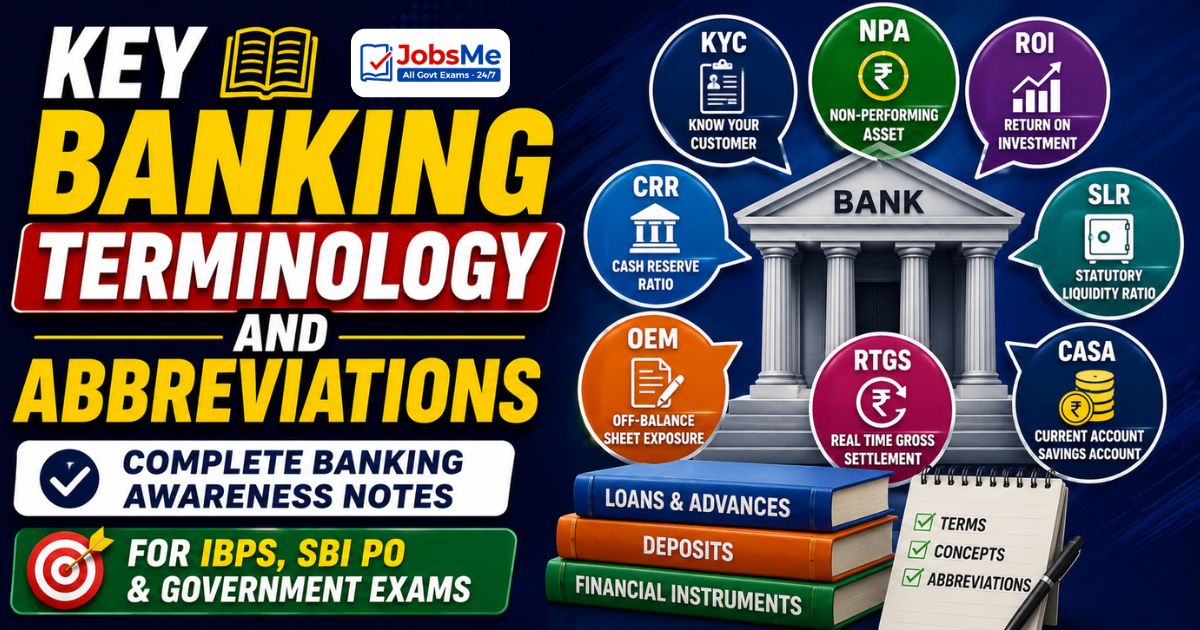

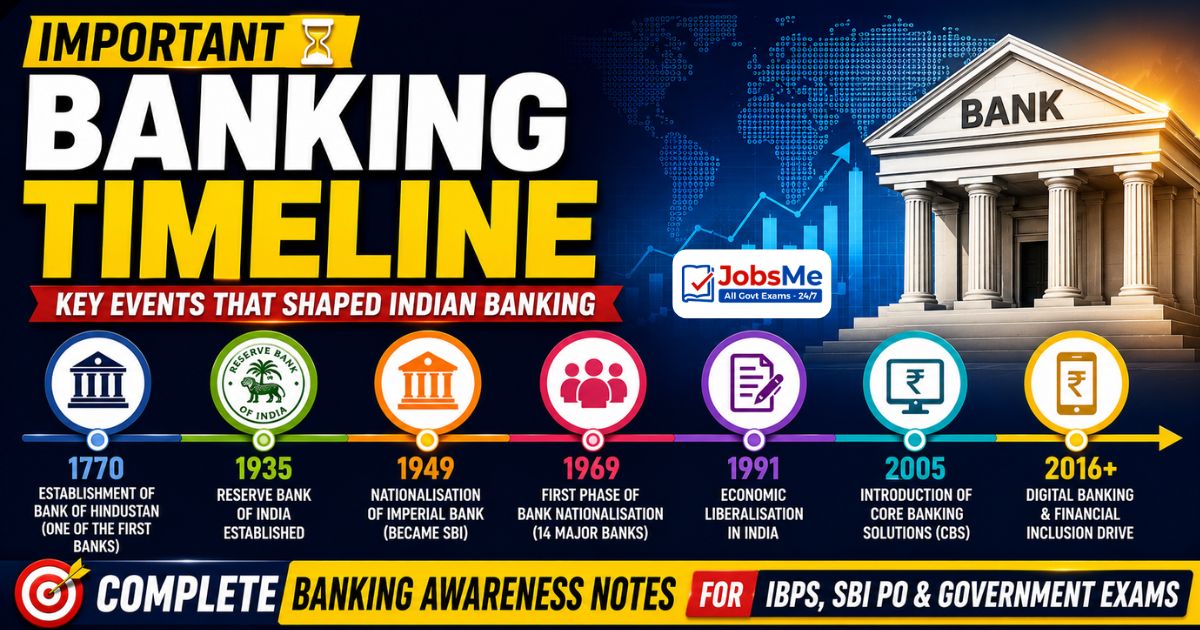

Banking and Financial Schemes – Complete Banking Awareness Notes 2026 for IBPS, SBI PO and RBI Grade B

Banking and Financial Schemes is one of the highest-frequency topics in banking awareness examinations. This chapter provides complete exam-ready coverage of every government and RBI-sponsored scheme including small savings schemes with current interest rates, financial inclusion schemes (PMJDY, MUDRA, Stand Up India, PM SVANidhi), agricultural credit schemes (KCC, PM-KISAN), pension schemes (APY, NPS), insurance schemes (PMJJBY, PMSBY) and the DBT/JAM infrastructure.

Jump to section

Banking and Financial Schemes - Introduction

Government and RBI-sponsored financial schemes are among the most consistently tested areas in every banking awareness examination. Questions test scheme names, launch dates, key features, eligibility, interest rates, tenure and implementing ministry. This chapter provides complete, up-to-date coverage of every major scheme with 2025 data.

Small Savings Schemes - Complete Details

| Scheme | Rate | Tenure | Max Deposit | Tax (EEE / Others) | Key Feature |

|---|---|---|---|---|---|

| PPF (Public Provident Fund) | 7.1% p.a. | 15 years (extendable in 5-yr blocks) | Rs. 1,50,000/year | EEE — fully exempt | Min Rs. 500/year; loan after 3 years; partial withdrawal from 7th year; protected from court attachment |

| NSC (National Savings Certificate) | 7.7% p.a. | 5 years | No limit | 80C; interest taxable but deemed reinvested (80C eligible) | No TDS; no premature closure except on death/court order |

