canada Deposit Insurance Corporation) | CAD 1,00,000 per depositor per category per institution | 1967 |

| Australia | Financial Claims Scheme (FCS) | AUD 2,50,000 per depositor per institution | 2008 |

| Japan | Deposit Insurance Corporation of Japan (DIC) | JPY 10 million (approximately USD 65,000) per depositor per bank | 1971 |

Memory Tricks - SARFAESI and DICGC

Remember SARFAESI Three Roles

Trick: S-A-E = Securitization (convert NPAs to SRs), Asset Reconstruction (ARCs buy NPAs), Enforcement (banks seize and sell collateral). The Act's name contains all three: Securitization, Reconstruction, Enforcement.

Remember the 60-Day Rule

Trick: SARFAESI gives borrower 60 days to pay or appeal. After 60 days of notice, bank can seize. Then borrower has 45 days to go to DRT. Two timeframes: 60 days for bank notice, 45 days for borrower's DRT appeal.

Remember SARFAESI Exclusions

Trick: SARFAESI cannot touch AGU — Agricultural land, unsecured loans Under Rs. 1 lakh. AGU is what SARFAESI cannot do.

Remember DICGC Coverage

Trick: DICGC = "Deposits Insured — Can Get Compensation." The Rs. 5 lakh limit since 2020. Think: DICGC protects a FIVE-lakh safety net for every depositor in every bank. Five separate banks = five separate Rs. 5 lakh protections.

Remember DICGC vs FDIC

Trick: FDIC (USA) = 250,000 USD. DICGC (India) = 5 lakh INR. FDIC is much larger in absolute terms — because Indian per-capita income is far lower, Rs. 5 lakh covers 98% of Indian depositors by number.

Remember Deposit Insurance History

Trick: India had Rs. 1 lakh coverage from 1993 to 2020 — 27 long years unchanged. Then PMC Bank crisis (2019) → Government acted → Rs. 5 lakh from 2020. Crisis → Policy response → Bigger coverage.

One-Liners for Quick Revision - SARFAESI and DICGC

- SARFAESI Act enacted: 2002; enables NPA recovery without court order.

- SARFAESI based on: Narasimham Committee II (1998) and T.R. Andhyarujina Committee recommendations.

- SARFAESI applies to: secured loans of Rs. 1 lakh and above.

- SARFAESI 60-day notice: bank must give borrower 60 days to respond before seizing assets.

- Borrower's DRT appeal: within 45 days of possession; pre-deposit 50% of dues required.

- SARFAESI does NOT cover: agricultural land, unsecured loans, loans below Rs. 1 lakh.

- Three roles of SARFAESI: Securitization, Asset Reconstruction, Enforcement.

- ARCIL: first ARC in India (2002); promoted by SBI, ICICI Bank, IDBI Bank, PNB.

- ARC minimum capital: Rs. 100 crore net owned funds; regulated by RBI.

- Security Receipts (SRs): issued by ARCs to banks in exchange for NPA portfolios.

- DICGC established: July 15, 1978; under DICGC Act 1961.

- DICGC: wholly-owned subsidiary of RBI; headquarters in Mumbai.

- DICGC coverage: Rs. 5,00,000 per depositor per bank (raised from Rs. 1 lakh in February 2020).

- DICGC covers: principal plus interest combined up to Rs. 5 lakh.

- DICGC premium: 12 paise per Rs. 100 of assessable deposits; paid by banks, not depositors.

- Different banks = separate insurance: deposits in 5 banks = 5 × Rs. 5 lakh protection.

- DICGC does NOT cover: NBFCs, PACS, inter-bank deposits, government deposits.

- Unclaimed deposits transferred to DEAF after 10 years; claimable at any time.

- UDGAM portal: 8.59 lakh users searching for unclaimed deposits (July 2025).

- FDIC (USA): USD 2,50,000; FSCS (UK): GBP 85,000; EDIS (EU): EUR 1,00,000.

- 98% of Indian depositors by number are fully covered by DICGC Rs. 5 lakh limit.

Preparing for competitive exams requires consistent revision. Platforms like JobsMe simplify preparation through:

- Daily Current Affairs

- Weekly Current Affairs

- Monthly Current Affairs

- Static GK for Competitive Exams

- Latest Government Jobs Notifications

- Computer Awareness

Stay updated, revise regularly, and attempt quizzes for better accuracy in UPSC, SSC CGL, IBPS PO/Clerk, SBI, RBI Grade B, RRB NTPC, Defence, and State PSC exams.

Free quiz • No signup required

Put this topic into practice with Current Affairs Quiz 20 June 2026 | UPSC, SSC, Banking, Railways & State PSC MCQs with Answers. It is the quickest way to reinforce what you just learned.

Frequently Asked Questions

What is the SARFAESI Act and why was it enacted?

What is the 60-day notice period under SARFAESI?

What are the three roles of the SARFAESI Act?

What is DICGC and how much deposit insurance does it provide?

What is a Security Receipt issued by an ARC?

Which deposits are NOT covered by DICGC?

What is the DEAF (Depositor Education and Awareness Fund)?

About the author