| KVP (Kisan Vikas Patra) | 7.5% p.a. | 115 months (9 yrs 7 months) — doubles investment | No limit | No 80C; interest fully taxable | Premature closure after 2.5 years; no upper limit; transferable to another person |

| SSA (Sukanya Samriddhi) | 8.2% p.a. | 21 years from opening (or marriage after 18) | Rs. 1,50,000/year | EEE — fully exempt | For girl child below 10 years only; max 2 accounts per family; 50% partial withdrawal after age 18 for education |

| SCSS (Senior Citizen Savings Scheme) | 8.2% p.a. | 5 years (extendable by 3 years) | Rs. 30,00,000 | 80C; TDS if interest >Rs. 50,000/year | Age 60+; defence retired from 50; VRS from 55; quarterly payout |

| MSSC (Mahila Samman Savings Certificate) | 7.5% p.a. | 2 years | Rs. 2,00,000 | No 80C; interest taxable | Only for women and girls; 40% partial withdrawal after 1 year; limited period scheme (till March 2025) |

| POMIS (Post Office Monthly Income) | 7.4% p.a. | 5 years | Rs. 9L (single); Rs. 15L (joint) | No 80C; interest taxable; no TDS | Monthly interest payout; principal returned at maturity |

| Post Office Time Deposit (5-year) | 7.5% p.a. | 5 years | No limit | 80C for 5-year only; interest taxable | Similar to bank FD; government guarantee; available at post offices |

| Post Office RD | 6.7% p.a. | 5 years | No limit | No 80C; interest taxable | Min Rs. 100/month; good for disciplined regular savings |

| Post Office Savings Account | 4.0% p.a. | No fixed tenure | No limit | Interest up to Rs. 10,000 exempt; above taxable | Min balance Rs. 500; used for DBT credit |

Financial Inclusion Schemes

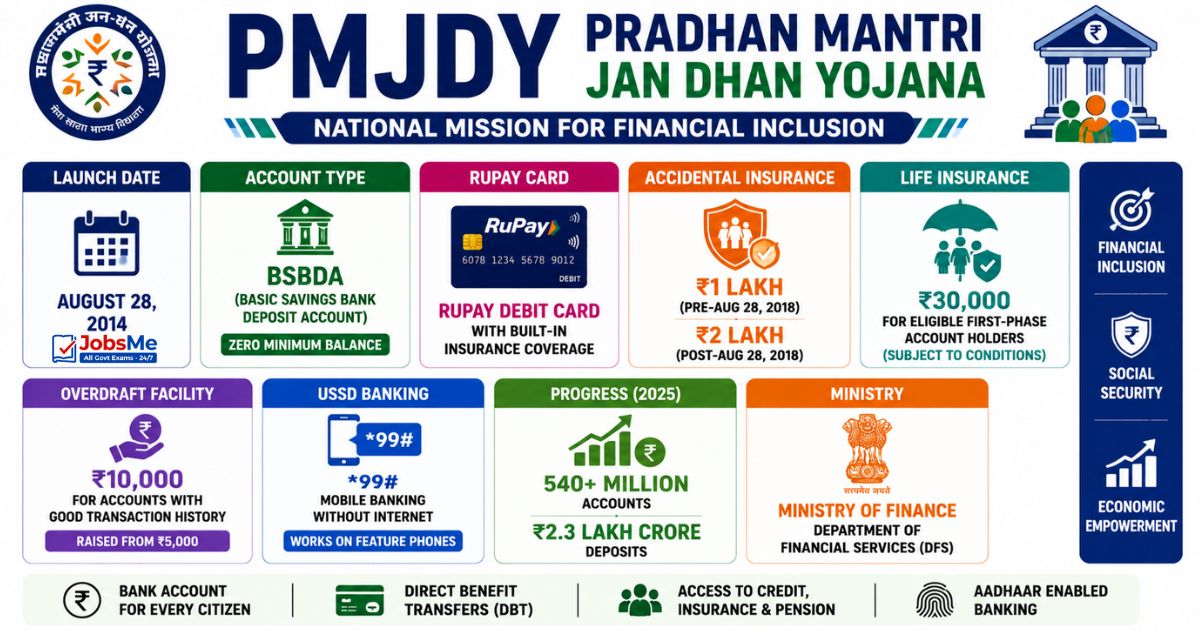

PMJDY - Pradhan Mantri Jan Dhan Yojana

| Parameter | Details |

|---|---|

| Launch Date | August 28, 2014 |

| Account Type | BSBDA (Basic Savings Bank Deposit Account) — zero minimum balance |

| RuPay Card | RuPay debit card with built-in insurance coverage |

| Accidental Insurance | Rs. 1 lakh (pre-August 28, 2018); Rs. 2 lakh (post-August 28, 2018) |

| Life Insurance | Rs. 30,000 for eligible first-phase account holders (subject to conditions) |

| Overdraft Facility | Rs. 10,000 for accounts with good transaction history (raised from Rs. 5,000) |

| USSD Banking | *99# — mobile banking without internet; works on feature phones |

| Progress (2025) | 540+ million accounts; Rs. 2.3 lakh crore deposits |

| Ministry | Ministry of Finance — Department of Financial Services (DFS) |

PM MUDRA Yojana (PMMY)

| Category | Loan Range | Target Borrower |

|---|---|---|

| Shishu | Up to Rs. 50,000 | Startups and very small businesses; no collateral required |

| Kishore | Rs. 50,001 to Rs. 5,00,000 | Businesses with some track record needing expansion capital |

| Tarun | Rs. 5,00,001 to Rs. 10,00,000 | Well-established micro-enterprises seeking further growth |

| Tarun Plus (2024) | Rs. 10,00,001 to Rs. 20,00,000 | Businesses that have successfully repaid Tarun loans |

- Launched: April 8, 2015

- MUDRA: Micro Units Development and Refinance Agency — subsidiary of SIDBI

- Loans routed through commercial banks, RRBs, SFBs, NBFCs, MFIs

- MUDRA Card: RuPay-based card for flexible working capital withdrawals

- Cumulative disbursement: Rs. 27+ lakh crore; 47+ crore loans sanctioned

Stand Up India

| Parameter | Details |

|---|---|

| Launch Date | April 5, 2016 |

| Target | SC/ST entrepreneurs and women entrepreneurs |

| Loan Range | Rs. 10,00,000 to Rs. 1,00,00,000 (Rs. 10 lakh to Rs. 1 crore) |

| Enterprise Type | Greenfield enterprises only (new businesses, not expansion of existing) |

| Bank Branch Target | At least one SC/ST borrower AND one woman borrower per bank branch |

| Repayment | Up to 7 years with moratorium up to 18 months |

| Portal | standupmitra.in |

Startup India

| Parameter | Details |

|---|---|

| Launch Date | January 16, 2016 |

| DPIIT Recognition | Startups must register at startupindia.gov.in for DPIIT recognition |

| Tax Exemption | Income tax exemption for 3 out of first 10 years under Section 80-IAC |

| Patent Fee Rebate | 80% rebate on patent filing fees + fast-track examination |

| Fund of Funds | Rs. 10,000 crore managed by SIDBI to invest in AIFs backing startups |

| Self-Certification | Compliance with 6 labour and 3 environment laws via self-certification |

PM SVANidhi - PM Street Vendor's AtmaNirbhar Nidhi

| Parameter | Details |

|---|---|

| Launch Date | June 1, 2020 |

| Purpose | Working capital loans for street vendors affected by COVID-19 |

| Loan Progression | Rs. 10,000 → Rs. 20,000 → Rs. 50,000 (on timely repayment each time) |

| Interest Subsidy | 7% per annum on timely repayment |

| Digital Incentive | Up to Rs. 1,200 cashback per year for digital transactions |

| Ministry | Ministry of Housing and Urban Affairs; SIDBI as nodal agency |

Agricultural Credit and Farm Schemes

Kisan Credit Card (KCC)

| Parameter | Details |

|---|---|

| Launched | 1998 — based on R.V. Gupta Committee recommendations |

| Purpose | Flexible revolving credit for crop production, post-harvest expenses, farm asset maintenance, allied activities and personal consumption needs of farmers |

| Credit Nature | Revolving — farmers draw, repay and redraw within limit through the crop cycle |

| Validity | 5 years with annual review |

| Credit Limit | Based on scale of finance for crops; increases 10% per year for 5 years |

| Eligible Borrowers | Owner-cultivators; tenant farmers; oral lessees; share croppers; SHGs and JLGs of farmers; fishermen (extended to allied sectors) |

| Issuing Banks | Commercial Banks, RRBs, Small Finance Banks, Cooperative Banks |

| Interest Subvention | Government provides interest subvention; effective rate for prompt repayers kept at 4% p.a. (Kisan Short Term Crop Loan Interest Subvention Scheme) |

| Insurance | KCC holders eligible for PMFBY (Pradhan Mantri Fasal Bima Yojana) crop insurance |

PM-KISAN - Pradhan Mantri Kisan Samman Nidhi

| Parameter | Details |

|---|---|

| Launch Date | February 24, 2019 (announced in Interim Budget 2019) |

| Purpose | Direct income support to farmer families to meet agricultural input costs and other needs |

| Amount | Rs. 6,000 per year in three equal installments of Rs. 2,000 each (every 4 months) |

| Transfer Mode | Direct Benefit Transfer (DBT) directly into farmer's Aadhaar-linked bank account |

| Eligibility | All landholding farmer families with cultivable landholding (originally small and marginal only; expanded to all in 2019) |

| Excluded | Income taxpayers; former or serving government officers; doctors, engineers, chartered accountants; retirees with pension above Rs. 10,000/month |

| Progress (2025) | Over 11 crore farmers receiving benefits; Rs. 3.45 lakh crore disbursed cumulatively |

| Ministry | Ministry of Agriculture and Farmers' Welfare |

PMFBY - Pradhan Mantri Fasal Bima Yojana

| Parameter | Details |

|---|---|

| Launch Date | February 18, 2016 (replaced National Agricultural Insurance Scheme) |

| Purpose | Crop insurance to protect farmers against crop loss due to natural calamities, pest attack and diseases |

| Premium by Farmer | Maximum 2% for kharif crops; 1.5% for rabi crops; 5% for horticulture and commercial crops |

| Premium Balance | Remaining premium shared equally between State and Central Government |

| Implementing Agency | Agriculture Insurance Company of India (AIC) and empanelled private insurers |

| Technology | Satellite imagery, drone surveys and smartphone apps for quick crop loss assessment |

Pension Schemes

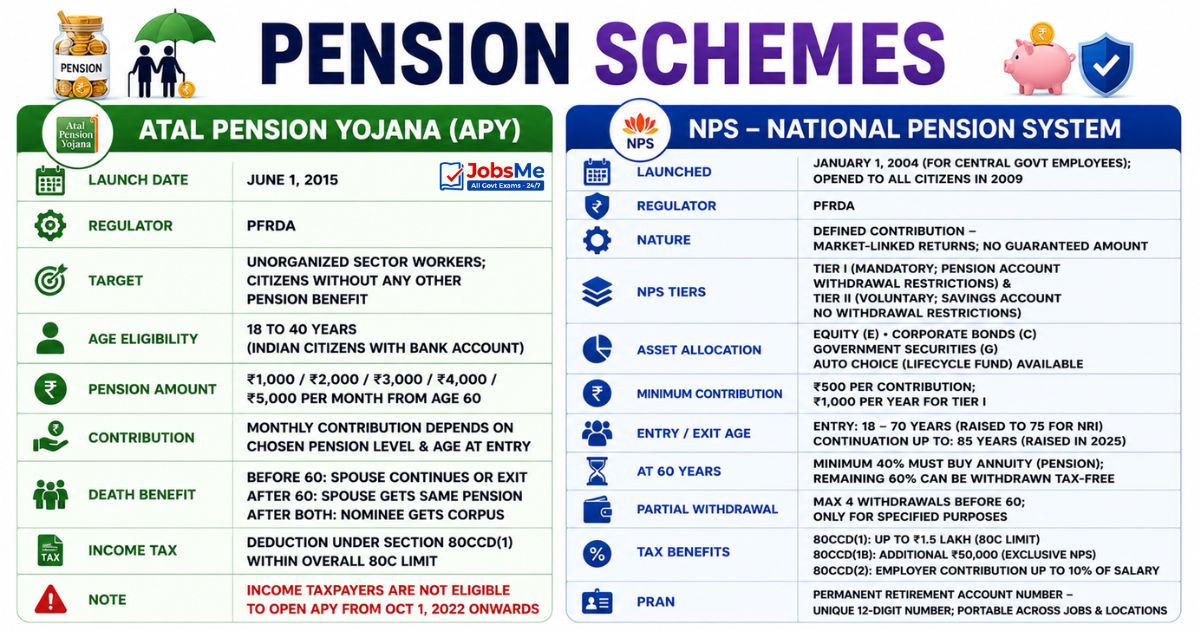

Atal Pension Yojana (APY)

| Parameter | Details |

|---|---|

| Launch Date | June 1, 2015 |

| Regulator | PFRDA (Pension Fund Regulatory and Development Authority) |

| Target | Unorganized sector workers; citizens without any other pension benefit |

| Age Eligibility | Indian citizens aged 18 to 40 years with a bank account |

| Pension Amount | Guaranteed fixed monthly pension of Rs. 1,000 / Rs. 2,000 / Rs. 3,000 / Rs. 4,000 or Rs. 5,000 (subscriber's choice) from age 60 |

| Contribution | Monthly contribution depends on chosen pension level and age at entry — the younger you join, the lower the monthly contribution |

| Death Benefit | If subscriber dies before 60, spouse can continue contributions or exit; if subscriber dies after 60, spouse receives same pension; after both die, nominee receives accumulated corpus |

| Income Tax | Contribution qualifies for deduction under Section 80CCD(1) within the overall Section 80C limit |

| Note | Income taxpayers are not eligible to open APY from October 1, 2022 onwards |

NPS - National Pension System

| Parameter | Details |

|---|---|

| Launched | January 1, 2004 for central government employees; opened to all citizens in 2009 |

| Regulator | PFRDA (Pension Fund Regulatory and Development Authority) |

| Nature | Defined Contribution — market-linked returns; no guaranteed pension amount |

| NPS Tiers | Tier I (mandatory; pension account with withdrawal restrictions) and Tier II (voluntary; savings account with no withdrawal restrictions) |

| Asset Allocation | Subscriber chooses allocation among Equity (E), Corporate Bonds (C) and Government Securities (G); Auto Choice (lifecycle fund) is available for those who prefer default allocation |

| Minimum Contribution | Rs. 500 per contribution; Rs. 1,000 per year for Tier I |

| Entry/Exit Age | Minimum entry age: 18 years; maximum: 70 years (raised to 75 years for NRI); maximum age for continuation: 85 years (raised in 2025) |

| At 60 Years | Minimum 40% of accumulated corpus must be used to purchase annuity (pension); remaining 60% can be withdrawn tax-free |

| Partial Withdrawal | Maximum 4 partial withdrawals before age 60; only for specified purposes (higher education, home purchase, serious illness, disability) |

| Tax Benefits | Contribution under 80CCD(1) within Rs. 1.5 lakh (80C limit); additional Rs. 50,000 under 80CCD(1B) — exclusive NPS benefit; employer contribution up to 10% of salary under 80CCD(2) |

| PRAN | Permanent Retirement Account Number — unique 12-digit number allotted to each NPS subscriber; portable across jobs and locations |

Government Insurance Schemes

| Scheme | Launch | Premium | Cover | Eligibility |

|---|---|---|---|---|

| PMJJBY (Pradhan Mantri Jeevan Jyoti Bima Yojana) | May 9, 2015 | Rs. 436/year (revised; auto-deducted from bank account) | Rs. 2,00,000 life insurance (death due to any cause) | Age 18-50 years with bank/post office account; renewable annually till 55 |

| PMSBY (Pradhan Mantri Suraksha Bima Yojana) | May 9, 2015 | Rs. 20/year (auto-deducted) | Rs. 2,00,000 for accidental death or permanent total disability; Rs. 1,00,000 for permanent partial disability | Age 18-70 years with bank/post office account |

DBT and JAM Trinity

DBT - Direct Benefit Transfer

| Parameter | Details |

|---|---|

| Launch Date | January 1, 2013 (pilot in 43 districts) |

| Purpose | Transfer government subsidies and benefits directly into the bank accounts of beneficiaries — eliminating middlemen, reducing leakage and improving targeting |

| Infrastructure | Built on the JAM (Jan Dhan-Aadhaar-Mobile) trinity |

| Schemes Covered | Over 1,000 central government schemes including LPG subsidy (PAHAL), MGNREGS wages, PM-KISAN, scholarship schemes, food subsidy, PMJDY overdraft |

| Savings to Exchequer | DBT has saved the government over Rs. 3 lakh crore by eliminating ghost beneficiaries and duplicate entries since inception |

JAM Trinity - The Digital Infrastructure for Financial Inclusion

JAM stands for Jan Dhan + Aadhaar + Mobile. These three components work together to form India's digital financial infrastructure enabling universal, frictionless and leakage-free benefit delivery.

| Component | Role | Administered by |

|---|---|---|

| Jan Dhan (PMJDY) | Bank account for every citizen — the receiving end of DBT transfers | Ministry of Finance (DFS) |

| Aadhaar | Unique biometric identity — used for authentication, deduplication and Aadhaar-linked payment routing via AePS | UIDAI (Unique Identification Authority of India) |

| Mobile | Real-time OTP-based authentication; UPI and USSD-based banking on feature phones; *99# for non-smartphone banking | DoT (Department of Telecommunications) + NPCI |

Other Key Schemes

| Scheme | Launched | Key Feature |

|---|---|---|

| PMAY-G (Pradhan Mantri Awas Yojana - Gramin) | November 20, 2016 | Housing for all in rural areas by 2024; Rs. 1.2 lakh (plains) to Rs. 1.3 lakh (hilly/NE) per unit; DBT payment directly to beneficiary |

| PMAY-U (Urban) | June 25, 2015 | Affordable housing for economically weaker sections and low-income groups in urban areas; interest subsidy on home loans under CLSS (Credit Linked Subsidy Scheme) |

| MGNREGS (Mahatma Gandhi NREGS) | February 2, 2006 | Guaranteed 100 days of employment per year to rural households; wages paid directly via DBT to bank/post office accounts |

| PM Garib Kalyan Anna Yojana (PMGKAY) | April 2020 (COVID relief) | Free ration (5 kg grain per person per month) to NFSA beneficiaries; merged with regular PDS from January 1, 2024 |

| e-RUPI | August 2021 | Prepaid digital voucher via QR code or SMS; no bank account needed; targeted welfare delivery; programmable (single-use, specific purpose) |

| ULI (Unified Lending Interface) | Pilot 2023; expanded 2025 | RBI's digital credit delivery platform; consent-based data sharing for frictionless loans to farmers and MSMEs; 3.2 million loans; Rs. 1.75 trillion disbursed (Oct 2025) |

| UDGAM Portal | August 18, 2023 | RBI portal for depositors to search unclaimed deposits across multiple banks; 8.59 lakh users (July 2025) |

| PRAVAAH | May 28, 2024 | RBI's online portal for regulatory approvals (Platform for Regulatory Application, Validation and AutHorisation); single-window for all RBI licence/approval applications |

| RB-IOS 2021 (Banking Ombudsman) | November 12, 2021 | One Nation One Ombudsman; integrated scheme replacing three separate ombudsman schemes; 22 offices; online complaint at cms.rbi.org.in |

Memory Tricks - Banking Schemes

Remember MUDRA Categories

Trick: SKT = Shishu (child — up to Rs. 50k), Kishore (teen — Rs. 50k to Rs. 5L), Tarun (adult — Rs. 5L to Rs. 10L). And now Tarun Plus (Rs. 10L to Rs. 20L). Like stages of human growth.

Remember PPF Key Numbers

Trick: PPF = 15 years, 7.1%, Rs. 1.5 lakh max, EEE. Easy to recall: PPF has 3 key numbers — 15 (years), 1.5 (lakh max), 7.1 (rate). EEE = completely tax-free at all three stages.

Remember SSA vs SCSS

Trick: SSA = Girl child, 8.2%, 21 years, EEE. SCSS = Senior citizen (60+), 8.2%, 5 years, max Rs. 30 lakh, quarterly payout. Both earn 8.2% — the highest rates among small savings. SSA = daughter's future; SCSS = parent's retirement.

Remember PMJJBY vs PMSBY

Trick: PMJJBY = Life insurance (Jeevan = life); Rs. 436/year; Rs. 2 lakh cover; age 18-50. PMSBY = Accident insurance (Suraksha = safety/protection); Rs. 20/year; Rs. 2 lakh cover; age 18-70. J for Jeevan (life) — higher premium. S for Suraksha (protection) — lowest premium of any scheme in India.

Remember APY vs NPS

Trick: APY = Atal = Guaranteed pension (fixed Rs. 1k-5k); unorganized sector; 18-40 years. NPS = National = Not guaranteed (market-linked); all citizens; 18-75 years. APY = Assured. NPS = Not guaranteed but potentially higher.

Remember JAM Trinity

Trick: JAM = Jan Dhan (account) + Aadhaar (identity) + Mobile (delivery). JAM unlocks DBT — the three keys that together open the door to direct government benefit delivery.

One-Liners for Quick Revision

- PPF: 7.1%; 15 years; max Rs. 1.5 lakh/year; EEE; loan from 3rd year; withdrawal from 7th year.

- NSC: 7.7%; 5 years; no TDS; interest reinvested deemed as 80C investment.

- KVP: 7.5%; matures in 115 months; money doubles; no upper limit.

- SSA (Sukanya): 8.2%; girl child below 10 years; 21 years tenure; EEE; min Rs. 250/year.

- SCSS: 8.2%; age 60+; max Rs. 30 lakh; quarterly payout; 80C deduction.

- MSSC: 7.5%; women and girls only; max Rs. 2 lakh; 2 years tenure.

- POMIS: 7.4%; max Rs. 9L (single), Rs. 15L (joint); monthly payout.

- PMJDY launched: August 28, 2014; accident insurance Rs. 2 lakh; overdraft Rs. 10,000.

- MUDRA: Shishu up to Rs. 50k; Kishore up to Rs. 5L; Tarun up to Rs. 10L; Tarun Plus up to Rs. 20L.

- Stand Up India: Rs. 10L to Rs. 1 crore; SC/ST and women; greenfield only; launched April 5, 2016.

- Startup India: January 16, 2016; 3-year tax holiday; DPIIT recognition; SIDBI Fund of Funds Rs. 10,000 crore.

- PM SVANidhi: June 1, 2020; street vendors; Rs. 10k → Rs. 20k → Rs. 50k; 7% interest subsidy.

- KCC: launched 1998; R.V. Gupta Committee; revolving credit; 5-year validity.

- PM-KISAN: February 24, 2019; Rs. 6,000/year in 3 installments of Rs. 2,000 via DBT.

- PMFBY: crop insurance; farmer pays max 2% kharif, 1.5% rabi, 5% horticulture.

- PMJJBY: life insurance; Rs. 436/year; Rs. 2 lakh cover; age 18-50 years.

- PMSBY: accident insurance; Rs. 20/year; Rs. 2 lakh cover; age 18-70 years.

- APY: guaranteed pension Rs. 1,000-Rs. 5,000/month; for age 18-40 years; regulated by PFRDA.

- NPS: market-linked; upper age raised to 85 years (2025); at 60 must annuitize minimum 40%.

- DBT launched: January 1, 2013; JAM = Jan Dhan + Aadhaar + Mobile; saved Rs. 3 lakh crore+ to exchequer.

- UDGAM portal: RBI portal for unclaimed deposits; 8.59 lakh users (July 2025).

- RB-IOS 2021: One Nation One Ombudsman; launched November 12, 2021; 22 offices.

Preparing for competitive exams requires consistent revision. Platforms like JobsMe simplify preparation through:

- Daily Current Affairs

- Weekly Current Affairs

- Monthly Current Affairs

- Static GK for Competitive Exams

- Latest Government Jobs Notifications

- Computer Awareness

Stay updated, revise regularly, and attempt quizzes for better accuracy in UPSC, SSC CGL, IBPS PO/Clerk, SBI, RBI Grade B, RRB NTPC, Defence, and State PSC exams.

Free quiz • No signup required

Put this topic into practice with Current Affairs Quiz 20 June 2026 | UPSC, SSC, Banking, Railways & State PSC MCQs with Answers. It is the quickest way to reinforce what you just learned.

Frequently Asked Questions

What is PMJDY and what are its key features?

What are the three categories under PM MUDRA Yojana?

What is the Sukanya Samriddhi Account?

What is the difference between APY and NPS?

About the author